Journalist

KIM JIYOON

yoon0930@ajunews.com

-

Kona I Posts 94% Jump in Q1 Operating Profit on Premium Metal Card Exports Fintech company Kona I said Tuesday it posted first-quarter consolidated revenue of 76.6 billion won ($766 billion) and operating profit of 24.6 billion won. Revenue rose 31.3% from a year earlier and operating profit jumped 94%, the company said. The card industry typically sees weaker volumes early in the year because overseas financial institutions place orders in cycles, but Kona I reported double-digit growth in both revenue and profit. Kona I said expanded exports of premium metal cards drove the results, citing steady growth in demand for high-end cards globally even as mobile payments spread. Its payments platform business also grew, the company said, as the central government expanded budget support for local currency programs. Kona I said it maintained its operating base in major local governments including Gyeonggi Province and expanded the platform to new areas including Jincheon, Sejong, Chungju and Sangju, boosting transaction volume. The company said its shift to an open platform also helped, as it broadened links with mobile payment services such as Naver Pay and Kakao Pay and diversified rewards. Chief Executive Cho Jeong-il said both overseas exports and the domestic platform business posted meaningful year-on-year growth. He said the company expects growth momentum to continue for the full year, noting that global card volumes tend to be concentrated in the second half. * This article has been translated by AI. 2026-04-15 13:57:37

Kona I Posts 94% Jump in Q1 Operating Profit on Premium Metal Card Exports Fintech company Kona I said Tuesday it posted first-quarter consolidated revenue of 76.6 billion won ($766 billion) and operating profit of 24.6 billion won. Revenue rose 31.3% from a year earlier and operating profit jumped 94%, the company said. The card industry typically sees weaker volumes early in the year because overseas financial institutions place orders in cycles, but Kona I reported double-digit growth in both revenue and profit. Kona I said expanded exports of premium metal cards drove the results, citing steady growth in demand for high-end cards globally even as mobile payments spread. Its payments platform business also grew, the company said, as the central government expanded budget support for local currency programs. Kona I said it maintained its operating base in major local governments including Gyeonggi Province and expanded the platform to new areas including Jincheon, Sejong, Chungju and Sangju, boosting transaction volume. The company said its shift to an open platform also helped, as it broadened links with mobile payment services such as Naver Pay and Kakao Pay and diversified rewards. Chief Executive Cho Jeong-il said both overseas exports and the domestic platform business posted meaningful year-on-year growth. He said the company expects growth momentum to continue for the full year, noting that global card volumes tend to be concentrated in the second half. * This article has been translated by AI. 2026-04-15 13:57:37 -

Korean Internet Banks Lift Deposit Rates Into 3% Range to Compete for Savers As major commercial banks keep deposit rates in the 2% range, South Korea’s internet-only banks are competing for funding by offering rates even 0.1 percentage point higher. The strategy is aimed at attracting rate-sensitive savers seeking higher returns on deposits. According to the financial sector on Monday, key deposit and savings products at internet banks are generally priced in the 3% range. KakaoBank raised rates on some funding products by up to 0.1 percentage point starting Monday. Its one-year time deposit rose to 3.1% from 3.0%, and its one-year flexible savings product increased to 3.25% from 3.15%. The move marked an additional hike about two months after Feb. 13 and puts its rates among the highest compared with major commercial banks. K Bank also increased the one-year rate on its “CodeK” time deposit to 3.2% from 3.01% starting March 31, a 0.19 percentage point rise. Toss Bank has not raised rates on funding products this year, but launched a one-year “time deposit with interest paid upfront” product in December at about 2.8% annually. Internet banks have been stepping up rate competition as they seek to expand their deposit base by offering higher yields than traditional lenders. Unlike major banks, internet banks do not operate offline branches, reducing fixed costs such as branch expenses and in-person staffing and giving them more room to offer higher deposit rates. “Given the nature of internet banks, we are maintaining a strategy of setting deposit rates somewhat higher than those of major banks,” an official at one internet bank said. “Even offering rates in the 3% range does not put undue pressure on profitability.” Rising market rates have also played a role. According to the Korea Financial Investment Association, yields on one-year bank bonds have recently been in the low 3% range, up about 0.3 percentage point so far this year. While higher bank-bond yields raise funding costs, major banks have a larger share of low-cost deposits — such as payroll accounts and corporate operating funds — reducing the incentive to raise deposit and savings rates. Internet banks, by contrast, have a higher share of customers sensitive to interest rates and are moving to strengthen competitiveness through deposit and savings products. “Market rates have risen significantly recently, so we adjusted rates as a response,” another internet-bank official said.* This article has been translated by AI. 2026-04-14 16:42:00

Korean Internet Banks Lift Deposit Rates Into 3% Range to Compete for Savers As major commercial banks keep deposit rates in the 2% range, South Korea’s internet-only banks are competing for funding by offering rates even 0.1 percentage point higher. The strategy is aimed at attracting rate-sensitive savers seeking higher returns on deposits. According to the financial sector on Monday, key deposit and savings products at internet banks are generally priced in the 3% range. KakaoBank raised rates on some funding products by up to 0.1 percentage point starting Monday. Its one-year time deposit rose to 3.1% from 3.0%, and its one-year flexible savings product increased to 3.25% from 3.15%. The move marked an additional hike about two months after Feb. 13 and puts its rates among the highest compared with major commercial banks. K Bank also increased the one-year rate on its “CodeK” time deposit to 3.2% from 3.01% starting March 31, a 0.19 percentage point rise. Toss Bank has not raised rates on funding products this year, but launched a one-year “time deposit with interest paid upfront” product in December at about 2.8% annually. Internet banks have been stepping up rate competition as they seek to expand their deposit base by offering higher yields than traditional lenders. Unlike major banks, internet banks do not operate offline branches, reducing fixed costs such as branch expenses and in-person staffing and giving them more room to offer higher deposit rates. “Given the nature of internet banks, we are maintaining a strategy of setting deposit rates somewhat higher than those of major banks,” an official at one internet bank said. “Even offering rates in the 3% range does not put undue pressure on profitability.” Rising market rates have also played a role. According to the Korea Financial Investment Association, yields on one-year bank bonds have recently been in the low 3% range, up about 0.3 percentage point so far this year. While higher bank-bond yields raise funding costs, major banks have a larger share of low-cost deposits — such as payroll accounts and corporate operating funds — reducing the incentive to raise deposit and savings rates. Internet banks, by contrast, have a higher share of customers sensitive to interest rates and are moving to strengthen competitiveness through deposit and savings products. “Market rates have risen significantly recently, so we adjusted rates as a response,” another internet-bank official said.* This article has been translated by AI. 2026-04-14 16:42:00 -

KakaoBank Eyes Mongolia Expansion, Prepares Stablecoin Plan KakaoBank said it is pushing to enter Mongolia after expanding into Indonesia and Thailand, as it looks to diversify revenue through overseas business. The company also said it plans to secure a license to issue stablecoins after the enactment of the Digital Asset Basic Act, aiming to take an early lead in that market. At a news conference on April 8 at the Fairmont Ambassador Seoul in Yeouido, KakaoBank CEO Yoon Ho-young said the company plans to export its credit-scoring system, called “KakaoBank Score,” to Mongolian financial institutions. The model uses nonfinancial data, he said. “Mongolia is a market where the credit evaluation system has not yet been sufficiently advanced,” Yoon said. “It is meaningful to apply KakaoBank’s inclusive finance capabilities accumulated in Korea to overseas markets.” Mongolia would be KakaoBank’s third overseas business after Indonesia and Thailand. KakaoBank is also preparing to start operations in the first quarter of next year for “BankX,” an internet bank set up as a joint venture with Thailand’s SCBX Group. KakaoBank said it plans to introduce key products locally, including its “26-week savings” and “group account,” and to lead development of the mobile app to deliver a user experience similar to its service in Korea. KakaoBank said its competitiveness in “easy finance” is driving broader cooperation with overseas financial firms, saying its services can be effective in Southeast Asian markets where informal lending is high or financial infrastructure is limited. Yoon said local interest was strong in its overdraft loan product, adding that working with local partners, rather than entering directly, can reduce risk. KakaoBank also said it plans to obtain a stablecoin issuance license after the Digital Asset Basic Act is enacted and to participate across issuance and distribution. If needed, it will consider mergers and acquisitions across payments and investment, the company said. “The goal is to make a won-denominated stablecoin as convenient to use as withdrawing funds from an account,” Yoon said. “If there is a suitable company, we will actively look for M&A opportunities.” 2026-04-08 15:57:17

KakaoBank Eyes Mongolia Expansion, Prepares Stablecoin Plan KakaoBank said it is pushing to enter Mongolia after expanding into Indonesia and Thailand, as it looks to diversify revenue through overseas business. The company also said it plans to secure a license to issue stablecoins after the enactment of the Digital Asset Basic Act, aiming to take an early lead in that market. At a news conference on April 8 at the Fairmont Ambassador Seoul in Yeouido, KakaoBank CEO Yoon Ho-young said the company plans to export its credit-scoring system, called “KakaoBank Score,” to Mongolian financial institutions. The model uses nonfinancial data, he said. “Mongolia is a market where the credit evaluation system has not yet been sufficiently advanced,” Yoon said. “It is meaningful to apply KakaoBank’s inclusive finance capabilities accumulated in Korea to overseas markets.” Mongolia would be KakaoBank’s third overseas business after Indonesia and Thailand. KakaoBank is also preparing to start operations in the first quarter of next year for “BankX,” an internet bank set up as a joint venture with Thailand’s SCBX Group. KakaoBank said it plans to introduce key products locally, including its “26-week savings” and “group account,” and to lead development of the mobile app to deliver a user experience similar to its service in Korea. KakaoBank said its competitiveness in “easy finance” is driving broader cooperation with overseas financial firms, saying its services can be effective in Southeast Asian markets where informal lending is high or financial infrastructure is limited. Yoon said local interest was strong in its overdraft loan product, adding that working with local partners, rather than entering directly, can reduce risk. KakaoBank also said it plans to obtain a stablecoin issuance license after the Digital Asset Basic Act is enacted and to participate across issuance and distribution. If needed, it will consider mergers and acquisitions across payments and investment, the company said. “The goal is to make a won-denominated stablecoin as convenient to use as withdrawing funds from an account,” Yoon said. “If there is a suitable company, we will actively look for M&A opportunities.” 2026-04-08 15:57:17 -

KakaoBank to Lead App Development for Thailand’s BankX Virtual Bank, Set Up New Base in Mongolia KakaoBank will lead overall development of the mobile app for Thailand’s virtual bank BankX, which is set to begin operations in the first half of next year. The company is also accelerating its overseas push by choosing Mongolia as a new base in Southeast Asia. It also plans to flesh out an “AI-native bank” strategy built around hyper-personalized AI services. KakaoBank CEO Yun Ho-young outlined the plan at a news conference Tuesday at a hotel in Seoul’s Yeouido district. “Using AI technology, we will provide a financial secretary optimized for everyone, and expand our stage worldwide to write the history of financial innovation,” Yun said. KakaoBank is currently working with Indonesia’s Superbank to apply its digital banking operating know-how locally. Superbank listed on the Indonesia Stock Exchange late last year and has become the country’s top digital bank by market capitalization. In Thailand, KakaoBank is preparing to launch virtual bank operations in the first half of next year through BankX, a joint venture set up with the SCBX Group. KakaoBank plans to bring to Thailand signature products that have succeeded at home, including its “26-week savings” and “group account” offerings. It said it will directly lead mobile app development, aiming to export its capability to build a digital banking platform rather than provide advice alone. KakaoBank also selected Mongolia as a new overseas base. Working with local financial institutions, it plans to share know-how behind its credit scoring system, “KakaoBank Score,” which uses nonfinancial data to assess creditworthiness. The company also presented an AI-based roadmap for its app. In the second quarter, it plans to add an in-app “investment” tab to help customers compare and invest in a range of financial products using AI. In the third quarter, it plans to apply AI to its “payments home” feature and roll out a “personalized spending management service” that proactively suggests ways to manage expenses based on customers’ payment data. KakaoBank said it also plans to enter the retirement pension market and expand into a “lifetime asset management” service spanning customers from their 20s and 30s to seniors. The goal is to evolve into a “financial secretary” platform that recommends needed services first, rather than simply offering more functions. “As a financial app adds more functions, customers face the ‘paradox of expansion,’ where it becomes harder to find what they need,” Yun said. “The future KakaoBank is pursuing is one where AI identifies and solves complex financial problems first.”* This article has been translated by AI. 2026-04-08 10:03:29

KakaoBank to Lead App Development for Thailand’s BankX Virtual Bank, Set Up New Base in Mongolia KakaoBank will lead overall development of the mobile app for Thailand’s virtual bank BankX, which is set to begin operations in the first half of next year. The company is also accelerating its overseas push by choosing Mongolia as a new base in Southeast Asia. It also plans to flesh out an “AI-native bank” strategy built around hyper-personalized AI services. KakaoBank CEO Yun Ho-young outlined the plan at a news conference Tuesday at a hotel in Seoul’s Yeouido district. “Using AI technology, we will provide a financial secretary optimized for everyone, and expand our stage worldwide to write the history of financial innovation,” Yun said. KakaoBank is currently working with Indonesia’s Superbank to apply its digital banking operating know-how locally. Superbank listed on the Indonesia Stock Exchange late last year and has become the country’s top digital bank by market capitalization. In Thailand, KakaoBank is preparing to launch virtual bank operations in the first half of next year through BankX, a joint venture set up with the SCBX Group. KakaoBank plans to bring to Thailand signature products that have succeeded at home, including its “26-week savings” and “group account” offerings. It said it will directly lead mobile app development, aiming to export its capability to build a digital banking platform rather than provide advice alone. KakaoBank also selected Mongolia as a new overseas base. Working with local financial institutions, it plans to share know-how behind its credit scoring system, “KakaoBank Score,” which uses nonfinancial data to assess creditworthiness. The company also presented an AI-based roadmap for its app. In the second quarter, it plans to add an in-app “investment” tab to help customers compare and invest in a range of financial products using AI. In the third quarter, it plans to apply AI to its “payments home” feature and roll out a “personalized spending management service” that proactively suggests ways to manage expenses based on customers’ payment data. KakaoBank said it also plans to enter the retirement pension market and expand into a “lifetime asset management” service spanning customers from their 20s and 30s to seniors. The goal is to evolve into a “financial secretary” platform that recommends needed services first, rather than simply offering more functions. “As a financial app adds more functions, customers face the ‘paradox of expansion,’ where it becomes harder to find what they need,” Yun said. “The future KakaoBank is pursuing is one where AI identifies and solves complex financial problems first.”* This article has been translated by AI. 2026-04-08 10:03:29 -

Online P2P lenders seek looser investment caps as cumulative loans near 20 trillion won Online investment-linked finance firms, known as on-tu-eop, are calling for deregulation — including higher investment caps for retail investors — to improve profitability and expand inclusive finance. With cumulative lending nearing 20 trillion won, the sector is increasingly seen as an alternative source of credit, drawing attention to whether talks on easing rules will gain momentum. According to the financial industry, the sector held a policy forum at the National Assembly on March 26 under the theme of measures to revitalize online investment-linked finance. The business connects investors and borrowers through online platforms. Investors participate in loans and earn returns through claims to principal and interest. After the relevant law took effect in 2020, the sector was brought into the regulated financial system. Recently, through linked investments with savings banks, firms have supplied midrate credit loans averaging in the 12% range to borrowers in the bottom 50% of personal credit scores, serving as a channel for working-class lending. At the forum, participants highlighted the need to broaden institutional investor participation and raise investment limits for individuals. Institutional investors are currently capped at 40% of investment per loan. The limit for general retail investors is 40 million won, while products tied to real estate-collateralized loans are capped at 20 million won. Lee Hyo-jin, CEO of 8percent, said the sector differs from traditional banks because it relies on transaction fees rather than net interest margins, meaning higher volume directly supports growth. “If we expand transaction volume through easing investment regulations, a virtuous cycle is possible — more funding supply, lower rates and stronger demand,” Lee said. He added that improving the operating environment is needed to meet policy goals such as spreading inclusive finance and supporting financial innovation. Speakers also called for expanding the scope of loans eligible for linked investment by lending institutions. Lee Jung-min, an attorney at Kim & Chang, said linked-investment products are currently limited to personal credit loans where risk can be managed. “Given the purpose of the On-tu Act to supply midrate financing to blind spots in lending, the scope should be expanded to include loans to sole proprietors, where funding demand is high,” he said. Other proposals included easing limits on on-tu firms’ own-capital investments and restructuring investment frameworks. Financial authorities and some experts urged caution. Jeong Seon-in, director of digital finance at the Financial Services Commission, said investment risks can emerge years later, requiring a careful approach. “Efforts to strengthen qualitative management and build trust must go hand in hand,” Jeong said. Seo Byeong-ho, head of the Financial Innovation Research Division at the Korea Institute of Finance, noted that deregulation such as raising minimum capital requirements was implemented in 2022 and 2023, and said the focus now should be on boosting trust, including stronger disclosure. 2026-03-26 15:24:00

Online P2P lenders seek looser investment caps as cumulative loans near 20 trillion won Online investment-linked finance firms, known as on-tu-eop, are calling for deregulation — including higher investment caps for retail investors — to improve profitability and expand inclusive finance. With cumulative lending nearing 20 trillion won, the sector is increasingly seen as an alternative source of credit, drawing attention to whether talks on easing rules will gain momentum. According to the financial industry, the sector held a policy forum at the National Assembly on March 26 under the theme of measures to revitalize online investment-linked finance. The business connects investors and borrowers through online platforms. Investors participate in loans and earn returns through claims to principal and interest. After the relevant law took effect in 2020, the sector was brought into the regulated financial system. Recently, through linked investments with savings banks, firms have supplied midrate credit loans averaging in the 12% range to borrowers in the bottom 50% of personal credit scores, serving as a channel for working-class lending. At the forum, participants highlighted the need to broaden institutional investor participation and raise investment limits for individuals. Institutional investors are currently capped at 40% of investment per loan. The limit for general retail investors is 40 million won, while products tied to real estate-collateralized loans are capped at 20 million won. Lee Hyo-jin, CEO of 8percent, said the sector differs from traditional banks because it relies on transaction fees rather than net interest margins, meaning higher volume directly supports growth. “If we expand transaction volume through easing investment regulations, a virtuous cycle is possible — more funding supply, lower rates and stronger demand,” Lee said. He added that improving the operating environment is needed to meet policy goals such as spreading inclusive finance and supporting financial innovation. Speakers also called for expanding the scope of loans eligible for linked investment by lending institutions. Lee Jung-min, an attorney at Kim & Chang, said linked-investment products are currently limited to personal credit loans where risk can be managed. “Given the purpose of the On-tu Act to supply midrate financing to blind spots in lending, the scope should be expanded to include loans to sole proprietors, where funding demand is high,” he said. Other proposals included easing limits on on-tu firms’ own-capital investments and restructuring investment frameworks. Financial authorities and some experts urged caution. Jeong Seon-in, director of digital finance at the Financial Services Commission, said investment risks can emerge years later, requiring a careful approach. “Efforts to strengthen qualitative management and build trust must go hand in hand,” Jeong said. Seo Byeong-ho, head of the Financial Innovation Research Division at the Korea Institute of Finance, noted that deregulation such as raising minimum capital requirements was implemented in 2022 and 2023, and said the focus now should be on boosting trust, including stronger disclosure. 2026-03-26 15:24:00 -

Survey: 7 in 10 South Korean fintech firms operate without e-finance registration South Korea’s payment gateway (PG) industry is expanding rapidly, but about seven in 10 fintech companies are operating without registering as an electronic financial business, a new survey found. Despite tighter oversight of PG operators, many firms still take part in payment functions outside the regulatory system, raising concerns about blind spots in supervision. According to the Korea Fintech Industry Association’s “2025 Fintech Industry Survey,” released Monday, only 32% of 322 surveyed fintech companies were registered as electronic financial businesses. Another 64.3% were operating without registration, and 3.7% said they were considering registering. The association said this was the first time results of a full survey on fintech firms’ registration status had been made public. The survey covered a wide range of fintech fields — including payments, wealth management, insurtech and IT and solution providers — so the unregistered share does not necessarily equal the unregistered share among firms that are required to register. Under the Electronic Financial Transactions Act, businesses that provide services such as simple payments, prepaid top-ups and settlement must register with financial authorities. Operating without registration can be punished by up to three years in prison or a fine of up to 20 million won. Critics have said the law’s narrow definition of PG business leaves gaps, including for “dual-business” PG operators that run their main business — such as online marketplace brokerage — while also handling settlements as a side activity. Industry officials also argue that registration requirements — including capital, staffing and security systems — can be a high barrier for early-stage startups. Some companies say they only provide technology and do not directly control the flow of funds, and therefore interpret themselves as not subject to registration. Registration rates varied sharply by industry. Financial-sector firms, which have traditionally provided financial functions, showed a 59.2% registration rate. By contrast, information and communications firms and software/IT firms posted rates of 13.9% and 20.5%, respectively. The report attributed this in part to IT-based companies defining their services as “technology services” while in practice performing PG-like functions such as accepting payments or handling settlements without registering. The report warned that as platform-based payment ecosystems expand, more businesses are becoming involved in payment and settlement processes while remaining outside the scope of electronic financial business registration, increasing the risk of consumer harm. On some online platforms, consumers may feel they are paying through the platform itself, but settlements are often handled by a separate PG firm or financial institution. When payment delays or refund disputes arise, users may struggle to identify who is responsible, delaying relief, the report said. The report also found growth in “PG-like” firms that remain outside regulation, particularly among electronic financial support providers — which assist financial institutions with IT systems, data processing, security and authentication — and among “third-tier PG firms.” It defined third-tier PG firms as reseller or agency-type businesses that re-sell services based on contracts with second-tier PG firms. A fintech industry official said that when businesses in the regulatory gray zone cause incidents, the fallout can spread across the entire industry. The official called for steps to improve transparency, including tightening rules to bring gray-zone operators into the system or blocking unqualified firms from entering the market. 2026-03-24 10:03:07

Survey: 7 in 10 South Korean fintech firms operate without e-finance registration South Korea’s payment gateway (PG) industry is expanding rapidly, but about seven in 10 fintech companies are operating without registering as an electronic financial business, a new survey found. Despite tighter oversight of PG operators, many firms still take part in payment functions outside the regulatory system, raising concerns about blind spots in supervision. According to the Korea Fintech Industry Association’s “2025 Fintech Industry Survey,” released Monday, only 32% of 322 surveyed fintech companies were registered as electronic financial businesses. Another 64.3% were operating without registration, and 3.7% said they were considering registering. The association said this was the first time results of a full survey on fintech firms’ registration status had been made public. The survey covered a wide range of fintech fields — including payments, wealth management, insurtech and IT and solution providers — so the unregistered share does not necessarily equal the unregistered share among firms that are required to register. Under the Electronic Financial Transactions Act, businesses that provide services such as simple payments, prepaid top-ups and settlement must register with financial authorities. Operating without registration can be punished by up to three years in prison or a fine of up to 20 million won. Critics have said the law’s narrow definition of PG business leaves gaps, including for “dual-business” PG operators that run their main business — such as online marketplace brokerage — while also handling settlements as a side activity. Industry officials also argue that registration requirements — including capital, staffing and security systems — can be a high barrier for early-stage startups. Some companies say they only provide technology and do not directly control the flow of funds, and therefore interpret themselves as not subject to registration. Registration rates varied sharply by industry. Financial-sector firms, which have traditionally provided financial functions, showed a 59.2% registration rate. By contrast, information and communications firms and software/IT firms posted rates of 13.9% and 20.5%, respectively. The report attributed this in part to IT-based companies defining their services as “technology services” while in practice performing PG-like functions such as accepting payments or handling settlements without registering. The report warned that as platform-based payment ecosystems expand, more businesses are becoming involved in payment and settlement processes while remaining outside the scope of electronic financial business registration, increasing the risk of consumer harm. On some online platforms, consumers may feel they are paying through the platform itself, but settlements are often handled by a separate PG firm or financial institution. When payment delays or refund disputes arise, users may struggle to identify who is responsible, delaying relief, the report said. The report also found growth in “PG-like” firms that remain outside regulation, particularly among electronic financial support providers — which assist financial institutions with IT systems, data processing, security and authentication — and among “third-tier PG firms.” It defined third-tier PG firms as reseller or agency-type businesses that re-sell services based on contracts with second-tier PG firms. A fintech industry official said that when businesses in the regulatory gray zone cause incidents, the fallout can spread across the entire industry. The official called for steps to improve transparency, including tightening rules to bring gray-zone operators into the system or blocking unqualified firms from entering the market. 2026-03-24 10:03:07 -

Why South Korea’s Internet Banks Sat Out Bank of Korea’s ‘Project Hangang’ CBDC Test As the Bank of Korea moves ahead with the second phase of its central bank digital currency experiment, known as “Project Hangang,” attention is turning to why South Korea’s internet-only banks are not taking part. Industry officials cite weak profitability, high upfront costs and limited interoperability as key factors that reduced incentives to join. According to the financial sector on Thursday, the country’s three internet banks did not express an intention to participate in the second-phase program. Project Hangang is a test in which the central bank issues a blockchain-based “wholesale digital currency,” and private banks distribute it as a payment instrument called “deposit tokens,” allowing consumers to use them in everyday transactions. Nine banks will participate in the second phase: the seven banks that joined the first phase — KB Kookmin, Shinhan, Woori, Hana, IBK and NH NongHyup, and Busan Bank — plus Kyongnam Bank and iM Bank. Kim Dong-seop, head of the Bank of Korea’s digital currency planning team, said at a briefing the previous day that the central bank did not proceed by selecting some banks and excluding others. He said internet banks likely had “various considerations,” including internal circumstances and priorities. Industry observers say the project’s unclear revenue model, combined with heavy initial infrastructure spending, likely discouraged participation. They argue that while a privately led stablecoin market can create both a risk of losing deposit customers and an opportunity to capture a new market, the central bank’s model does not present banks with a clear profit structure. During the first real-transaction test, conducted for two months starting in April last year, the seven participating commercial banks were reported to have spent nearly 35 billion won on infrastructure such as computer systems and on marketing for the project. Skepticism also remains over user convenience. The central bank says it simplified payment procedures in the first phase by introducing features such as biometric authentication. But internet banks and big tech firms that already offer advanced “face pay” and other streamlined payment services do not see it as a distinct innovation, according to industry assessments. Criticism has also focused on the technical design. The Bank of Korea expects distributed ledger technology, including blockchain, to help prevent misuse of deposit tokens. However, industry officials argue the system is effectively centralized and could paralyze the entire payment network if problems arise at the central bank. Internet banks say they will monitor market reaction to the second test before deciding whether to join later, but many in the industry expect participation is unlikely. One industry official said the first project failed because it lacked interoperability. “If the goal is a digital currency that works globally, linking with dollar stablecoins and the like is important, but the second project also has no interoperability,” the official said. The official added that there are no internationally successful cases of a centralized deposit-token system based on a permissioned blockchain, and said banks have reason to be cautious because the revenue model and operating costs are uncertain and could become a “sinkhole of sunk costs.”* This article has been translated by AI. 2026-03-19 17:03:00

Why South Korea’s Internet Banks Sat Out Bank of Korea’s ‘Project Hangang’ CBDC Test As the Bank of Korea moves ahead with the second phase of its central bank digital currency experiment, known as “Project Hangang,” attention is turning to why South Korea’s internet-only banks are not taking part. Industry officials cite weak profitability, high upfront costs and limited interoperability as key factors that reduced incentives to join. According to the financial sector on Thursday, the country’s three internet banks did not express an intention to participate in the second-phase program. Project Hangang is a test in which the central bank issues a blockchain-based “wholesale digital currency,” and private banks distribute it as a payment instrument called “deposit tokens,” allowing consumers to use them in everyday transactions. Nine banks will participate in the second phase: the seven banks that joined the first phase — KB Kookmin, Shinhan, Woori, Hana, IBK and NH NongHyup, and Busan Bank — plus Kyongnam Bank and iM Bank. Kim Dong-seop, head of the Bank of Korea’s digital currency planning team, said at a briefing the previous day that the central bank did not proceed by selecting some banks and excluding others. He said internet banks likely had “various considerations,” including internal circumstances and priorities. Industry observers say the project’s unclear revenue model, combined with heavy initial infrastructure spending, likely discouraged participation. They argue that while a privately led stablecoin market can create both a risk of losing deposit customers and an opportunity to capture a new market, the central bank’s model does not present banks with a clear profit structure. During the first real-transaction test, conducted for two months starting in April last year, the seven participating commercial banks were reported to have spent nearly 35 billion won on infrastructure such as computer systems and on marketing for the project. Skepticism also remains over user convenience. The central bank says it simplified payment procedures in the first phase by introducing features such as biometric authentication. But internet banks and big tech firms that already offer advanced “face pay” and other streamlined payment services do not see it as a distinct innovation, according to industry assessments. Criticism has also focused on the technical design. The Bank of Korea expects distributed ledger technology, including blockchain, to help prevent misuse of deposit tokens. However, industry officials argue the system is effectively centralized and could paralyze the entire payment network if problems arise at the central bank. Internet banks say they will monitor market reaction to the second test before deciding whether to join later, but many in the industry expect participation is unlikely. One industry official said the first project failed because it lacked interoperability. “If the goal is a digital currency that works globally, linking with dollar stablecoins and the like is important, but the second project also has no interoperability,” the official said. The official added that there are no internationally successful cases of a centralized deposit-token system based on a permissioned blockchain, and said banks have reason to be cautious because the revenue model and operating costs are uncertain and could become a “sinkhole of sunk costs.”* This article has been translated by AI. 2026-03-19 17:03:00 -

KakaoBank Cuts Rates on Real Estate-Backed Loans for Sole Proprietors to Low 2% Range KakaoBank said on 17 it will cut interest rates on its “real estate-backed loans for sole proprietors” by as much as 0.75 percentage points to ease financing burdens for small business owners. The bank said it will lower loan rates by up to 0.60 points and expand its preferential rate discount to 0.30 points a year from 0.15. With both applied, the minimum rate is 2.895% a year. KakaoBank said it is the only financial firm offering rates in the 2% range among banks providing real estate-backed loans to sole proprietors. KakaoBank launched the product in October last year. It can be used non-face-to-face for up to 1 billion won for purposes including business operating funds and purchasing a business site. Some industries, including residential building development and supply and residential building rental, are excluded. “We further lowered rates on our real estate-backed loans for sole proprietors to expand financial support for small business owners struggling to raise funds,” KakaoBank said, adding it will continue to introduce innovative financial services to improve convenience for sole proprietor customers.* This article has been translated by AI. 2026-03-17 08:42:00

KakaoBank Cuts Rates on Real Estate-Backed Loans for Sole Proprietors to Low 2% Range KakaoBank said on 17 it will cut interest rates on its “real estate-backed loans for sole proprietors” by as much as 0.75 percentage points to ease financing burdens for small business owners. The bank said it will lower loan rates by up to 0.60 points and expand its preferential rate discount to 0.30 points a year from 0.15. With both applied, the minimum rate is 2.895% a year. KakaoBank said it is the only financial firm offering rates in the 2% range among banks providing real estate-backed loans to sole proprietors. KakaoBank launched the product in October last year. It can be used non-face-to-face for up to 1 billion won for purposes including business operating funds and purchasing a business site. Some industries, including residential building development and supply and residential building rental, are excluded. “We further lowered rates on our real estate-backed loans for sole proprietors to expand financial support for small business owners struggling to raise funds,” KakaoBank said, adding it will continue to introduce innovative financial services to improve convenience for sole proprietor customers.* This article has been translated by AI. 2026-03-17 08:42:00 -

Korean Internet Banks’ Boards Rarely Dissent Despite 70% Outside Directors South Korea’s internet-only banks have boards where outside directors make up nearly 70%, yet most agenda items are still approved unanimously, according to a review of recent filings. Over the past three years, Toss Bank recorded the most dissenting votes, but only six in total. Industry observers say the boards’ oversight role is unlikely to strengthen unless the process for recommending outside directors changes. An analysis of the past three years of “annual reports on governance and compensation systems” for the three internet-only banks — Toss Bank, K Bank and KakaoBank — posted on the Korea Federation of Banks website showed Toss Bank had five dissenting opinions last year and one in 2024, for six overall. At Toss Bank, five dissenting opinions were recorded among 119 board resolutions last year. Four were raised at a January board meeting by Lee Kun-ho, an outside director and a former KB Kookmin Bank president. Lee opposed approval of a 2025 stock option grant plan; convening a first extraordinary shareholders meeting in 2025 and setting the record date; approval of canceling stock option grants; and an agenda item to revise internal rules. Since launching in 2021, Toss Bank has granted stock options to employees in 19 rounds through September last year. In April last year, it introduced a program allowing employees to swap part of their year-end bonus (1 million won) for stock options. The stock options included a condition barring resignation for two years, and 372 of about 700 regular employees reportedly chose the program. The industry has speculated that disagreements may have surfaced on the board during the process of adopting the program. K Bank, despite having the highest outside-director ratio at 73%, had no dissenting votes on board resolutions over the past three years, the analysis found. KakaoBank recorded two dissenting opinions over the same period. In 2023, outside director Lee Eun-kyung opposed agenda items on support measures for victims of rental fraud and approval of revisions to a shared-growth agreement. There was also one case in which an item was put on hold: In June last year, directors agreed to defer a proposal on an affiliate contract for employee corporate and welfare card use, citing the need for additional review and discussion. The resolution was later taken up at the eighth board meeting. Kim Dae-jong, a professor in the business administration department at Sejong University, said outside directors are selected by bank employees, creating a structure in which “they have no choice but to agree close to 100%,” making dissent effectively difficult. 2026-03-12 15:18:00

Korean Internet Banks’ Boards Rarely Dissent Despite 70% Outside Directors South Korea’s internet-only banks have boards where outside directors make up nearly 70%, yet most agenda items are still approved unanimously, according to a review of recent filings. Over the past three years, Toss Bank recorded the most dissenting votes, but only six in total. Industry observers say the boards’ oversight role is unlikely to strengthen unless the process for recommending outside directors changes. An analysis of the past three years of “annual reports on governance and compensation systems” for the three internet-only banks — Toss Bank, K Bank and KakaoBank — posted on the Korea Federation of Banks website showed Toss Bank had five dissenting opinions last year and one in 2024, for six overall. At Toss Bank, five dissenting opinions were recorded among 119 board resolutions last year. Four were raised at a January board meeting by Lee Kun-ho, an outside director and a former KB Kookmin Bank president. Lee opposed approval of a 2025 stock option grant plan; convening a first extraordinary shareholders meeting in 2025 and setting the record date; approval of canceling stock option grants; and an agenda item to revise internal rules. Since launching in 2021, Toss Bank has granted stock options to employees in 19 rounds through September last year. In April last year, it introduced a program allowing employees to swap part of their year-end bonus (1 million won) for stock options. The stock options included a condition barring resignation for two years, and 372 of about 700 regular employees reportedly chose the program. The industry has speculated that disagreements may have surfaced on the board during the process of adopting the program. K Bank, despite having the highest outside-director ratio at 73%, had no dissenting votes on board resolutions over the past three years, the analysis found. KakaoBank recorded two dissenting opinions over the same period. In 2023, outside director Lee Eun-kyung opposed agenda items on support measures for victims of rental fraud and approval of revisions to a shared-growth agreement. There was also one case in which an item was put on hold: In June last year, directors agreed to defer a proposal on an affiliate contract for employee corporate and welfare card use, citing the need for additional review and discussion. The resolution was later taken up at the eighth board meeting. Kim Dae-jong, a professor in the business administration department at Sejong University, said outside directors are selected by bank employees, creating a structure in which “they have no choice but to agree close to 100%,” making dissent effectively difficult. 2026-03-12 15:18:00 -

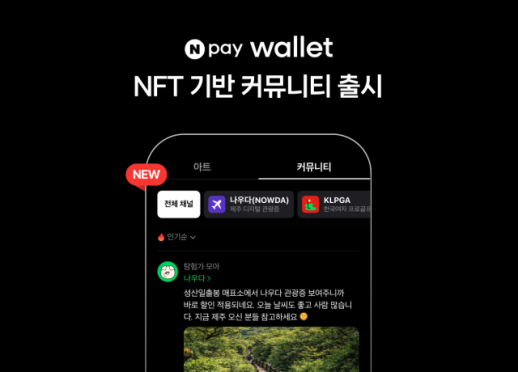

Naver Pay Launches NFT-Based Community Features in Npay Wallet Naver Pay said on March 12 it has launched a new community service based on non-fungible tokens, or NFTs, within its non-custodial digital asset wallet, Npay Wallet. Npay Wallet is a digital asset wallet designed to securely store digital art, tickets and certificates. The new Npay Wallet Community is built around NFTs and is intended to let users connect through shared interests. In the community's "channels," users can freely discuss specific topics, including Jeju Island's digital tourism pass, "Nauda," and game streams on Naver's streaming service, "Chzzk." By contrast, "ticket verification rooms" are operated as closed groups open only to holders of tickets and related NFTs for specific performances or events, including the KLPGA (Korea Ladies Professional Golf Association). The company said the goal is to help attendees form communities and increase engagement and a sense of being on site. Naver Pay said it plans to expand the community to additional content areas, including sports, games and performances, using NFTs. Starting March 31, it plans community events tied to Chzzk game broadcasts to offer a participatory experience that combines watching matches with fan interaction. To mark the launch, Naver Pay is also running an open promotion. Users who complete three missions in the community — liking posts, leaving comments and writing posts — can receive 1,000 won in Npay points. Those who post NFT verification content will be entered in a drawing for up to 50,000 won in additional points. An official at Naver Pay said, "Npay Wallet will expand beyond a digital wallet that stores NFTs into a platform that also provides community experiences where various events and fandom activities take place." * This article has been translated by AI. 2026-03-12 14:33:00

Naver Pay Launches NFT-Based Community Features in Npay Wallet Naver Pay said on March 12 it has launched a new community service based on non-fungible tokens, or NFTs, within its non-custodial digital asset wallet, Npay Wallet. Npay Wallet is a digital asset wallet designed to securely store digital art, tickets and certificates. The new Npay Wallet Community is built around NFTs and is intended to let users connect through shared interests. In the community's "channels," users can freely discuss specific topics, including Jeju Island's digital tourism pass, "Nauda," and game streams on Naver's streaming service, "Chzzk." By contrast, "ticket verification rooms" are operated as closed groups open only to holders of tickets and related NFTs for specific performances or events, including the KLPGA (Korea Ladies Professional Golf Association). The company said the goal is to help attendees form communities and increase engagement and a sense of being on site. Naver Pay said it plans to expand the community to additional content areas, including sports, games and performances, using NFTs. Starting March 31, it plans community events tied to Chzzk game broadcasts to offer a participatory experience that combines watching matches with fan interaction. To mark the launch, Naver Pay is also running an open promotion. Users who complete three missions in the community — liking posts, leaving comments and writing posts — can receive 1,000 won in Npay points. Those who post NFT verification content will be entered in a drawing for up to 50,000 won in additional points. An official at Naver Pay said, "Npay Wallet will expand beyond a digital wallet that stores NFTs into a platform that also provides community experiences where various events and fandom activities take place." * This article has been translated by AI. 2026-03-12 14:33:00