Latest by

-

SpaceX: Pioneering Space Manufacturing and Mars Colonization "We will move humanity to Mars and make it a colony of Earth." In early 2001, Elon Musk attended a fundraising event for the Mars Society, a nonprofit focused on space exploration. He donated $100,000 and joined the board. At that time, Musk had a modest dream of building a small greenhouse on Mars. That fall, he traveled to Russia to purchase decommissioned intercontinental ballistic missiles (ICBMs) to secure a launch vehicle. After negotiations with Russia fell through, Musk resolved to build his own rockets, leading to the founding of SpaceX. This marked the beginning of his vision for the "migration of Earthlings to Mars and the establishment of a multi-planetary species." Musk was once labeled a "great dreamer" and a "fraud," with some viewing his ambitions as unrealistic. However, 24 years later, his trajectory suggests otherwise. To fund the astronomical costs of reaching Mars, Musk founded Tesla, focusing on autonomous driving technology. He also established Tesla Energy to secure energy for the era of space manufacturing. This initiative includes the development of "Gigafactories," aiming for fully automated manufacturing facilities without human intervention. SpaceX has developed reusable launch vehicles and is also working on humanoid robots capable of performing tasks like humans. On the evening of June 23, Korean time, SpaceX successfully tested its unmanned re-entry capsule, "Starfall," designed to deliver goods manufactured in space back to Earth. This vision of establishing advanced manufacturing facilities in space is becoming clearer. Utilizing solar energy and achieving extreme efficiency without biological intervention, SpaceX aims to produce high-value space-manufactured products that generate revenue and drive technological innovation. Musk's entire trajectory is directed toward the monumental goal of "Mars colonization." At this point, the idea of conquering Mars is no longer a fantasy. Since Musk first mentioned Mars colonization, he has not wasted a single year, and his dream is now becoming a reality. The success of the Starfall launch signifies the realization of the "space manufacturing" era. In the past, both the public and some sectors of academia and industry have questioned, "Why spend enormous amounts of money to manufacture items in space?" However, the emergence of a new material known as "ZBLAN," often referred to as the next-generation optical fiber cable, has drawn attention to space manufacturing. ZBLAN, made by mixing five fluorides including zirconium and barium, theoretically offers signal transmission efficiency that is 10 to 100 times better than existing optical fibers. The challenge is that ZBLAN cannot be manufactured on Earth due to micro-convection caused by gravity, which forms atomic-level defects that block light. Manufacturing it in space, free from gravitational interference, allows for the creation of glass crystals with nearly zero defects. Experiments conducted on the International Space Station (ISS) have successfully produced commercially viable ZBLAN. Applying ZBLAN to undersea cables crossing the Atlantic would eliminate the need for expensive repeaters that compensate for light loss. Its applications extend beyond telecommunications to military lasers and medical equipment. The challenge remains in transporting it back to Earth, a path that SpaceX is paving. While the technology to establish manufacturing facilities in space is enticing, Elon Musk's dream of "Mars exploration" is even more admirable. What our companies need now is the "spirit of challenge that sells dreams." It is time to set goals that will mark a significant chapter in human history and to pursue disruptive innovation that creates new technologies and opens up markets in the process.* This article has been translated by AI. 2026-06-24 14:16:00

SpaceX: Pioneering Space Manufacturing and Mars Colonization "We will move humanity to Mars and make it a colony of Earth." In early 2001, Elon Musk attended a fundraising event for the Mars Society, a nonprofit focused on space exploration. He donated $100,000 and joined the board. At that time, Musk had a modest dream of building a small greenhouse on Mars. That fall, he traveled to Russia to purchase decommissioned intercontinental ballistic missiles (ICBMs) to secure a launch vehicle. After negotiations with Russia fell through, Musk resolved to build his own rockets, leading to the founding of SpaceX. This marked the beginning of his vision for the "migration of Earthlings to Mars and the establishment of a multi-planetary species." Musk was once labeled a "great dreamer" and a "fraud," with some viewing his ambitions as unrealistic. However, 24 years later, his trajectory suggests otherwise. To fund the astronomical costs of reaching Mars, Musk founded Tesla, focusing on autonomous driving technology. He also established Tesla Energy to secure energy for the era of space manufacturing. This initiative includes the development of "Gigafactories," aiming for fully automated manufacturing facilities without human intervention. SpaceX has developed reusable launch vehicles and is also working on humanoid robots capable of performing tasks like humans. On the evening of June 23, Korean time, SpaceX successfully tested its unmanned re-entry capsule, "Starfall," designed to deliver goods manufactured in space back to Earth. This vision of establishing advanced manufacturing facilities in space is becoming clearer. Utilizing solar energy and achieving extreme efficiency without biological intervention, SpaceX aims to produce high-value space-manufactured products that generate revenue and drive technological innovation. Musk's entire trajectory is directed toward the monumental goal of "Mars colonization." At this point, the idea of conquering Mars is no longer a fantasy. Since Musk first mentioned Mars colonization, he has not wasted a single year, and his dream is now becoming a reality. The success of the Starfall launch signifies the realization of the "space manufacturing" era. In the past, both the public and some sectors of academia and industry have questioned, "Why spend enormous amounts of money to manufacture items in space?" However, the emergence of a new material known as "ZBLAN," often referred to as the next-generation optical fiber cable, has drawn attention to space manufacturing. ZBLAN, made by mixing five fluorides including zirconium and barium, theoretically offers signal transmission efficiency that is 10 to 100 times better than existing optical fibers. The challenge is that ZBLAN cannot be manufactured on Earth due to micro-convection caused by gravity, which forms atomic-level defects that block light. Manufacturing it in space, free from gravitational interference, allows for the creation of glass crystals with nearly zero defects. Experiments conducted on the International Space Station (ISS) have successfully produced commercially viable ZBLAN. Applying ZBLAN to undersea cables crossing the Atlantic would eliminate the need for expensive repeaters that compensate for light loss. Its applications extend beyond telecommunications to military lasers and medical equipment. The challenge remains in transporting it back to Earth, a path that SpaceX is paving. While the technology to establish manufacturing facilities in space is enticing, Elon Musk's dream of "Mars exploration" is even more admirable. What our companies need now is the "spirit of challenge that sells dreams." It is time to set goals that will mark a significant chapter in human history and to pursue disruptive innovation that creates new technologies and opens up markets in the process.* This article has been translated by AI. 2026-06-24 14:16:00 -

Trump Calls for Faster Gas Price Reductions Amid Falling Oil Prices Donald Trump, President of the United States, has directed the Department of Justice to investigate major oil companies for not lowering gas prices despite a decline in crude oil prices. On June 24, Trump posted on social media platform Truth Social, stating, "Major oil companies are not reducing gas prices at the pump, even though they are purchasing crude oil at much lower prices." He added, "Crude oil prices are plummeting, which means consumers are getting ripped off." Trump emphasized, "I have instructed the Department of Justice to investigate this issue immediately, and gas prices need to come down much faster than they currently are." These remarks publicly express frustration that the decrease in international oil prices is not being adequately reflected in consumer prices. Trump has consistently highlighted reducing energy prices as a key priority for stabilizing inflation and easing household burdens.* This article has been translated by AI. 2026-06-24 14:16:00

Trump Calls for Faster Gas Price Reductions Amid Falling Oil Prices Donald Trump, President of the United States, has directed the Department of Justice to investigate major oil companies for not lowering gas prices despite a decline in crude oil prices. On June 24, Trump posted on social media platform Truth Social, stating, "Major oil companies are not reducing gas prices at the pump, even though they are purchasing crude oil at much lower prices." He added, "Crude oil prices are plummeting, which means consumers are getting ripped off." Trump emphasized, "I have instructed the Department of Justice to investigate this issue immediately, and gas prices need to come down much faster than they currently are." These remarks publicly express frustration that the decrease in international oil prices is not being adequately reflected in consumer prices. Trump has consistently highlighted reducing energy prices as a key priority for stabilizing inflation and easing household burdens.* This article has been translated by AI. 2026-06-24 14:16:00 -

Surge in Medical School Enrollment Contradicts Access for Non-Local Students Although the number of medical school admissions for the 2027 academic year has significantly increased, the general admissions process, which is open to all applicants regardless of residency, has become more restrictive. Analysts in the education sector suggest that the explosive growth in the regional selection ratio at non-metropolitan medical schools has effectively blocked access for students from the capital region seeking to attend these institutions. According to a report released on June 24 by JinHakSa, the total number of medical school admissions nationwide for the 2027 academic year is set at 3,508, including 488 spots for the newly established regional physician selection program. This marks an increase of 492 from the previous year’s total of 3,016. However, the general admissions category, which allows applicants to apply without residency restrictions, has decreased to 1,757, down 27 from last year’s 1,784. This represents a sharp decline of 11.8% (234 spots) compared to the 2024 academic year, which had 1,991 general admissions. As a result, the ratio of general admissions to regional selections (including local talent and regional physicians) has narrowed to approximately 50.1% to 49.9%, creating a near 5-to-5 balance. Notably, the regional bias in non-metropolitan medical schools has intensified, with 69.4% of the admissions slots (7 out of 10) allocated to local students. An additional analysis of detailed admissions data by JinHakSa reveals stark disparities in regional selection barriers. In the Gwangju and Jeolla region, out of a total of 573 medical school admissions, 443 were filled through regional selection, resulting in an impressive 77.3% ratio. This was followed by Jeju (76.5%), Busan, Ulsan, and Gyeongnam (72.8%), Daegu and Gyeongbuk (70.9%), and Daejeon and Chungcheong (69.6%), all showing overwhelming majorities in regional selections. At the individual university level, the situation is even more pronounced. Dong-A University allocated 56 out of 66 total admissions to regional selection, achieving the highest rate at 84.8%. Chonnam National University (84.0%), Gyeongsang National University (83.7%), Wonkwang University (83.6%), and Dongguk University WISE (83.3%) also confirmed that over 80% of their new students are from local areas. Conversely, the university with the largest reduction in general admissions available to capital region students was Soonchunhyang University, which saw a decrease of 18 spots, followed by Dongguk University WISE (-7 spots) and Gyeongsang National University (-6 spots). Distinct differences are also evident in the types of admissions processes. General admissions are primarily based on regular admissions, which account for 41.3% (726 spots), followed by comprehensive student evaluations at 35.7% (628 spots). In contrast, regional selections are dominated by academic performance evaluations, which comprise 50.5% of the process. This shift in admissions structure means that applicants' strategies will need to adapt significantly based on their residency. This trend reflects not just an expansion of medical school capacity but also the government's commitment to enhancing regional talent selection, which has become more pronounced in the admissions process for the 2027 academic year. The medical school admissions paradigm is rapidly shifting from a nationwide competition to a regional league, suggesting that residency will become a crucial factor in applicants' profiles. Yoo An-cheol, head of JinHakSa's admissions strategy research center, stated, "The most significant change in medical school admissions recently is not the increase in the number of spots, but rather the shift in the selection criteria. Students now need to assess not just how many spots are available, but how many of those spots they are eligible to apply for." He added, "Students who meet the qualifications for regional selection should actively utilize the expanded regional selection tracks, while those preparing for general admissions need to focus their efforts on the types of admissions that align with their strengths, such as regular admissions and comprehensive evaluations."* This article has been translated by AI. 2026-06-24 14:12:00

Surge in Medical School Enrollment Contradicts Access for Non-Local Students Although the number of medical school admissions for the 2027 academic year has significantly increased, the general admissions process, which is open to all applicants regardless of residency, has become more restrictive. Analysts in the education sector suggest that the explosive growth in the regional selection ratio at non-metropolitan medical schools has effectively blocked access for students from the capital region seeking to attend these institutions. According to a report released on June 24 by JinHakSa, the total number of medical school admissions nationwide for the 2027 academic year is set at 3,508, including 488 spots for the newly established regional physician selection program. This marks an increase of 492 from the previous year’s total of 3,016. However, the general admissions category, which allows applicants to apply without residency restrictions, has decreased to 1,757, down 27 from last year’s 1,784. This represents a sharp decline of 11.8% (234 spots) compared to the 2024 academic year, which had 1,991 general admissions. As a result, the ratio of general admissions to regional selections (including local talent and regional physicians) has narrowed to approximately 50.1% to 49.9%, creating a near 5-to-5 balance. Notably, the regional bias in non-metropolitan medical schools has intensified, with 69.4% of the admissions slots (7 out of 10) allocated to local students. An additional analysis of detailed admissions data by JinHakSa reveals stark disparities in regional selection barriers. In the Gwangju and Jeolla region, out of a total of 573 medical school admissions, 443 were filled through regional selection, resulting in an impressive 77.3% ratio. This was followed by Jeju (76.5%), Busan, Ulsan, and Gyeongnam (72.8%), Daegu and Gyeongbuk (70.9%), and Daejeon and Chungcheong (69.6%), all showing overwhelming majorities in regional selections. At the individual university level, the situation is even more pronounced. Dong-A University allocated 56 out of 66 total admissions to regional selection, achieving the highest rate at 84.8%. Chonnam National University (84.0%), Gyeongsang National University (83.7%), Wonkwang University (83.6%), and Dongguk University WISE (83.3%) also confirmed that over 80% of their new students are from local areas. Conversely, the university with the largest reduction in general admissions available to capital region students was Soonchunhyang University, which saw a decrease of 18 spots, followed by Dongguk University WISE (-7 spots) and Gyeongsang National University (-6 spots). Distinct differences are also evident in the types of admissions processes. General admissions are primarily based on regular admissions, which account for 41.3% (726 spots), followed by comprehensive student evaluations at 35.7% (628 spots). In contrast, regional selections are dominated by academic performance evaluations, which comprise 50.5% of the process. This shift in admissions structure means that applicants' strategies will need to adapt significantly based on their residency. This trend reflects not just an expansion of medical school capacity but also the government's commitment to enhancing regional talent selection, which has become more pronounced in the admissions process for the 2027 academic year. The medical school admissions paradigm is rapidly shifting from a nationwide competition to a regional league, suggesting that residency will become a crucial factor in applicants' profiles. Yoo An-cheol, head of JinHakSa's admissions strategy research center, stated, "The most significant change in medical school admissions recently is not the increase in the number of spots, but rather the shift in the selection criteria. Students now need to assess not just how many spots are available, but how many of those spots they are eligible to apply for." He added, "Students who meet the qualifications for regional selection should actively utilize the expanded regional selection tracks, while those preparing for general admissions need to focus their efforts on the types of admissions that align with their strengths, such as regular admissions and comprehensive evaluations."* This article has been translated by AI. 2026-06-24 14:12:00 -

Lotte Hotels Expands Luxury Portfolio with The Grand Lotte The global luxury hotel market is becoming increasingly competitive. Moving beyond the past focus on opulent hardware, the industry now emphasizes 'hyper-personalization' to meet the diverse tastes and experiences of customers. In this context, Lotte Hotels and Resorts, a leader in South Korea's hotel industry, is making a bold move with the launch of its new high-end brand, The Grand Lotte, nine years after the introduction of its luxury brand, Signiel. The flagship hotel, The Grand Lotte Seoul, will open on August 14 following a major renovation of the original Lotte Hotel Seoul, which first opened in 1979. This transformation is part of Lotte Hotels and Resorts' strategic plan to diversify its brand portfolio and target the global luxury market. Recently, global hotel chains have been further segmenting their luxury brands to precisely target specific customer demographics. Lotte Hotels and Resorts has built a robust portfolio, including the landmark luxury brand Signiel, the upscale Lotte Hotel, the lifestyle brand L7, and the business-oriented Lotte City Hotel. The Grand Lotte, the newest addition, aims to offer a higher level of sophistication and value based on Lotte's 47 years of history and operational expertise. The brand seeks to differentiate itself among the plethora of five-star hotels and create synergy with Signiel to comprehensively meet high-end demand. Its brand philosophy, described as 'a symbol of timeless elegance and sophistication,' reflects a commitment to maintaining the essence of classic luxury while incorporating modern sensibilities. However, a long history can be a double-edged sword. While 47 years provide an unmatched heritage, there is a risk of appearing outdated if the brand fails to keep pace with rapid market trends. The success of The Grand Lotte will depend on overcoming this dilemma and creating an innovative hospitality experience. To achieve this, Lotte has meticulously refined its brand identity. The traditional knot-tying technique has been modernly reinterpreted, and a monogram combining the English initials G and L has been created to visualize the brand's elegance and hospitality philosophy. The rooms at The Grand Lotte Seoul, set to debut in August, will feature designs that blend French luxury craftsmanship with Korean aesthetic sensibilities. Importantly, the focus is on innovation in the brand's soft elements, beyond just hardware changes. The brand philosophy must be consistently communicated at every customer touchpoint. From room design to modern interpretations of traditional uniforms, signature desserts, floral styling, and custom-developed scents, the integrated brand experience will be crucial in distinguishing The Grand Lotte from existing Lotte Hotel brands. The launch of The Grand Lotte Seoul is poised to be a significant moment for the urban luxury hotel market this summer, as well as for attracting global high-end tourists visiting Korea. To celebrate the brand's debut, a special time sale event called 'The Grand Festa' will run from June 24 to 30, providing insight into market reactions. The stay period will be from July 1 to September 30, with renovated rooms available starting August 14. The promotional offerings include three packages: room-only, breakfast-inclusive, and lounge access. Each package features common perks favored by luxury travelers, such as a complimentary bottle of wine, a custom hand wash, and late check-out, aimed at boosting initial bookings. Lotte Hotels and Resorts plans to expand its presence in key global cities, starting with The Grand Lotte Seoul. After proving the potential of Korean luxury with Signiel, the industry is keenly watching how Lotte will reshape the global luxury hospitality landscape with The Grand Lotte, drawing on its 47 years of expertise.* This article has been translated by AI. 2026-06-24 14:12:00

Lotte Hotels Expands Luxury Portfolio with The Grand Lotte The global luxury hotel market is becoming increasingly competitive. Moving beyond the past focus on opulent hardware, the industry now emphasizes 'hyper-personalization' to meet the diverse tastes and experiences of customers. In this context, Lotte Hotels and Resorts, a leader in South Korea's hotel industry, is making a bold move with the launch of its new high-end brand, The Grand Lotte, nine years after the introduction of its luxury brand, Signiel. The flagship hotel, The Grand Lotte Seoul, will open on August 14 following a major renovation of the original Lotte Hotel Seoul, which first opened in 1979. This transformation is part of Lotte Hotels and Resorts' strategic plan to diversify its brand portfolio and target the global luxury market. Recently, global hotel chains have been further segmenting their luxury brands to precisely target specific customer demographics. Lotte Hotels and Resorts has built a robust portfolio, including the landmark luxury brand Signiel, the upscale Lotte Hotel, the lifestyle brand L7, and the business-oriented Lotte City Hotel. The Grand Lotte, the newest addition, aims to offer a higher level of sophistication and value based on Lotte's 47 years of history and operational expertise. The brand seeks to differentiate itself among the plethora of five-star hotels and create synergy with Signiel to comprehensively meet high-end demand. Its brand philosophy, described as 'a symbol of timeless elegance and sophistication,' reflects a commitment to maintaining the essence of classic luxury while incorporating modern sensibilities. However, a long history can be a double-edged sword. While 47 years provide an unmatched heritage, there is a risk of appearing outdated if the brand fails to keep pace with rapid market trends. The success of The Grand Lotte will depend on overcoming this dilemma and creating an innovative hospitality experience. To achieve this, Lotte has meticulously refined its brand identity. The traditional knot-tying technique has been modernly reinterpreted, and a monogram combining the English initials G and L has been created to visualize the brand's elegance and hospitality philosophy. The rooms at The Grand Lotte Seoul, set to debut in August, will feature designs that blend French luxury craftsmanship with Korean aesthetic sensibilities. Importantly, the focus is on innovation in the brand's soft elements, beyond just hardware changes. The brand philosophy must be consistently communicated at every customer touchpoint. From room design to modern interpretations of traditional uniforms, signature desserts, floral styling, and custom-developed scents, the integrated brand experience will be crucial in distinguishing The Grand Lotte from existing Lotte Hotel brands. The launch of The Grand Lotte Seoul is poised to be a significant moment for the urban luxury hotel market this summer, as well as for attracting global high-end tourists visiting Korea. To celebrate the brand's debut, a special time sale event called 'The Grand Festa' will run from June 24 to 30, providing insight into market reactions. The stay period will be from July 1 to September 30, with renovated rooms available starting August 14. The promotional offerings include three packages: room-only, breakfast-inclusive, and lounge access. Each package features common perks favored by luxury travelers, such as a complimentary bottle of wine, a custom hand wash, and late check-out, aimed at boosting initial bookings. Lotte Hotels and Resorts plans to expand its presence in key global cities, starting with The Grand Lotte Seoul. After proving the potential of Korean luxury with Signiel, the industry is keenly watching how Lotte will reshape the global luxury hospitality landscape with The Grand Lotte, drawing on its 47 years of expertise.* This article has been translated by AI. 2026-06-24 14:12:00 -

KOSPI Attempts to Stabilize Above 8300 as Samsung Electronics Surges 7% The KOSPI index rose slightly on June 24, recovering from a sharp decline the previous day and trading above the 8300 mark. According to the Korea Exchange, as of 1:55 PM, the KOSPI was trading at 8,339.05, up 124.45 points (1.52%) from the previous trading day. The index initially rose by 125.95 points (1.86%) and even increased by as much as 373.68 points (4.55%) at one point. At the same time, individual and institutional investors were net buyers in the securities market, purchasing 2.02 trillion won and 2.05 trillion won, respectively. Foreign investors, however, were net sellers, offloading 4.20 trillion won worth of shares. Among the top market capitalizations in the KOSPI, Samsung Electronics saw a significant increase of 7.9%. In contrast, SK Hynix experienced a decline of 0.68%. Other gainers included Samsung C&T (7.69%), Samsung Biologics (6.52%), Doosan Enerbility (2.02%), Hanwha Aerospace (1.21%), and Samsung Life (0.71%). On the downside, SK Square (-5.35%), Samsung Electro-Mechanics (-0.75%), Hyundai Motor (-0.59%), and HD Hyundai Heavy Industries (-0.17%) were among the decliners. Meanwhile, the KOSDAQ index was trading at 902.08, up 10.56 points (1.18%) from the previous session. The KOSDAQ index also opened with a gain of 13.61 points (1.53%). In the KOSDAQ market, individual and foreign investors were net sellers, with sales of 252.7 billion won and 34.6 billion won, respectively, while institutions were net buyers, purchasing 274.6 billion won. Most of the top stocks in the KOSDAQ showed an upward trend. Alteogen led the gains with an increase of 10.81%, followed by Kolon TissueGene (5.99%), HLB (5.26%), EcoPro (4.85%), Rainbow Robotics (2.19%), Iot Technics (1.96%), EcoPro BM (1.52%), and JUSUNG Engineering (0.05%). However, Reno Industrial (-0.94%) and Wonik IPS (-1.20%) saw declines. Kang Jin-hyuk, a researcher at Shinhan Investment Corp, noted, "The KOSPI rebounded as bargain hunting emerged following the previous day's shock, leading to a recovery in large-cap stocks." He added, "Despite some adjustments in certain small and medium-sized enterprises in the KOSDAQ market, major biotech stocks surged, driving the index upward."* This article has been translated by AI. 2026-06-24 14:12:00

KOSPI Attempts to Stabilize Above 8300 as Samsung Electronics Surges 7% The KOSPI index rose slightly on June 24, recovering from a sharp decline the previous day and trading above the 8300 mark. According to the Korea Exchange, as of 1:55 PM, the KOSPI was trading at 8,339.05, up 124.45 points (1.52%) from the previous trading day. The index initially rose by 125.95 points (1.86%) and even increased by as much as 373.68 points (4.55%) at one point. At the same time, individual and institutional investors were net buyers in the securities market, purchasing 2.02 trillion won and 2.05 trillion won, respectively. Foreign investors, however, were net sellers, offloading 4.20 trillion won worth of shares. Among the top market capitalizations in the KOSPI, Samsung Electronics saw a significant increase of 7.9%. In contrast, SK Hynix experienced a decline of 0.68%. Other gainers included Samsung C&T (7.69%), Samsung Biologics (6.52%), Doosan Enerbility (2.02%), Hanwha Aerospace (1.21%), and Samsung Life (0.71%). On the downside, SK Square (-5.35%), Samsung Electro-Mechanics (-0.75%), Hyundai Motor (-0.59%), and HD Hyundai Heavy Industries (-0.17%) were among the decliners. Meanwhile, the KOSDAQ index was trading at 902.08, up 10.56 points (1.18%) from the previous session. The KOSDAQ index also opened with a gain of 13.61 points (1.53%). In the KOSDAQ market, individual and foreign investors were net sellers, with sales of 252.7 billion won and 34.6 billion won, respectively, while institutions were net buyers, purchasing 274.6 billion won. Most of the top stocks in the KOSDAQ showed an upward trend. Alteogen led the gains with an increase of 10.81%, followed by Kolon TissueGene (5.99%), HLB (5.26%), EcoPro (4.85%), Rainbow Robotics (2.19%), Iot Technics (1.96%), EcoPro BM (1.52%), and JUSUNG Engineering (0.05%). However, Reno Industrial (-0.94%) and Wonik IPS (-1.20%) saw declines. Kang Jin-hyuk, a researcher at Shinhan Investment Corp, noted, "The KOSPI rebounded as bargain hunting emerged following the previous day's shock, leading to a recovery in large-cap stocks." He added, "Despite some adjustments in certain small and medium-sized enterprises in the KOSDAQ market, major biotech stocks surged, driving the index upward."* This article has been translated by AI. 2026-06-24 14:12:00 -

Reuters: SK Hynix Poised to Surpass Samsung with HBM Leadership Reuters has highlighted SK Hynix's achievements in the artificial intelligence (AI) semiconductor market, noting that long-term investments in high-bandwidth memory (HBM), once considered a niche product, have transformed the company's standing. On June 24, Reuters reported that "SK Hynix has surpassed Samsung Electronics to become the top company by market capitalization on the domestic stock exchange, thanks to over a decade of investment in HBM." When SK Group acquired Hynix in 2012, many viewed the decision as risky. However, the company's early lead in HBM has coincided with a surge in demand for AI semiconductors. HBM is a type of memory semiconductor that stacks multiple DRAM chips vertically to enhance data processing speeds. Initially categorized as a product not widely used by data center customers, it has now become an essential component for AI accelerators, leading to a dramatic increase in demand. In 2014, SK Hynix launched the world's first HBM product in collaboration with AMD. However, the company faced setbacks with its second-generation HBM products, falling behind Samsung Electronics in the late 2010s. Internally, discussions arose about whether to halt HBM development. Instead of withdrawing, SK Hynix opted for additional investments, anticipating a rise in demand from Nvidia. The company invested 880 billion won in expanding its packaging facilities in Icheon and other locations. Initially, these investments proved burdensome. In 2019, demand from Nvidia and cryptocurrency mining companies declined, leading to lower utilization rates at these facilities. Shin Dae-yong, a former SK Hynix executive who led HBM development, told Reuters, "In 2019, it was a headache; it seemed useless at the time." A turning point came in 2022 with the launch of OpenAI's ChatGPT. The surge in generative AI led to a significant increase in demand for Nvidia's AI accelerators, which in turn boosted the need for HBM. Reuters noted that "SK Hynix was already prepared in terms of performance and production capacity, and it has now established itself as a key HBM supplier for Nvidia." HBM has become a stepping stone for SK Hynix to quickly recover from a downturn in the memory market. Despite reporting an annual operating loss of 7.73 trillion won in 2023 due to a sharp decline in memory prices, the company is projected to achieve record operating profits in 2024. In 2025, it even briefly held the title of the world's top DRAM producer. Samsung Electronics is currently pursuing a stronger position in the HBM market. Reuters explained, "While Samsung produces the base chips used in HBM in-house, SK Hynix is collaborating with TSMC to enhance performance starting with the next-generation HBM4."* This article has been translated by AI. 2026-06-24 14:08:00

Reuters: SK Hynix Poised to Surpass Samsung with HBM Leadership Reuters has highlighted SK Hynix's achievements in the artificial intelligence (AI) semiconductor market, noting that long-term investments in high-bandwidth memory (HBM), once considered a niche product, have transformed the company's standing. On June 24, Reuters reported that "SK Hynix has surpassed Samsung Electronics to become the top company by market capitalization on the domestic stock exchange, thanks to over a decade of investment in HBM." When SK Group acquired Hynix in 2012, many viewed the decision as risky. However, the company's early lead in HBM has coincided with a surge in demand for AI semiconductors. HBM is a type of memory semiconductor that stacks multiple DRAM chips vertically to enhance data processing speeds. Initially categorized as a product not widely used by data center customers, it has now become an essential component for AI accelerators, leading to a dramatic increase in demand. In 2014, SK Hynix launched the world's first HBM product in collaboration with AMD. However, the company faced setbacks with its second-generation HBM products, falling behind Samsung Electronics in the late 2010s. Internally, discussions arose about whether to halt HBM development. Instead of withdrawing, SK Hynix opted for additional investments, anticipating a rise in demand from Nvidia. The company invested 880 billion won in expanding its packaging facilities in Icheon and other locations. Initially, these investments proved burdensome. In 2019, demand from Nvidia and cryptocurrency mining companies declined, leading to lower utilization rates at these facilities. Shin Dae-yong, a former SK Hynix executive who led HBM development, told Reuters, "In 2019, it was a headache; it seemed useless at the time." A turning point came in 2022 with the launch of OpenAI's ChatGPT. The surge in generative AI led to a significant increase in demand for Nvidia's AI accelerators, which in turn boosted the need for HBM. Reuters noted that "SK Hynix was already prepared in terms of performance and production capacity, and it has now established itself as a key HBM supplier for Nvidia." HBM has become a stepping stone for SK Hynix to quickly recover from a downturn in the memory market. Despite reporting an annual operating loss of 7.73 trillion won in 2023 due to a sharp decline in memory prices, the company is projected to achieve record operating profits in 2024. In 2025, it even briefly held the title of the world's top DRAM producer. Samsung Electronics is currently pursuing a stronger position in the HBM market. Reuters explained, "While Samsung produces the base chips used in HBM in-house, SK Hynix is collaborating with TSMC to enhance performance starting with the next-generation HBM4."* This article has been translated by AI. 2026-06-24 14:08:00 -

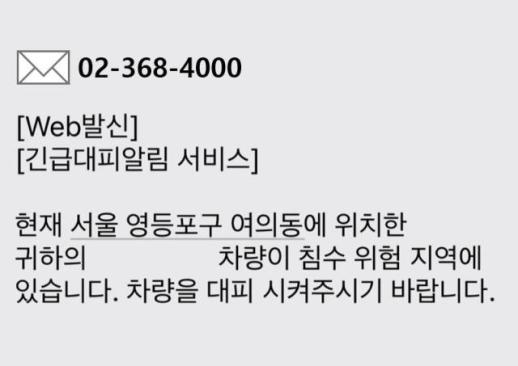

Move Your Car if You Receive Flood Risk Alerts, Insurance Development Institute Says As summer approaches, bringing increased heavy rainfall and typhoons, the Insurance Development Institute is implementing an emergency evacuation alert service to help quickly relocate vehicles parked in flood-risk areas. The Insurance Development Institute announced on June 24 that it has been operating the 'Emergency Evacuation Alert Service' since June of last year in collaboration with non-life insurance companies to prevent vehicle flood damage. This service allows patrol officers from insurance companies, local governments, and police to input vehicle license plate numbers into a system for cars parked in flood-risk areas. Owners receive evacuation notifications via text message (SMS), voice alerts, and KakaoTalk. According to the Insurance Development Institute, there were a total of 35,011 vehicle flood incidents reported by 12 non-life insurance companies from 2021 to 2025. Of these, 33,490 incidents occurred between July and October, accounting for 95.7% of the total. The service began around June 2024. As of the end of May this year, there were 2,503 users, and among the 2,802 vehicles that received evacuation alerts last year, only 9 were involved in flood incidents. The Insurance Development Institute urged users to verify the official sender number and KakaoTalk authentication channel to avoid mistaking emergency evacuation alerts for phishing scams or spam. The evacuation alert messages do not contain internet addresses (URLs) or app installation links.* This article has been translated by AI. 2026-06-24 14:08:00

Move Your Car if You Receive Flood Risk Alerts, Insurance Development Institute Says As summer approaches, bringing increased heavy rainfall and typhoons, the Insurance Development Institute is implementing an emergency evacuation alert service to help quickly relocate vehicles parked in flood-risk areas. The Insurance Development Institute announced on June 24 that it has been operating the 'Emergency Evacuation Alert Service' since June of last year in collaboration with non-life insurance companies to prevent vehicle flood damage. This service allows patrol officers from insurance companies, local governments, and police to input vehicle license plate numbers into a system for cars parked in flood-risk areas. Owners receive evacuation notifications via text message (SMS), voice alerts, and KakaoTalk. According to the Insurance Development Institute, there were a total of 35,011 vehicle flood incidents reported by 12 non-life insurance companies from 2021 to 2025. Of these, 33,490 incidents occurred between July and October, accounting for 95.7% of the total. The service began around June 2024. As of the end of May this year, there were 2,503 users, and among the 2,802 vehicles that received evacuation alerts last year, only 9 were involved in flood incidents. The Insurance Development Institute urged users to verify the official sender number and KakaoTalk authentication channel to avoid mistaking emergency evacuation alerts for phishing scams or spam. The evacuation alert messages do not contain internet addresses (URLs) or app installation links.* This article has been translated by AI. 2026-06-24 14:08:00 -

North Korean soldier crosses border to defect to South Korea SEOUL, June 24 (AJP) - A North Korean soldier crossed the military demarcation line overnight, the Joint Chiefs of Staff (JCS) here said on Wednesday. "The soldier has been investigated by relevant agencies," the JCS said, without providing further details. But he was reportedly found to have expressed an intention to defect. The last time a North Korean soldier crossed the heavily fortified border to defect was in October last year. That followed two separate defections by North Korean men in July, bringing the total number of North Korean defectors since President Lee Jae Myung took office to four. By the end of 2023, a total of 34,078 North Koreans — 9,542 men and 24,536 women — had escaped to the South. The number of defection cases has recently shown signs of a slight uptick, with 43 defectors arriving in the first quarter of last year after a sharp decline during the coronavirus pandemic, when North Korea closed its borders to the outside world. 2026-06-24 14:07:59

North Korean soldier crosses border to defect to South Korea SEOUL, June 24 (AJP) - A North Korean soldier crossed the military demarcation line overnight, the Joint Chiefs of Staff (JCS) here said on Wednesday. "The soldier has been investigated by relevant agencies," the JCS said, without providing further details. But he was reportedly found to have expressed an intention to defect. The last time a North Korean soldier crossed the heavily fortified border to defect was in October last year. That followed two separate defections by North Korean men in July, bringing the total number of North Korean defectors since President Lee Jae Myung took office to four. By the end of 2023, a total of 34,078 North Koreans — 9,542 men and 24,536 women — had escaped to the South. The number of defection cases has recently shown signs of a slight uptick, with 43 defectors arriving in the first quarter of last year after a sharp decline during the coronavirus pandemic, when North Korea closed its borders to the outside world. 2026-06-24 14:07:59 -

Government Inspects Export Challenges for Food Companies in Jeonbuk, Enhances K-Food Support The government is addressing the export challenges faced by food companies in the Jeonbuk region to expand K-Food exports. On June 24, the Ministry of Economy and Finance's Export Plus Support Team announced that it would visit Jeonbuk for two days to hold a meeting with food export companies and a financial support briefing. The meeting, held at the Korea Food Industry Cluster Promotion Agency in Iksan, included representatives from the Export Plus Support Team, the Ministry of Trade, Industry and Energy's Overseas Certification Support Team, Iksan City, the Korea Trade-Investment Promotion Agency (KOTRA), the Small and Medium Business Administration, the Korea International Trade Association, and the Korea Export Insurance Corporation, along with food export companies. During the meeting, companies raised concerns about rising export logistics costs, the burden of responding to country-specific certifications and regulations, developing overseas markets, post-management of international exhibitions, and a lack of information on overseas certifications. In response, the government and export support agencies introduced various support programs, including export and logistics vouchers, policy funding, overseas branch establishment projects, buyer matching services, and mentoring for overseas certifications. Yoo Beom-min, deputy head of the Export Plus Support Team, stated, "K-Food, alongside K-content, is a representative export industry gaining attention in the global market. The government and export support agencies will work as a united team to resolve the challenges faced by companies and actively support the expansion of K-Food exports." On June 25, the support team plans to hold a financial support briefing for export companies in Jeonju, in collaboration with the Korea Export-Import Bank, IBK Industrial Bank, Korea Export Insurance Corporation, Credit Guarantee Fund, and Technology Guarantee Fund, to introduce financial support programs such as exchange rate fluctuation insurance and preferential interest rate loans. Additionally, the team will hold a regional export promotion cooperation meeting with Jeonbuk Province to discuss support measures for export companies. The support team aims to establish cooperative channels with local governments in nine provinces nationwide by the end of this year.* This article has been translated by AI. 2026-06-24 14:04:00

Government Inspects Export Challenges for Food Companies in Jeonbuk, Enhances K-Food Support The government is addressing the export challenges faced by food companies in the Jeonbuk region to expand K-Food exports. On June 24, the Ministry of Economy and Finance's Export Plus Support Team announced that it would visit Jeonbuk for two days to hold a meeting with food export companies and a financial support briefing. The meeting, held at the Korea Food Industry Cluster Promotion Agency in Iksan, included representatives from the Export Plus Support Team, the Ministry of Trade, Industry and Energy's Overseas Certification Support Team, Iksan City, the Korea Trade-Investment Promotion Agency (KOTRA), the Small and Medium Business Administration, the Korea International Trade Association, and the Korea Export Insurance Corporation, along with food export companies. During the meeting, companies raised concerns about rising export logistics costs, the burden of responding to country-specific certifications and regulations, developing overseas markets, post-management of international exhibitions, and a lack of information on overseas certifications. In response, the government and export support agencies introduced various support programs, including export and logistics vouchers, policy funding, overseas branch establishment projects, buyer matching services, and mentoring for overseas certifications. Yoo Beom-min, deputy head of the Export Plus Support Team, stated, "K-Food, alongside K-content, is a representative export industry gaining attention in the global market. The government and export support agencies will work as a united team to resolve the challenges faced by companies and actively support the expansion of K-Food exports." On June 25, the support team plans to hold a financial support briefing for export companies in Jeonju, in collaboration with the Korea Export-Import Bank, IBK Industrial Bank, Korea Export Insurance Corporation, Credit Guarantee Fund, and Technology Guarantee Fund, to introduce financial support programs such as exchange rate fluctuation insurance and preferential interest rate loans. Additionally, the team will hold a regional export promotion cooperation meeting with Jeonbuk Province to discuss support measures for export companies. The support team aims to establish cooperative channels with local governments in nine provinces nationwide by the end of this year.* This article has been translated by AI. 2026-06-24 14:04:00 -

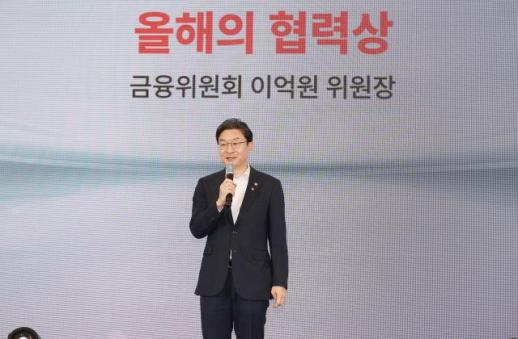

Five Startups Selected for Collaboration with Financial Institutions Five startups providing practical services such as funeral preparation, card spending analysis, policy support fund inquiries, lease risk assessments, and financial AI response verification have been recognized for their collaboration with financial institutions. Lee Ok-yeon, chairman of the Financial Services Commission, attended the "Startup Open Innovation #Financial Sector" award ceremony held at Front One in Mapo, Seoul, on June 24, where he presented awards for exemplary collaborations between startups and financial institutions. The event aimed to identify collaboration needs between startups and financial institutions and to connect them with actual cooperation cases. This year, five startups were selected from a total of 44 proposals submitted by May 18, following a preliminary review. The selected collaborations include: 1) Goi Funeral Research Institute and OK Savings Bank for an IT-based one-stop funeral platform; 2) WhatSub and Shinhan Card for a card data analysis solution; 3) Wello and Kakao Bank for a customized policy support fund platform; 4) TerraFi and Woori Bank for pre-lease risk assessment services; and 5) Tynaps and KB Kookmin Bank for a financial response reliability verification solution. The awarded companies will receive benefits such as workshop support worth up to 3 million won, priority consideration for the D.CAMP placement program, and financial support from partner institutions.* This article has been translated by AI. 2026-06-24 14:00:00

Five Startups Selected for Collaboration with Financial Institutions Five startups providing practical services such as funeral preparation, card spending analysis, policy support fund inquiries, lease risk assessments, and financial AI response verification have been recognized for their collaboration with financial institutions. Lee Ok-yeon, chairman of the Financial Services Commission, attended the "Startup Open Innovation #Financial Sector" award ceremony held at Front One in Mapo, Seoul, on June 24, where he presented awards for exemplary collaborations between startups and financial institutions. The event aimed to identify collaboration needs between startups and financial institutions and to connect them with actual cooperation cases. This year, five startups were selected from a total of 44 proposals submitted by May 18, following a preliminary review. The selected collaborations include: 1) Goi Funeral Research Institute and OK Savings Bank for an IT-based one-stop funeral platform; 2) WhatSub and Shinhan Card for a card data analysis solution; 3) Wello and Kakao Bank for a customized policy support fund platform; 4) TerraFi and Woori Bank for pre-lease risk assessment services; and 5) Tynaps and KB Kookmin Bank for a financial response reliability verification solution. The awarded companies will receive benefits such as workshop support worth up to 3 million won, priority consideration for the D.CAMP placement program, and financial support from partner institutions.* This article has been translated by AI. 2026-06-24 14:00:00