Journalist

Kwon Ga-rim

hidden@ajunews.com

-

FIU Adjusts Reporting Requirements for Virtual Asset Transfers Domestic virtual asset businesses will now manage their own anti-money laundering risks instead of being required to report all transactions involving over 10 million won ($7,500) to financial authorities. On June 5, the Financial Intelligence Unit (FIU), under the Financial Services Commission, met with representatives from virtual asset exchanges to gather industry feedback on proposed amendments to the Enforcement Decree and supervisory regulations of the Special Financial Act. The initial proposal, announced in March, mandated that domestic businesses report any transfers of virtual assets exceeding 10 million won to the FIU, regardless of the transaction's risk level. However, the virtual asset industry expressed concerns that mandatory reporting for all transactions over this threshold would lead to operational chaos. In response, the FIU revised its approach, recognizing that enforcing blanket reporting based solely on transaction amounts could result in businesses submitting reports without proper risk assessments.* This article has been translated by AI. 2026-06-05 16:21:00

FIU Adjusts Reporting Requirements for Virtual Asset Transfers Domestic virtual asset businesses will now manage their own anti-money laundering risks instead of being required to report all transactions involving over 10 million won ($7,500) to financial authorities. On June 5, the Financial Intelligence Unit (FIU), under the Financial Services Commission, met with representatives from virtual asset exchanges to gather industry feedback on proposed amendments to the Enforcement Decree and supervisory regulations of the Special Financial Act. The initial proposal, announced in March, mandated that domestic businesses report any transfers of virtual assets exceeding 10 million won to the FIU, regardless of the transaction's risk level. However, the virtual asset industry expressed concerns that mandatory reporting for all transactions over this threshold would lead to operational chaos. In response, the FIU revised its approach, recognizing that enforcing blanket reporting based solely on transaction amounts could result in businesses submitting reports without proper risk assessments.* This article has been translated by AI. 2026-06-05 16:21:00 -

KB Financial Group Establishes $8.5 Million Cooperative Fund with Ministry of SMEs KB Financial Group announced on June 5 that it has established a cooperative fund worth 10 billion won (approximately $8.5 million) in collaboration with the Ministry of SMEs and Startups and the Korea Federation of Small and Medium Enterprises.The fund expands the previous focus on large corporate supply chains to include small and medium-sized enterprises (SMEs) and micro-enterprises.KB Financial plans to support the local economy through investments of 2 billion won in artificial intelligence transformation (AX), 3 billion won in green transformation (GX), and 2 billion won in safety transformation (SX).Additionally, 3 billion won will be contributed to a cooperative fund aimed at impact investments in community-based social economy enterprises and social ventures.Yang Jong-hee, Chairman of KB Financial, stated, "We will continue to contribute to the sustainable growth of small businesses and micro-enterprises, as well as the revitalization of the local economy, based on our social responsibility in finance."KB Financial also plans to invest 10.5 trillion won in support for vulnerable groups and 6.5 trillion won for small businesses and self-employed individuals by 2030.* This article has been translated by AI. 2026-06-05 15:33:00

KB Financial Group Establishes $8.5 Million Cooperative Fund with Ministry of SMEs KB Financial Group announced on June 5 that it has established a cooperative fund worth 10 billion won (approximately $8.5 million) in collaboration with the Ministry of SMEs and Startups and the Korea Federation of Small and Medium Enterprises.The fund expands the previous focus on large corporate supply chains to include small and medium-sized enterprises (SMEs) and micro-enterprises.KB Financial plans to support the local economy through investments of 2 billion won in artificial intelligence transformation (AX), 3 billion won in green transformation (GX), and 2 billion won in safety transformation (SX).Additionally, 3 billion won will be contributed to a cooperative fund aimed at impact investments in community-based social economy enterprises and social ventures.Yang Jong-hee, Chairman of KB Financial, stated, "We will continue to contribute to the sustainable growth of small businesses and micro-enterprises, as well as the revitalization of the local economy, based on our social responsibility in finance."KB Financial also plans to invest 10.5 trillion won in support for vulnerable groups and 6.5 trillion won for small businesses and self-employed individuals by 2030.* This article has been translated by AI. 2026-06-05 15:33:00 -

Hanwha Aerospace Faces Financial Scrutiny Under New Safety Regulations Financial authorities are set to implement financial penalties on companies violating the Serious Accident Punishment Act, with Hanwha Aerospace potentially being the first major case under this new regulation. According to financial sector sources on June 5, the Financial Commission has mandated that banks incorporate companies' serious accident histories into their credit assessments starting this year. This initiative follows President Lee Jae-myung's strong criticism of Posco E&C last year after a fatal accident, during which he called for restrictions on bank loans to such companies. As a result, the explosion at Hanwha Aerospace's Daejeon facility is being closely watched as a potential first instance of credit restrictions in the financial sector. In the first quarter of this year, Hanwha Aerospace reported short-term borrowings totaling 6.89 trillion won, with approximately 5.75 trillion won, or 83%, sourced from domestic banks. Major banks such as KB Kookmin Bank, Shinhan Bank, Hana Bank, Woori Bank, NH Nonghyup Bank, Industrial Bank of Korea, Export-Import Bank of Korea, Busan Bank, and iM Bank have provided operational and facility funding to Hanwha Aerospace. The company also has about 3.60 trillion won in long-term borrowings from these banks. While there has been no administrative or judicial ruling against Hanwha Aerospace yet, creditor banks are closely monitoring the circumstances of the accident and any potential legal liabilities. Banks evaluate both financial and non-financial factors when assessing corporate credit. Although financial metrics typically carry more weight, the increasing emphasis on environmental, social, and governance (ESG) management has led to a growing importance of non-financial assessments. Following President Lee's demands for stricter financial penalties on accident-prone companies last year, banks are now monitoring Hanwha Aerospace's compliance with the Serious Accident Punishment Act. If Hanwha Aerospace is classified as a company violating the Serious Accident Punishment Act, it could face stricter loan assessments, reduced credit limits, more rigorous evaluations for loan extensions, and adjustments in interest rates. A financial sector source stated, "While we need to consider financial factors, we cannot immediately withdraw loans. However, the non-financial assessments could negatively impact their standing. If it becomes clear that the facility has experienced frequent accidents and safety inspections have not been adequately conducted, it could lead to a downgrade in credit ratings and, in the worst-case scenario, loan withdrawals." However, there are few precedents for applying the financial penalties under the Serious Accident Punishment Act to large corporations, making this incident a crucial test of the regulation's effectiveness. Another financial sector source noted, "If we were to hastily withdraw loans, it could threaten the survival of partner companies. We will carefully consider the severity of the situation and the potential for improvement while strengthening our credit assessments." A representative from the financial authorities remarked, "Once a public announcement confirms a serious accident, banks' credit assessments should be strengthened." 2026-06-05 15:18:00

Hanwha Aerospace Faces Financial Scrutiny Under New Safety Regulations Financial authorities are set to implement financial penalties on companies violating the Serious Accident Punishment Act, with Hanwha Aerospace potentially being the first major case under this new regulation. According to financial sector sources on June 5, the Financial Commission has mandated that banks incorporate companies' serious accident histories into their credit assessments starting this year. This initiative follows President Lee Jae-myung's strong criticism of Posco E&C last year after a fatal accident, during which he called for restrictions on bank loans to such companies. As a result, the explosion at Hanwha Aerospace's Daejeon facility is being closely watched as a potential first instance of credit restrictions in the financial sector. In the first quarter of this year, Hanwha Aerospace reported short-term borrowings totaling 6.89 trillion won, with approximately 5.75 trillion won, or 83%, sourced from domestic banks. Major banks such as KB Kookmin Bank, Shinhan Bank, Hana Bank, Woori Bank, NH Nonghyup Bank, Industrial Bank of Korea, Export-Import Bank of Korea, Busan Bank, and iM Bank have provided operational and facility funding to Hanwha Aerospace. The company also has about 3.60 trillion won in long-term borrowings from these banks. While there has been no administrative or judicial ruling against Hanwha Aerospace yet, creditor banks are closely monitoring the circumstances of the accident and any potential legal liabilities. Banks evaluate both financial and non-financial factors when assessing corporate credit. Although financial metrics typically carry more weight, the increasing emphasis on environmental, social, and governance (ESG) management has led to a growing importance of non-financial assessments. Following President Lee's demands for stricter financial penalties on accident-prone companies last year, banks are now monitoring Hanwha Aerospace's compliance with the Serious Accident Punishment Act. If Hanwha Aerospace is classified as a company violating the Serious Accident Punishment Act, it could face stricter loan assessments, reduced credit limits, more rigorous evaluations for loan extensions, and adjustments in interest rates. A financial sector source stated, "While we need to consider financial factors, we cannot immediately withdraw loans. However, the non-financial assessments could negatively impact their standing. If it becomes clear that the facility has experienced frequent accidents and safety inspections have not been adequately conducted, it could lead to a downgrade in credit ratings and, in the worst-case scenario, loan withdrawals." However, there are few precedents for applying the financial penalties under the Serious Accident Punishment Act to large corporations, making this incident a crucial test of the regulation's effectiveness. Another financial sector source noted, "If we were to hastily withdraw loans, it could threaten the survival of partner companies. We will carefully consider the severity of the situation and the potential for improvement while strengthening our credit assessments." A representative from the financial authorities remarked, "Once a public announcement confirms a serious accident, banks' credit assessments should be strengthened." 2026-06-05 15:18:00 -

KB Kookmin Bank Launches 'KB Veterans Benefit Remittance Check' Service with No Fees KB Kookmin Bank announced on June 5 that it will launch the 'KB Veterans Benefit Remittance Check' service in honor of National Defense and Veterans Month.This service is designed to assist veterans living abroad who do not have local bank accounts, allowing them to receive and use foreign currency remittance checks directly.The Ministry of Veterans Affairs plans to transition to a remittance payment method for veterans living overseas starting in 2027 to enhance the convenience of benefit receipt. However, to minimize the inconvenience for some beneficiaries who find it difficult to open and use overseas accounts, KB Kookmin Bank has collaborated with the ministry to introduce the KB Veterans Benefit Remittance Check service.To reduce the burden on customers using this service, KB Kookmin Bank will waive all fees associated with issuing remittance checks. This initiative aims to make it easier for national merit recipients and their families living abroad to receive their benefits.A representative from KB Kookmin Bank stated, "This service has been established to ensure that veterans living abroad can receive their benefits more conveniently and securely. We will continue to contribute to creating social value through various inclusive financial practices for those who have dedicated themselves to the nation."In addition to launching this new service, KB Kookmin Bank is also participating in volunteer activities at the National Cemetery in Seoul to commemorate National Defense and Veterans Month. 2026-06-05 10:03:00

KB Kookmin Bank Launches 'KB Veterans Benefit Remittance Check' Service with No Fees KB Kookmin Bank announced on June 5 that it will launch the 'KB Veterans Benefit Remittance Check' service in honor of National Defense and Veterans Month.This service is designed to assist veterans living abroad who do not have local bank accounts, allowing them to receive and use foreign currency remittance checks directly.The Ministry of Veterans Affairs plans to transition to a remittance payment method for veterans living overseas starting in 2027 to enhance the convenience of benefit receipt. However, to minimize the inconvenience for some beneficiaries who find it difficult to open and use overseas accounts, KB Kookmin Bank has collaborated with the ministry to introduce the KB Veterans Benefit Remittance Check service.To reduce the burden on customers using this service, KB Kookmin Bank will waive all fees associated with issuing remittance checks. This initiative aims to make it easier for national merit recipients and their families living abroad to receive their benefits.A representative from KB Kookmin Bank stated, "This service has been established to ensure that veterans living abroad can receive their benefits more conveniently and securely. We will continue to contribute to creating social value through various inclusive financial practices for those who have dedicated themselves to the nation."In addition to launching this new service, KB Kookmin Bank is also participating in volunteer activities at the National Cemetery in Seoul to commemorate National Defense and Veterans Month. 2026-06-05 10:03:00 -

Bithumb Recognized by Police for Preventing $8 Million in Phishing Scams Bithumb announced on June 5 that it received a certificate of appreciation from the National Police Agency for its contributions to preventing phishing scams involving virtual assets.Since March, Bithumb has been operating a proactive collaboration system that connects information on malicious app installers provided by the police's Integrated Response Team with member data to register users as 'at risk.' This system has enabled Bithumb to notify the police in real-time about 66 suspicious transactions, preventing approximately 800 million won (about $600,000) in phishing losses.One notable case involved a customer who attempted to buy and withdraw virtual assets worth 150 million won (about $112,000) after being deceived by criminals impersonating institutions. Bithumb collaborated with the police to block the transaction. Additionally, the platform detected another suspicious transaction where a user was misled into opening a new account and attempting to transfer 88.9 million won (about $66,000), thus preventing further losses.Bithumb plans to strengthen its data-sharing system with the police regarding phishing crimes while enhancing its security measures and investor protection activities.Currently, Bithumb has implemented a security system that automatically restricts transactions if a remote control app is detected during app operation. The company is also developing a system that automatically issues warnings and limits service use upon detecting malicious apps, while maintaining customer assets at a higher ratio than legal standards to combat fraud effectively.Byun Seung-moo, Bithumb's compliance officer, stated, "Bithumb has continuously enhanced its security system to detect phishing site lure activities and suspicious transactions early, ensuring a safe virtual asset trading environment. In the future, we plan to build a faster and more sophisticated response system through collaboration with the National Police Agency, continuously strengthening our user protection capabilities."* This article has been translated by AI. 2026-06-05 08:45:00

Bithumb Recognized by Police for Preventing $8 Million in Phishing Scams Bithumb announced on June 5 that it received a certificate of appreciation from the National Police Agency for its contributions to preventing phishing scams involving virtual assets.Since March, Bithumb has been operating a proactive collaboration system that connects information on malicious app installers provided by the police's Integrated Response Team with member data to register users as 'at risk.' This system has enabled Bithumb to notify the police in real-time about 66 suspicious transactions, preventing approximately 800 million won (about $600,000) in phishing losses.One notable case involved a customer who attempted to buy and withdraw virtual assets worth 150 million won (about $112,000) after being deceived by criminals impersonating institutions. Bithumb collaborated with the police to block the transaction. Additionally, the platform detected another suspicious transaction where a user was misled into opening a new account and attempting to transfer 88.9 million won (about $66,000), thus preventing further losses.Bithumb plans to strengthen its data-sharing system with the police regarding phishing crimes while enhancing its security measures and investor protection activities.Currently, Bithumb has implemented a security system that automatically restricts transactions if a remote control app is detected during app operation. The company is also developing a system that automatically issues warnings and limits service use upon detecting malicious apps, while maintaining customer assets at a higher ratio than legal standards to combat fraud effectively.Byun Seung-moo, Bithumb's compliance officer, stated, "Bithumb has continuously enhanced its security system to detect phishing site lure activities and suspicious transactions early, ensuring a safe virtual asset trading environment. In the future, we plan to build a faster and more sophisticated response system through collaboration with the National Police Agency, continuously strengthening our user protection capabilities."* This article has been translated by AI. 2026-06-05 08:45:00 -

KB Kookmin Bank Launches New Ad Featuring Director Jang Hang-jun and Writer Kim Eun-hee KB Kookmin Bank announced on June 4 that it has released a new advertisement for its senior integrated brand, 'KB Golden Life.' The ad features director Jang Hang-jun and writer Kim Eun-hee, who have been selected as the new models. It tells the warm story of the couple's journey together through difficult times, conveying the message, "With KB Golden Life, everyone can experience their golden years." The tagline, "Let’s make this life even more brilliant with KB Golden Life," reflects the brand's commitment to empathizing with customers' life journeys and supporting their future. The advertisement showcases the 'KB Golden Life Total Care Solution,' which includes: △ Specialized senior consulting and total care services at branches nationwide △ Customized pension products for stable retirement asset management, including retirement pensions △ Tailored asset succession consulting through trust products and gift planning services that include will and inheritance functions △ Information on senior living, caregiving, and nursing services, covering all aspects of asset management, retirement planning, inheritance, gifting, caregiving, and nursing throughout the customer’s life cycle. The campaign consists of several segments, including a couple's version, a segment featuring director Jang Hang-jun, a segment featuring writer Kim Eun-hee, and shorts, with the couple's version set to be released sequentially every Wednesday. A representative from KB Kookmin Bank stated, “We hope KB Golden Life becomes a reliable partner in creating our customers' golden years, just like the story of director Jang Hang-jun and writer Kim Eun-hee. We will continue to expand various services for a richer life for our senior customers.” KB Kookmin Bank has previously established a trustworthy brand image by selecting models such as the K-pop group Aespa (2021), Hearts to Hearts (August 2025), actress Park Eun-bin (since March 2023 as a model), and Choo Young-woo (March 2025). * This article has been translated by AI. 2026-06-04 15:42:00

KB Kookmin Bank Launches New Ad Featuring Director Jang Hang-jun and Writer Kim Eun-hee KB Kookmin Bank announced on June 4 that it has released a new advertisement for its senior integrated brand, 'KB Golden Life.' The ad features director Jang Hang-jun and writer Kim Eun-hee, who have been selected as the new models. It tells the warm story of the couple's journey together through difficult times, conveying the message, "With KB Golden Life, everyone can experience their golden years." The tagline, "Let’s make this life even more brilliant with KB Golden Life," reflects the brand's commitment to empathizing with customers' life journeys and supporting their future. The advertisement showcases the 'KB Golden Life Total Care Solution,' which includes: △ Specialized senior consulting and total care services at branches nationwide △ Customized pension products for stable retirement asset management, including retirement pensions △ Tailored asset succession consulting through trust products and gift planning services that include will and inheritance functions △ Information on senior living, caregiving, and nursing services, covering all aspects of asset management, retirement planning, inheritance, gifting, caregiving, and nursing throughout the customer’s life cycle. The campaign consists of several segments, including a couple's version, a segment featuring director Jang Hang-jun, a segment featuring writer Kim Eun-hee, and shorts, with the couple's version set to be released sequentially every Wednesday. A representative from KB Kookmin Bank stated, “We hope KB Golden Life becomes a reliable partner in creating our customers' golden years, just like the story of director Jang Hang-jun and writer Kim Eun-hee. We will continue to expand various services for a richer life for our senior customers.” KB Kookmin Bank has previously established a trustworthy brand image by selecting models such as the K-pop group Aespa (2021), Hearts to Hearts (August 2025), actress Park Eun-bin (since March 2023 as a model), and Choo Young-woo (March 2025). * This article has been translated by AI. 2026-06-04 15:42:00 -

Loan Rates Rise Again, Vulnerable Borrowers and Small Business Owners on Alert South Korea's Bank of Korea has signaled the start of a tightening cycle, raising concerns among borrowers. With mortgage and credit loan rates already hovering between 6% and 7%, further increases could heighten the risk of defaults, particularly among vulnerable borrowers and small business owners.As of June 2, the five major banks (Kookmin, Shinhan, Hana, Woori, and NH Nonghyup) are offering fixed-rate mortgages with interest rates ranging from 4.34% to 7.32%. Some banks have already seen their lower rates exceed 5%.Market analysts predict that if the Bank of Korea raises the benchmark interest rate by 0.25 percentage points up to three times this year, the upper limit for mortgage rates could surpass 8%. This is due to the correlation between benchmark rate hikes, rising bank bond rates, and increased funding costs, which ultimately affect loan interest rates.The burden is expected to fall heavily on borrowers exposed to interest rate fluctuations. Those who took out loans five years ago during the peak borrowing period with mixed rates and are now switching to variable rates, as well as those with six-month variable loans, are particularly at risk. For instance, a borrower who took out a 400 million won loan at a 5% interest rate with a 30-year equal principal and interest repayment plan would see their monthly payment rise from approximately 2.14 million won to about 2.93 million won if rates increase to 8%, an increase of around 800,000 won.The challenges for vulnerable borrowers are intensifying. The number of individual business owners registered as financial defaulters surged from 67,900 in 2022 to over 120,000 in April this year. The delinquency rate for loans to individual business owners from domestic banks has also reached its highest level in five years. As the economic difficulties for small businesses and self-employed individuals worsen, the number of personal bankruptcy filings has risen to its highest level since 2021.Borrowers with credit loans are also facing uncertainty. Amid a booming stock market, the trend of borrowing to invest, known as 'debt investment,' has led to the highest level of personal credit loan balances at the five major banks since November 2023. The upper limit for credit loan rates at major banks has already reached around 6%, raising concerns about increased default risks if rates continue to rise.Rising interest rates also pose challenges for banks. If borrowers' repayment abilities decline, financial institutions will need to bolster their loss absorption capabilities by increasing provisions for bad debts.A financial industry official stated, "If the defaults among small businesses and self-employed individuals worsen, it could lead to a vicious cycle of domestic economic stagnation. Policy measures are needed to ensure that the impact of interest rate hikes does not disproportionately affect vulnerable borrowers and marginal businesses."* This article has been translated by AI. 2026-06-02 17:06:00

Loan Rates Rise Again, Vulnerable Borrowers and Small Business Owners on Alert South Korea's Bank of Korea has signaled the start of a tightening cycle, raising concerns among borrowers. With mortgage and credit loan rates already hovering between 6% and 7%, further increases could heighten the risk of defaults, particularly among vulnerable borrowers and small business owners.As of June 2, the five major banks (Kookmin, Shinhan, Hana, Woori, and NH Nonghyup) are offering fixed-rate mortgages with interest rates ranging from 4.34% to 7.32%. Some banks have already seen their lower rates exceed 5%.Market analysts predict that if the Bank of Korea raises the benchmark interest rate by 0.25 percentage points up to three times this year, the upper limit for mortgage rates could surpass 8%. This is due to the correlation between benchmark rate hikes, rising bank bond rates, and increased funding costs, which ultimately affect loan interest rates.The burden is expected to fall heavily on borrowers exposed to interest rate fluctuations. Those who took out loans five years ago during the peak borrowing period with mixed rates and are now switching to variable rates, as well as those with six-month variable loans, are particularly at risk. For instance, a borrower who took out a 400 million won loan at a 5% interest rate with a 30-year equal principal and interest repayment plan would see their monthly payment rise from approximately 2.14 million won to about 2.93 million won if rates increase to 8%, an increase of around 800,000 won.The challenges for vulnerable borrowers are intensifying. The number of individual business owners registered as financial defaulters surged from 67,900 in 2022 to over 120,000 in April this year. The delinquency rate for loans to individual business owners from domestic banks has also reached its highest level in five years. As the economic difficulties for small businesses and self-employed individuals worsen, the number of personal bankruptcy filings has risen to its highest level since 2021.Borrowers with credit loans are also facing uncertainty. Amid a booming stock market, the trend of borrowing to invest, known as 'debt investment,' has led to the highest level of personal credit loan balances at the five major banks since November 2023. The upper limit for credit loan rates at major banks has already reached around 6%, raising concerns about increased default risks if rates continue to rise.Rising interest rates also pose challenges for banks. If borrowers' repayment abilities decline, financial institutions will need to bolster their loss absorption capabilities by increasing provisions for bad debts.A financial industry official stated, "If the defaults among small businesses and self-employed individuals worsen, it could lead to a vicious cycle of domestic economic stagnation. Policy measures are needed to ensure that the impact of interest rate hikes does not disproportionately affect vulnerable borrowers and marginal businesses."* This article has been translated by AI. 2026-06-02 17:06:00 -

KakaoBank Expands Personal Business Loans Through Naver Pay KakaoBank announced on June 2 that it will collaborate with Naver Pay to expand support for personal business loans.As part of this partnership, KakaoBank's 'Personal Business Real Estate Loan' product will now be available for comparison on the 'Naver Pay Loan Comparison' service. This marks the first time KakaoBank's loan products have been featured on Naver Pay's loan comparison platform.The personal business real estate loan product allows users to conveniently access up to 1 billion won for various purposes, including operational funds and purchasing business premises, all through a non-face-to-face process.Initially, the Naver Pay loan comparison service will focus on loans for multi-family housing and officetels, with plans to expand the collateral options to include commercial complexes in the future.A representative from KakaoBank stated, "With this entry, more small business owners will have access to the personal business real estate loan product. We will continue to provide innovative financial services to help reduce the financial burden on our personal business customers and assist them in securing funds."Meanwhile, KakaoBank has been expanding its range of services for personal business owners, with related loan balances surpassing 3 trillion won in the first quarter of this year. 2026-06-02 15:42:00

KakaoBank Expands Personal Business Loans Through Naver Pay KakaoBank announced on June 2 that it will collaborate with Naver Pay to expand support for personal business loans.As part of this partnership, KakaoBank's 'Personal Business Real Estate Loan' product will now be available for comparison on the 'Naver Pay Loan Comparison' service. This marks the first time KakaoBank's loan products have been featured on Naver Pay's loan comparison platform.The personal business real estate loan product allows users to conveniently access up to 1 billion won for various purposes, including operational funds and purchasing business premises, all through a non-face-to-face process.Initially, the Naver Pay loan comparison service will focus on loans for multi-family housing and officetels, with plans to expand the collateral options to include commercial complexes in the future.A representative from KakaoBank stated, "With this entry, more small business owners will have access to the personal business real estate loan product. We will continue to provide innovative financial services to help reduce the financial burden on our personal business customers and assist them in securing funds."Meanwhile, KakaoBank has been expanding its range of services for personal business owners, with related loan balances surpassing 3 trillion won in the first quarter of this year. 2026-06-02 15:42:00 -

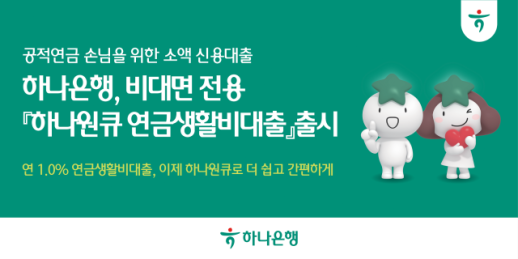

Hana Bank Launches Small-Scale Credit Loan for Pension Recipients Hana Bank announced the launch of a fully online small-scale credit loan product, 'Hana OneQ Pension Living Expense Loan,' designed for customers receiving public pensions on June 2.The Hana OneQ Pension Living Expense Loan targets customers who receive one of the four major public pensions: the National Pension, the Government Employees Pension, the Teachers Pension, and the Military Pension. This product expands access from in-person applications at bank branches to mobile, online channels.Customers can now manage everything from limit inquiries to applications, agreements, and disbursements through the Hana Bank mobile app, 'Hana OneQ,' without visiting a branch. The process has been simplified to minimize paperwork, making it easier for older customers to use with an intuitive interface.The loan offers a fixed interest rate of 1.0% and is available for a single limit of 500,000 won for customers receiving public pensions through Hana Bank. It operates as a revolving credit line, allowing for flexible use for temporary small expenses such as utility bills, medical costs, or event-related expenses.Designed to ensure stable repayment linked to pension accounts, the loan also aims to protect vulnerable groups from high-interest loan markets. Hana Bank is diversifying its offerings for public pension recipients, including the Pension Living Expense Loan, Happy Pension Loan, and home pension-linked loans.A Hana Bank official stated, "As the aging population accelerates, the demand for small living funds among pension recipients has increased, prompting the development of this product. We expect that the launch of this online product will enhance financial convenience for our customers and provide low-interest loan benefits to public pension recipients."* This article has been translated by AI. 2026-06-02 08:57:00

Hana Bank Launches Small-Scale Credit Loan for Pension Recipients Hana Bank announced the launch of a fully online small-scale credit loan product, 'Hana OneQ Pension Living Expense Loan,' designed for customers receiving public pensions on June 2.The Hana OneQ Pension Living Expense Loan targets customers who receive one of the four major public pensions: the National Pension, the Government Employees Pension, the Teachers Pension, and the Military Pension. This product expands access from in-person applications at bank branches to mobile, online channels.Customers can now manage everything from limit inquiries to applications, agreements, and disbursements through the Hana Bank mobile app, 'Hana OneQ,' without visiting a branch. The process has been simplified to minimize paperwork, making it easier for older customers to use with an intuitive interface.The loan offers a fixed interest rate of 1.0% and is available for a single limit of 500,000 won for customers receiving public pensions through Hana Bank. It operates as a revolving credit line, allowing for flexible use for temporary small expenses such as utility bills, medical costs, or event-related expenses.Designed to ensure stable repayment linked to pension accounts, the loan also aims to protect vulnerable groups from high-interest loan markets. Hana Bank is diversifying its offerings for public pension recipients, including the Pension Living Expense Loan, Happy Pension Loan, and home pension-linked loans.A Hana Bank official stated, "As the aging population accelerates, the demand for small living funds among pension recipients has increased, prompting the development of this product. We expect that the launch of this online product will enhance financial convenience for our customers and provide low-interest loan benefits to public pension recipients."* This article has been translated by AI. 2026-06-02 08:57:00 -

Major Banks Discuss Collaboration on Digital Assets Key personnel from major and regional banks gathered to discuss digital assets. On June 1, representatives from KB Kookmin Bank, Shinhan Bank, IBK Industrial Bank, and five regional banks, including iM Bank, Busan Bank, Gyeongnam Bank, Gwangju Bank, and Jeonbuk Bank, held a closed meeting at a hotel in Yeouido, Seoul. The meeting aimed to identify areas for joint action on digital assets and discuss various regulations. Participants reportedly collaborated on exploring the evolving role of banks within the rapidly changing digital ecosystem. They also discussed regulatory frameworks, including the second phase of digital asset legislation. Hana Bank did not participate in the meeting, leading to speculation in the financial sector that Hana Financial's recent investment in Dunamu prompted other banks to form alliances. Hana Bank recently announced it acquired 228,400 shares of Dunamu, representing a 6.55% stake, for approximately 1 trillion won. This acquisition positions Hana Bank as the fourth-largest shareholder in Dunamu. If Dunamu engages in a share exchange with Naver Financial, it could lead to the formation of a significant alliance. However, participating banks clarified that they are not yet discussing specific business partnerships or consortium formations. A financial industry official stated, "This was simply a meeting to analyze the market, and discussions about alliances will need to be observed further."* This article has been translated by AI. 2026-06-01 18:51:00

Major Banks Discuss Collaboration on Digital Assets Key personnel from major and regional banks gathered to discuss digital assets. On June 1, representatives from KB Kookmin Bank, Shinhan Bank, IBK Industrial Bank, and five regional banks, including iM Bank, Busan Bank, Gyeongnam Bank, Gwangju Bank, and Jeonbuk Bank, held a closed meeting at a hotel in Yeouido, Seoul. The meeting aimed to identify areas for joint action on digital assets and discuss various regulations. Participants reportedly collaborated on exploring the evolving role of banks within the rapidly changing digital ecosystem. They also discussed regulatory frameworks, including the second phase of digital asset legislation. Hana Bank did not participate in the meeting, leading to speculation in the financial sector that Hana Financial's recent investment in Dunamu prompted other banks to form alliances. Hana Bank recently announced it acquired 228,400 shares of Dunamu, representing a 6.55% stake, for approximately 1 trillion won. This acquisition positions Hana Bank as the fourth-largest shareholder in Dunamu. If Dunamu engages in a share exchange with Naver Financial, it could lead to the formation of a significant alliance. However, participating banks clarified that they are not yet discussing specific business partnerships or consortium formations. A financial industry official stated, "This was simply a meeting to analyze the market, and discussions about alliances will need to be observed further."* This article has been translated by AI. 2026-06-01 18:51:00