Journalist

KIM JIYOON

yoon0930@ajunews.com

-

Hanwha Life Financial Services Holds 2026 Annual Awards Ceremony, Honors 15 Champions Hanwha Life Financial Services announced on May 17 that it held its 2026 Annual Awards Ceremony to recognize outstanding sales performance by agents and sales managers from the previous year.The Annual Awards Ceremony is a key event celebrating agents and sales managers who achieved exceptional sales results over the past year. The ceremony was attended by approximately 1,600 people, including 15 champions, agents, sales managers, and employees.Kim Seung-yeon, chairman of Hanwha Group, conveyed his congratulations, stating, "The financial sector of Hanwha Group continues to take bold steps to lead the global financial market through AI-based industry transformation. You, at the center of this challenge, are the true heroes and pride of Hanwha Life."Since implementing a separation of manufacturing and sales in 2021, Hanwha Life Financial Services has maintained a growth trajectory. Last year, its revenue reached 2.4397 trillion won, a 7.4-fold increase compared to its first year of operation. The number of agents, including those from its subsidiary general agency (GA), is approximately 35,000, with expectations to surpass 40,000 within the year. 2026-05-17 13:46:11

Hanwha Life Financial Services Holds 2026 Annual Awards Ceremony, Honors 15 Champions Hanwha Life Financial Services announced on May 17 that it held its 2026 Annual Awards Ceremony to recognize outstanding sales performance by agents and sales managers from the previous year.The Annual Awards Ceremony is a key event celebrating agents and sales managers who achieved exceptional sales results over the past year. The ceremony was attended by approximately 1,600 people, including 15 champions, agents, sales managers, and employees.Kim Seung-yeon, chairman of Hanwha Group, conveyed his congratulations, stating, "The financial sector of Hanwha Group continues to take bold steps to lead the global financial market through AI-based industry transformation. You, at the center of this challenge, are the true heroes and pride of Hanwha Life."Since implementing a separation of manufacturing and sales in 2021, Hanwha Life Financial Services has maintained a growth trajectory. Last year, its revenue reached 2.4397 trillion won, a 7.4-fold increase compared to its first year of operation. The number of agents, including those from its subsidiary general agency (GA), is approximately 35,000, with expectations to surpass 40,000 within the year. 2026-05-17 13:46:11 -

Meritz Fire & Marine Reports Q1 Net Profit of 466.1 Billion Won, Up 0.8% Year-on-Year Meritz Fire & Marine announced on May 14 that it recorded a net profit of 466.1 billion won for the first quarter of this year, marking a 0.8% increase from 462.5 billion won in the same period last year. During the same period, the company reported revenues of 3.3079 trillion won and operating profit of 630.7 billion won, reflecting increases of 9.8% and 1.4%, respectively, compared to the previous year. Investment income rose to 296.2 billion won, a 13% increase from 262.1 billion won a year earlier, driving the overall performance. The asset management investment return rate stood at 5.4%, demonstrating effective capital management. In contrast, insurance profits fell to 334.6 billion won, down 7% from 359.8 billion won in the same quarter last year. Although the insurance contract margin (CSM) amortization increased by 5.7% to 304.1 billion won, losses in other areas, including a deficit of 38.9 billion won, impacted the results. The automobile insurance segment reported a loss of 6.4 billion won, with the loss ratio at 82.7%, a slight increase from the same period last year. The provisional solvency ratio (K-ICS) was 240%, up 1.1 percentage points from 238.9% a year ago, indicating a stable trend. A representative from Meritz Fire & Marine stated, "Despite challenging domestic and international conditions, we continue to grow through our differentiated strategy of maximizing total value."* This article has been translated by AI. 2026-05-15 02:35:42

Meritz Fire & Marine Reports Q1 Net Profit of 466.1 Billion Won, Up 0.8% Year-on-Year Meritz Fire & Marine announced on May 14 that it recorded a net profit of 466.1 billion won for the first quarter of this year, marking a 0.8% increase from 462.5 billion won in the same period last year. During the same period, the company reported revenues of 3.3079 trillion won and operating profit of 630.7 billion won, reflecting increases of 9.8% and 1.4%, respectively, compared to the previous year. Investment income rose to 296.2 billion won, a 13% increase from 262.1 billion won a year earlier, driving the overall performance. The asset management investment return rate stood at 5.4%, demonstrating effective capital management. In contrast, insurance profits fell to 334.6 billion won, down 7% from 359.8 billion won in the same quarter last year. Although the insurance contract margin (CSM) amortization increased by 5.7% to 304.1 billion won, losses in other areas, including a deficit of 38.9 billion won, impacted the results. The automobile insurance segment reported a loss of 6.4 billion won, with the loss ratio at 82.7%, a slight increase from the same period last year. The provisional solvency ratio (K-ICS) was 240%, up 1.1 percentage points from 238.9% a year ago, indicating a stable trend. A representative from Meritz Fire & Marine stated, "Despite challenging domestic and international conditions, we continue to grow through our differentiated strategy of maximizing total value."* This article has been translated by AI. 2026-05-15 02:35:42 -

KakaoBank Provides 125 Billion Won in Guaranteed Loans to Support Small Businesses in Seoul KakaoBank is taking steps to alleviate the financial burden on small businesses in Seoul.On May 14, KakaoBank announced a special contribution of 10 billion won to the Seoul Credit Guarantee Foundation, which will facilitate a total of 125 billion won in guaranteed loans.Under this agreement, KakaoBank plans to allocate 62.5 billion won each to two initiatives: the 'Rapid Financial Support' program in collaboration with the Seoul city government and the 'District Economic Support' program working with all 25 districts in Seoul.The Rapid Financial Support program includes a 'Special Contribution Guarantee' product with a maximum limit of 100 million won and the 'Quick Dream' product, which offers up to 30 million won to small business owners with personal credit scores below 839 (according to NICE standards).The District Economic Support program aims to provide loans of up to 100 million won to small businesses located in the 25 districts of Seoul. This marks the first instance of an internet-only bank collaborating with all districts in the city.Based on KakaoBank's special contribution, the Seoul Credit Guarantee Foundation will issue the guarantees, while each district will work to expand support and promote assistance for small businesses in their areas.A KakaoBank representative stated, "We initiated this agreement to ease the financial burden and enhance convenience for small business owners in Seoul. We will continue to expand financial support for individual entrepreneurs based on innovative financial technology and practice inclusive finance."* This article has been translated by AI. 2026-05-14 10:10:04

KakaoBank Provides 125 Billion Won in Guaranteed Loans to Support Small Businesses in Seoul KakaoBank is taking steps to alleviate the financial burden on small businesses in Seoul.On May 14, KakaoBank announced a special contribution of 10 billion won to the Seoul Credit Guarantee Foundation, which will facilitate a total of 125 billion won in guaranteed loans.Under this agreement, KakaoBank plans to allocate 62.5 billion won each to two initiatives: the 'Rapid Financial Support' program in collaboration with the Seoul city government and the 'District Economic Support' program working with all 25 districts in Seoul.The Rapid Financial Support program includes a 'Special Contribution Guarantee' product with a maximum limit of 100 million won and the 'Quick Dream' product, which offers up to 30 million won to small business owners with personal credit scores below 839 (according to NICE standards).The District Economic Support program aims to provide loans of up to 100 million won to small businesses located in the 25 districts of Seoul. This marks the first instance of an internet-only bank collaborating with all districts in the city.Based on KakaoBank's special contribution, the Seoul Credit Guarantee Foundation will issue the guarantees, while each district will work to expand support and promote assistance for small businesses in their areas.A KakaoBank representative stated, "We initiated this agreement to ease the financial burden and enhance convenience for small business owners in Seoul. We will continue to expand financial support for individual entrepreneurs based on innovative financial technology and practice inclusive finance."* This article has been translated by AI. 2026-05-14 10:10:04 -

Finda: Borrowers with Scores in the 400s Prefer Excellent Loans, 500-600s Favor Sunshine Loans Users with credit scores ranging from 400 to 800 are primarily seeking loans such as credit and secured loans, as well as policy finance products like Sunshine Loans. Finda reported on May 14 that an analysis of first-quarter data over the past three years revealed that borrowers in the 400 score range most frequently inquired about excellent loan products. Those with scores between 500 and 600 showed a higher frequency of inquiries about Sunshine Loans and auto-secured loans. In terms of the size of agreements, credit and auto-secured loans, along with policy finance products (Sunshine Loans, Saitdol, and New Hope Loans), accounted for a significant portion across all score ranges from 400 to 800. For borrowers in the 400 range, the most sought-after products in the first quarter of 2024 were Sunshine Loans, auto-secured loans, and home equity loans. However, in 2025, interest shifted towards home equity loans, auto-secured loans, and credit loans. In the first quarter of this year, excellent loan products accounted for 61.7% of inquiries, marking the highest interest. Finda attributed this trend to the expansion of its excellent loan brokerage service, which was first introduced in October of last year and has gained traction among low-credit borrowers. In the 500 score range, the inquiry rate for auto-secured loans has been the highest in the past three years. For those in the 600 range, credit loan inquiries were the most common in 2024 and 2025, but this year, they have been surpassed by Sunshine Loans and auto-secured loans. In the 700 score range, credit loans accounted for 33.3% of inquiries in the first quarter of this year, followed by auto-secured loans (22.6%), Saitdol loans (16.1%), Sunshine Loans (13.9%), and home equity loans (5.9%). In the 800 score range, demand for credit loans, along with Sunshine Loans, Saitdol, and auto and home equity loans, has remained steady. Lee Hye-min, CEO of Finda, stated, "Among mid- to low-credit borrowers, preferences for loan products vary by score range, making precise product matching essential."* This article has been translated by AI. 2026-05-14 09:03:03

Finda: Borrowers with Scores in the 400s Prefer Excellent Loans, 500-600s Favor Sunshine Loans Users with credit scores ranging from 400 to 800 are primarily seeking loans such as credit and secured loans, as well as policy finance products like Sunshine Loans. Finda reported on May 14 that an analysis of first-quarter data over the past three years revealed that borrowers in the 400 score range most frequently inquired about excellent loan products. Those with scores between 500 and 600 showed a higher frequency of inquiries about Sunshine Loans and auto-secured loans. In terms of the size of agreements, credit and auto-secured loans, along with policy finance products (Sunshine Loans, Saitdol, and New Hope Loans), accounted for a significant portion across all score ranges from 400 to 800. For borrowers in the 400 range, the most sought-after products in the first quarter of 2024 were Sunshine Loans, auto-secured loans, and home equity loans. However, in 2025, interest shifted towards home equity loans, auto-secured loans, and credit loans. In the first quarter of this year, excellent loan products accounted for 61.7% of inquiries, marking the highest interest. Finda attributed this trend to the expansion of its excellent loan brokerage service, which was first introduced in October of last year and has gained traction among low-credit borrowers. In the 500 score range, the inquiry rate for auto-secured loans has been the highest in the past three years. For those in the 600 range, credit loan inquiries were the most common in 2024 and 2025, but this year, they have been surpassed by Sunshine Loans and auto-secured loans. In the 700 score range, credit loans accounted for 33.3% of inquiries in the first quarter of this year, followed by auto-secured loans (22.6%), Saitdol loans (16.1%), Sunshine Loans (13.9%), and home equity loans (5.9%). In the 800 score range, demand for credit loans, along with Sunshine Loans, Saitdol, and auto and home equity loans, has remained steady. Lee Hye-min, CEO of Finda, stated, "Among mid- to low-credit borrowers, preferences for loan products vary by score range, making precise product matching essential."* This article has been translated by AI. 2026-05-14 09:03:03 -

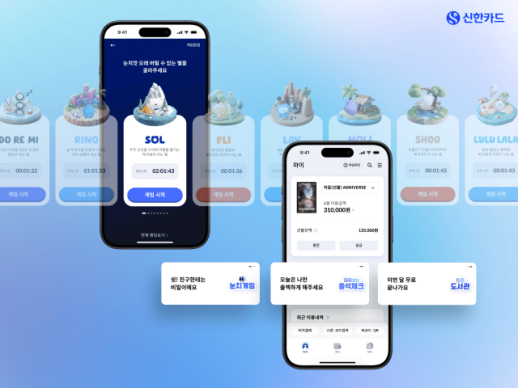

Shinhan Card Integrates Payments and Asset Management with SOL Pay Shinhan Card's lifestyle finance platform, Shinhan SOL Pay, is expanding its offerings by integrating payment, asset management, travel, and convenience services into a comprehensive financial platform. As of the end of February, Shinhan Card reported that the number of subscribers to Shinhan SOL Pay has reached approximately 20 million. The company aims to encourage customers to use Shinhan SOL Pay across various payment scenarios, thereby accumulating data to enhance customer experiences and build a virtuous ecosystem. Shinhan SOL Pay includes features such as a payment function called 'Pay,' transaction management under 'My,' asset management based on My Data in 'Assets,' a collection of discounts and events in 'Benefits,' and loan product recommendations in 'Finance,' all within a single app. The payment infrastructure is also being expanded. Shinhan Card has introduced the industry's first iPhone touch payment service, allowing iPhone users to make payments at all merchants without a physical card. It also offers global payment features such as Android-based NFC payments and UnionPay and Line Pay QR payments. Additionally, a dedicated platform for teenagers, 'SOL Pay First,' has been launched as an industry first. This platform is tailored to the financial lives of teenagers, prominently displaying their spending and remaining balance for the month, along with payment and transfer functions on the main screen. Services specifically designed for overseas travel have also been enhanced. Through 'SOL Travel+,' users can access discounts and cashback benefits for accommodations, shopping, and dining, as well as features to block overseas won payments and prevent fraudulent transactions abroad.* This article has been translated by AI. 2026-05-13 17:18:00

Shinhan Card Integrates Payments and Asset Management with SOL Pay Shinhan Card's lifestyle finance platform, Shinhan SOL Pay, is expanding its offerings by integrating payment, asset management, travel, and convenience services into a comprehensive financial platform. As of the end of February, Shinhan Card reported that the number of subscribers to Shinhan SOL Pay has reached approximately 20 million. The company aims to encourage customers to use Shinhan SOL Pay across various payment scenarios, thereby accumulating data to enhance customer experiences and build a virtuous ecosystem. Shinhan SOL Pay includes features such as a payment function called 'Pay,' transaction management under 'My,' asset management based on My Data in 'Assets,' a collection of discounts and events in 'Benefits,' and loan product recommendations in 'Finance,' all within a single app. The payment infrastructure is also being expanded. Shinhan Card has introduced the industry's first iPhone touch payment service, allowing iPhone users to make payments at all merchants without a physical card. It also offers global payment features such as Android-based NFC payments and UnionPay and Line Pay QR payments. Additionally, a dedicated platform for teenagers, 'SOL Pay First,' has been launched as an industry first. This platform is tailored to the financial lives of teenagers, prominently displaying their spending and remaining balance for the month, along with payment and transfer functions on the main screen. Services specifically designed for overseas travel have also been enhanced. Through 'SOL Travel+,' users can access discounts and cashback benefits for accommodations, shopping, and dining, as well as features to block overseas won payments and prevent fraudulent transactions abroad.* This article has been translated by AI. 2026-05-13 17:18:00 -

KakaoPay Expands Payment Platform with 1.13 Million Merchants KakaoPay is strengthening its competitiveness as a comprehensive payment platform by expanding into overseas payments, membership services, and utility bill payments.As of May 13, KakaoPay reported that it launched South Korea's first simple payment service for online transactions in 2014 and introduced offline payment services in 2018. Currently, KakaoPay is available at 1.13 million merchants nationwide. It also supports payments at 3 million locations through Samsung Pay and 1.1 million small business stores via Zero Pay.Users can utilize QR and barcode payments at various offline merchants, including convenience stores, cafes, restaurants, movie theaters, and supermarkets. The service also supports Samsung Pay's Magnetic Secure Transmission (MST) and Zero Pay's QR scanning method. Membership points such as Happy Points, CJ ONE, and Shinsegae Points are automatically accumulated during transactions.KakaoPay is also expanding its overseas payment services. It supports QR payments in over 50 countries and regions, including China, Japan, Southeast Asia, Europe, and the Americas, based on the AlipayPlus network. The introduction of NFC-based 'Tap & Go' payments allows mobile transactions at approximately 150 million Mastercard merchants worldwide.The company has enhanced its lifestyle services as well. KakaoPay's membership program allows users to accumulate and use points from over 40 partner programs with a single barcode. Through its electronic billing payment service, users can view and pay utility bills such as electricity, gas, local taxes, communication fees, and apartment management fees via KakaoTalk and KakaoPay.* This article has been translated by AI. 2026-05-13 17:17:22

KakaoPay Expands Payment Platform with 1.13 Million Merchants KakaoPay is strengthening its competitiveness as a comprehensive payment platform by expanding into overseas payments, membership services, and utility bill payments.As of May 13, KakaoPay reported that it launched South Korea's first simple payment service for online transactions in 2014 and introduced offline payment services in 2018. Currently, KakaoPay is available at 1.13 million merchants nationwide. It also supports payments at 3 million locations through Samsung Pay and 1.1 million small business stores via Zero Pay.Users can utilize QR and barcode payments at various offline merchants, including convenience stores, cafes, restaurants, movie theaters, and supermarkets. The service also supports Samsung Pay's Magnetic Secure Transmission (MST) and Zero Pay's QR scanning method. Membership points such as Happy Points, CJ ONE, and Shinsegae Points are automatically accumulated during transactions.KakaoPay is also expanding its overseas payment services. It supports QR payments in over 50 countries and regions, including China, Japan, Southeast Asia, Europe, and the Americas, based on the AlipayPlus network. The introduction of NFC-based 'Tap & Go' payments allows mobile transactions at approximately 150 million Mastercard merchants worldwide.The company has enhanced its lifestyle services as well. KakaoPay's membership program allows users to accumulate and use points from over 40 partner programs with a single barcode. Through its electronic billing payment service, users can view and pay utility bills such as electricity, gas, local taxes, communication fees, and apartment management fees via KakaoTalk and KakaoPay.* This article has been translated by AI. 2026-05-13 17:17:22 -

The Evolving Landscape of Payment Methods: Competition Intensifies in Offline Transactions The competition in the mobile payment market is shifting from securing app users to establishing dominance in offline payment infrastructure. As the mobile app market reaches saturation, the battle for control over payment terminals and networks is intensifying.According to a report released in January by global market research firm Mordor Intelligence, near-field communication (NFC) payment methods accounted for 54.2% of South Korea's mobile payment market last year.As a result, the penetration rate of NFC terminals in South Korea is expected to have increased significantly this year. The country's card payment infrastructure has primarily been built around magnetic secure transmission (MST) and integrated circuit (IC) terminals. Even after the introduction of Apple Pay, NFC-based payments remained at around 10% as of the end of last year.Recently, major tech companies Naver Pay and Toss have ramped up their competition to distribute their own NFC terminals. Toss is leading the charge, expanding its reach through its subsidiary Toss Place, which has been distributing the smart terminal Toss Front since 2023. As of April, the number of Toss Front installations surpassed 330,000. Initially focused on popular areas in Seoul, such as Seongsu and Hongdae, the infrastructure is now expanding to traditional markets and regions outside the metropolitan area.Naver Pay, a latecomer in the offline market, is accelerating its efforts. Its smart terminal, Npay Connect, launched in November, supports card payments, mobile payments, QR codes, and facial recognition payment service Face Sign. The company is employing a two-track strategy targeting both small businesses and franchises. A Naver Pay representative stated, "While we cannot disclose specific distribution figures, we believe we have exceeded our internal targets within five months of launch," adding that they are also working to introduce terminals at Paris Baguette in the second half of the year, which will increase availability in offline stores.Kakao Pay is focusing on expanding its QR-based payment network rather than distributing its own terminals. The company has opted to collaborate with existing point-of-sale (POS) and value-added network (VAN) providers instead of building its own hardware. A Kakao Pay representative emphasized, "The key is not to own the terminals but to enable Kakao Pay transactions anywhere," noting that they are expanding offline touchpoints through QR orders, kiosk payments, and international QR payments.Industry experts believe that control over offline payment data will be a crucial factor in determining the future success of the mobile payment market. As mobile payments expand beyond online transactions into the offline consumer landscape, companies that secure payment infrastructure can achieve both user lock-in effects and data competitiveness.Jeong Yu-shin, a professor at Sogang University's Business School, stated, "Fintech platforms have traditionally grown around non-face-to-face services, but they are now transitioning to strengthen offline touchpoints to enhance customer loyalty. Online services allow users to switch easily to better platforms, so there is a trend to combine offline infrastructure to solidify customer bases."The competition in offline payments is expected to intensify further if Apple Pay expands its partnerships with card issuers. Seo Ji-yong, a professor at Sangmyung University’s Business School, remarked, "Once Apple Pay is introduced, fintech companies will seek partnerships to expand in the offline market, leading to intensified competition for market share in face-to-face payment channels."* This article has been translated by AI. 2026-05-13 17:09:46

The Evolving Landscape of Payment Methods: Competition Intensifies in Offline Transactions The competition in the mobile payment market is shifting from securing app users to establishing dominance in offline payment infrastructure. As the mobile app market reaches saturation, the battle for control over payment terminals and networks is intensifying.According to a report released in January by global market research firm Mordor Intelligence, near-field communication (NFC) payment methods accounted for 54.2% of South Korea's mobile payment market last year.As a result, the penetration rate of NFC terminals in South Korea is expected to have increased significantly this year. The country's card payment infrastructure has primarily been built around magnetic secure transmission (MST) and integrated circuit (IC) terminals. Even after the introduction of Apple Pay, NFC-based payments remained at around 10% as of the end of last year.Recently, major tech companies Naver Pay and Toss have ramped up their competition to distribute their own NFC terminals. Toss is leading the charge, expanding its reach through its subsidiary Toss Place, which has been distributing the smart terminal Toss Front since 2023. As of April, the number of Toss Front installations surpassed 330,000. Initially focused on popular areas in Seoul, such as Seongsu and Hongdae, the infrastructure is now expanding to traditional markets and regions outside the metropolitan area.Naver Pay, a latecomer in the offline market, is accelerating its efforts. Its smart terminal, Npay Connect, launched in November, supports card payments, mobile payments, QR codes, and facial recognition payment service Face Sign. The company is employing a two-track strategy targeting both small businesses and franchises. A Naver Pay representative stated, "While we cannot disclose specific distribution figures, we believe we have exceeded our internal targets within five months of launch," adding that they are also working to introduce terminals at Paris Baguette in the second half of the year, which will increase availability in offline stores.Kakao Pay is focusing on expanding its QR-based payment network rather than distributing its own terminals. The company has opted to collaborate with existing point-of-sale (POS) and value-added network (VAN) providers instead of building its own hardware. A Kakao Pay representative emphasized, "The key is not to own the terminals but to enable Kakao Pay transactions anywhere," noting that they are expanding offline touchpoints through QR orders, kiosk payments, and international QR payments.Industry experts believe that control over offline payment data will be a crucial factor in determining the future success of the mobile payment market. As mobile payments expand beyond online transactions into the offline consumer landscape, companies that secure payment infrastructure can achieve both user lock-in effects and data competitiveness.Jeong Yu-shin, a professor at Sogang University's Business School, stated, "Fintech platforms have traditionally grown around non-face-to-face services, but they are now transitioning to strengthen offline touchpoints to enhance customer loyalty. Online services allow users to switch easily to better platforms, so there is a trend to combine offline infrastructure to solidify customer bases."The competition in offline payments is expected to intensify further if Apple Pay expands its partnerships with card issuers. Seo Ji-yong, a professor at Sangmyung University’s Business School, remarked, "Once Apple Pay is introduced, fintech companies will seek partnerships to expand in the offline market, leading to intensified competition for market share in face-to-face payment channels."* This article has been translated by AI. 2026-05-13 17:09:46 -

To Avoid Increasing Debt, Inclusive Finance Must Evolve While walking through my hometown recently, I counted the "For Rent" signs on buildings that had housed businesses for decades. The closure of these shops starkly illustrates the challenges faced by self-employed individuals.The difficulties in the field are reflected in the numbers. As of the end of last year, six out of ten self-employed individuals who borrowed from financial institutions were found to be multiple debtors, having taken loans from three or more sources. This indicates a reliance on borrowing from various financial sectors to maintain their livelihoods and repay existing debts.In response, the government has proposed "inclusive finance" as a solution. This initiative aims to expand financial support for vulnerable groups and self-employed individuals, enhancing their access to financial services. The government is also significantly lowering interest rates on policy products such as the New Hope Seed Loan, Sunshine Loan, and Youth Future Connection Loan through the Financial Stability Fund. Discussions are ongoing to improve the credit evaluation system to lower barriers for low- and medium-credit borrowers.While the expansion of inclusive finance is undoubtedly a necessary policy direction, there is a risk that discussions may focus solely on "increased lending." Currently, the self-employed sector faces not just a lack of liquidity but also structural challenges stemming from decreased consumer spending and rising costs.In fact, a survey conducted in February by the National Assembly Future Research Institute among 3,088 self-employed individuals revealed that 68.7% reported difficulties due to "raw material and supply costs," while 66.2% cited "intensified competition within the same industry." Additionally, 65.9% indicated that acquiring new customers is challenging. In such a context, if short-term loan supply is repeatedly provided, there is a risk that financial support will serve as a means to maintain existing debt rather than a stepping stone to recovery.Therefore, inclusive finance must evolve beyond mere loan support to genuinely assist financially vulnerable groups in achieving self-sufficiency. The Financial Services Commission declared a "transformation to inclusive finance" in January, setting the establishment of vulnerable groups within the formal financial system and their self-reliance as core values. For this declaration to lead to tangible results, a structure must be created that facilitates the recovery and resurgence of self-employed individuals and other financially vulnerable groups.First, policies are needed to help them survive in the changed domestic market and social structure. The focus should not only be on increasing the total amount of loans but also on the actual recovery and resurgence of vulnerable groups. For those diligently repaying their debts, options to reduce interest burdens and swiftly adjust unmanageable debts could be considered. For those unable to continue their businesses, support for transitioning to wage employment or orderly closures may be more effective than pressuring them to extend operations.Non-financial support is also essential to enhance the survival capacity of self-employed individuals. Training for digital transformation and support for market access should be provided to help them adapt to an environment where delivery platforms and online distribution are predominant. Additionally, vocational training and support for living stability should be examined for those undergoing industry transitions or re-employment. The success of inclusive finance should be evaluated not by how much capital is supplied to the market, but by how many individuals can continue their economic activities. Only then can inclusive finance establish itself as a genuine financial policy. * This article has been translated by AI. 2026-05-12 06:07:06

To Avoid Increasing Debt, Inclusive Finance Must Evolve While walking through my hometown recently, I counted the "For Rent" signs on buildings that had housed businesses for decades. The closure of these shops starkly illustrates the challenges faced by self-employed individuals.The difficulties in the field are reflected in the numbers. As of the end of last year, six out of ten self-employed individuals who borrowed from financial institutions were found to be multiple debtors, having taken loans from three or more sources. This indicates a reliance on borrowing from various financial sectors to maintain their livelihoods and repay existing debts.In response, the government has proposed "inclusive finance" as a solution. This initiative aims to expand financial support for vulnerable groups and self-employed individuals, enhancing their access to financial services. The government is also significantly lowering interest rates on policy products such as the New Hope Seed Loan, Sunshine Loan, and Youth Future Connection Loan through the Financial Stability Fund. Discussions are ongoing to improve the credit evaluation system to lower barriers for low- and medium-credit borrowers.While the expansion of inclusive finance is undoubtedly a necessary policy direction, there is a risk that discussions may focus solely on "increased lending." Currently, the self-employed sector faces not just a lack of liquidity but also structural challenges stemming from decreased consumer spending and rising costs.In fact, a survey conducted in February by the National Assembly Future Research Institute among 3,088 self-employed individuals revealed that 68.7% reported difficulties due to "raw material and supply costs," while 66.2% cited "intensified competition within the same industry." Additionally, 65.9% indicated that acquiring new customers is challenging. In such a context, if short-term loan supply is repeatedly provided, there is a risk that financial support will serve as a means to maintain existing debt rather than a stepping stone to recovery.Therefore, inclusive finance must evolve beyond mere loan support to genuinely assist financially vulnerable groups in achieving self-sufficiency. The Financial Services Commission declared a "transformation to inclusive finance" in January, setting the establishment of vulnerable groups within the formal financial system and their self-reliance as core values. For this declaration to lead to tangible results, a structure must be created that facilitates the recovery and resurgence of self-employed individuals and other financially vulnerable groups.First, policies are needed to help them survive in the changed domestic market and social structure. The focus should not only be on increasing the total amount of loans but also on the actual recovery and resurgence of vulnerable groups. For those diligently repaying their debts, options to reduce interest burdens and swiftly adjust unmanageable debts could be considered. For those unable to continue their businesses, support for transitioning to wage employment or orderly closures may be more effective than pressuring them to extend operations.Non-financial support is also essential to enhance the survival capacity of self-employed individuals. Training for digital transformation and support for market access should be provided to help them adapt to an environment where delivery platforms and online distribution are predominant. Additionally, vocational training and support for living stability should be examined for those undergoing industry transitions or re-employment. The success of inclusive finance should be evaluated not by how much capital is supplied to the market, but by how many individuals can continue their economic activities. Only then can inclusive finance establish itself as a genuine financial policy. * This article has been translated by AI. 2026-05-12 06:07:06 -

Green Elephant Revitalizes Hongseong's Downtown with Support from Saemaul Geumgo Saemaul Geumgo is expanding its role as a "local coexistence platform" that connects youth entrepreneurship with community revitalization, going beyond simple financial support. Leveraging its strengths as a community-based financial institution, it is creating a virtuous cycle in the local economy through funding and community connections.A prime example is the youth startup Green Elephant in Hongseong, South Chungcheong Province. Green Elephant produces meal kits using eco-friendly agricultural products contracted from over 30 local farms and delivers them in the early morning to the Hongseong area. Founded by Kim Man-i, the startup connects local agricultural products with consumers and young people.In its early stages, Green Elephant received 50 million won in funding from Hongju Saemaul Geumgo to establish its business. It later secured an additional 40 million won through the Saemaul Geumgo Central Association's Youth Local Support Project. The support extended beyond funding; Hongju Saemaul Geumgo also promoted and sold Green Elephant's products at its general meetings and member events.This collaboration has led to the revitalization of Hongseong's downtown area. The "Mujeong Market," a local commercial revitalization project, has been held nine times on Honggotong Street, attracting about 1,700 visitors. This initiative has transformed what was once a declining cultural and commercial center in Hongseong into a vibrant gathering place.The case of Green Elephant illustrates how local production, consumers, and finance can be interconnected in a virtuous cycle. Analysts suggest that local financial institutions are playing a platform role that goes beyond simple lending to connect entrepreneurship, distribution, and youth communities.The Hongseong MG Cooperation Center, established based on the private startup incubation facility Jelly's Lounge, is a notable example. This space has hosted 96 meetings for local creators, fostering collaboration among young residents.The MG Cooperation Center project is an initiative by the Saemaul Geumgo Central Association, in collaboration with the Ministry of the Interior and Safety and the Together Foundation, aimed at addressing local issues such as urban decline, agricultural overproduction, and youth isolation through youth entrepreneurship and community-based projects since 2024.The Saemaul Geumgo Central Association plans to expand its collaboration with youth village enterprises this year, selecting over 20 organizations to implement cooperative projects worth approximately 2 billion won. A representative from the Saemaul Geumgo Central Association stated, "We plan to actively promote community development through continuous cooperation with social solidarity economy enterprises."* This article has been translated by AI. 2026-05-11 06:12:20

Green Elephant Revitalizes Hongseong's Downtown with Support from Saemaul Geumgo Saemaul Geumgo is expanding its role as a "local coexistence platform" that connects youth entrepreneurship with community revitalization, going beyond simple financial support. Leveraging its strengths as a community-based financial institution, it is creating a virtuous cycle in the local economy through funding and community connections.A prime example is the youth startup Green Elephant in Hongseong, South Chungcheong Province. Green Elephant produces meal kits using eco-friendly agricultural products contracted from over 30 local farms and delivers them in the early morning to the Hongseong area. Founded by Kim Man-i, the startup connects local agricultural products with consumers and young people.In its early stages, Green Elephant received 50 million won in funding from Hongju Saemaul Geumgo to establish its business. It later secured an additional 40 million won through the Saemaul Geumgo Central Association's Youth Local Support Project. The support extended beyond funding; Hongju Saemaul Geumgo also promoted and sold Green Elephant's products at its general meetings and member events.This collaboration has led to the revitalization of Hongseong's downtown area. The "Mujeong Market," a local commercial revitalization project, has been held nine times on Honggotong Street, attracting about 1,700 visitors. This initiative has transformed what was once a declining cultural and commercial center in Hongseong into a vibrant gathering place.The case of Green Elephant illustrates how local production, consumers, and finance can be interconnected in a virtuous cycle. Analysts suggest that local financial institutions are playing a platform role that goes beyond simple lending to connect entrepreneurship, distribution, and youth communities.The Hongseong MG Cooperation Center, established based on the private startup incubation facility Jelly's Lounge, is a notable example. This space has hosted 96 meetings for local creators, fostering collaboration among young residents.The MG Cooperation Center project is an initiative by the Saemaul Geumgo Central Association, in collaboration with the Ministry of the Interior and Safety and the Together Foundation, aimed at addressing local issues such as urban decline, agricultural overproduction, and youth isolation through youth entrepreneurship and community-based projects since 2024.The Saemaul Geumgo Central Association plans to expand its collaboration with youth village enterprises this year, selecting over 20 organizations to implement cooperative projects worth approximately 2 billion won. A representative from the Saemaul Geumgo Central Association stated, "We plan to actively promote community development through continuous cooperation with social solidarity economy enterprises."* This article has been translated by AI. 2026-05-11 06:12:20 -

Fans Line Up for 'B Mainstream Invitation' to See 'Heo Gwan-min' "It seems more important to not judge others based on their tastes than to refine your own preferences. Just because you've seen high-end or classic films doesn't mean you should show off," said Kim Min-kyung, an editor at Minumsa, during an interview before the 'B Mainstream Invitation' event on May 9. Joining her were rapper Heo Ki Shibaseki and drummer Kim Gan-ji, who added, "Watch a lot and enjoy a lot," and "When you like something, don’t worry about what others think."The trio, known as 'Heo-Gan-Min,' are featured in Toss's YouTube channel 'Moneygraphy,' where they engage in candid discussions about their diverse tastes in film, literature, and gaming. Their open dialogue resonates with younger audiences, creating a liberating atmosphere that encourages honesty over judgment. Interestingly, the entity behind this taste community is the financial platform Toss. Since launching its YouTube channel 'Moneygraphy' in September 2021, Toss has expanded its content to include economic and lifestyle topics. The 'B Mainstream Invitation' is a spinoff from the economic content series 'B Mainstream Economics.'Toss's focus on content that is less directly related to financial services aligns with its strategy to enhance brand experience. This approach aims to increase user engagement and foster a sense of intimacy with the platform.The offline talk show attracted over 1,500 participants, showcasing its popularity. Attendees expressed their enthusiasm in an open chat room, stating things like, "I will move my salary account to Toss," and "I signed up for Toss FacePay." Toss representatives noted that the scene of participants lining up from 2:30 PM for the 6 PM event was unusual for a financial company.Baek Soon-do, the producer behind the 'B Mainstream Invitation,' remarked, "For the brand, offline events are the most effective way to leave a strong impression of Toss. We have not yet started concrete discussions about Season 2 or future directions, but we plan to continue presenting engaging projects and content."* This article has been translated by AI. 2026-05-11 06:05:11

Fans Line Up for 'B Mainstream Invitation' to See 'Heo Gwan-min' "It seems more important to not judge others based on their tastes than to refine your own preferences. Just because you've seen high-end or classic films doesn't mean you should show off," said Kim Min-kyung, an editor at Minumsa, during an interview before the 'B Mainstream Invitation' event on May 9. Joining her were rapper Heo Ki Shibaseki and drummer Kim Gan-ji, who added, "Watch a lot and enjoy a lot," and "When you like something, don’t worry about what others think."The trio, known as 'Heo-Gan-Min,' are featured in Toss's YouTube channel 'Moneygraphy,' where they engage in candid discussions about their diverse tastes in film, literature, and gaming. Their open dialogue resonates with younger audiences, creating a liberating atmosphere that encourages honesty over judgment. Interestingly, the entity behind this taste community is the financial platform Toss. Since launching its YouTube channel 'Moneygraphy' in September 2021, Toss has expanded its content to include economic and lifestyle topics. The 'B Mainstream Invitation' is a spinoff from the economic content series 'B Mainstream Economics.'Toss's focus on content that is less directly related to financial services aligns with its strategy to enhance brand experience. This approach aims to increase user engagement and foster a sense of intimacy with the platform.The offline talk show attracted over 1,500 participants, showcasing its popularity. Attendees expressed their enthusiasm in an open chat room, stating things like, "I will move my salary account to Toss," and "I signed up for Toss FacePay." Toss representatives noted that the scene of participants lining up from 2:30 PM for the 6 PM event was unusual for a financial company.Baek Soon-do, the producer behind the 'B Mainstream Invitation,' remarked, "For the brand, offline events are the most effective way to leave a strong impression of Toss. We have not yet started concrete discussions about Season 2 or future directions, but we plan to continue presenting engaging projects and content."* This article has been translated by AI. 2026-05-11 06:05:11