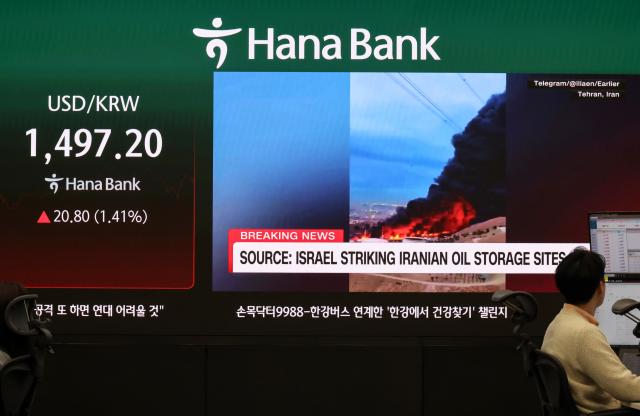

SEOUL, March 16-South Korea’s financial markets have swung sharply as the U.S.-Iran war rattles investors, with the won-dollar exchange rate hovering around 1,500 won per dollar.

Disruptions to Middle East crude supplies have pushed fuel prices higher, prompting the first oil price-control measures in 30 years. With global logistics strained, exporters and importers face growing uncertainty over when and where shipments of key products and raw materials may be delayed.

The Korean economy, which had been showing signs of emerging from a prolonged slump on the back of a semiconductor boom and a strong stock market, is now being shaken by the crisis in the Middle East.

The regional turmoil, triggered by U.S. airstrikes on Iran, has highlighted how exposed a small, open economy can be when geopolitics turn volatile. Milestones that had impressed global investors — including the Kospi topping 6,000 and exports reaching $700 billion, the world’s sixth-largest total — now appear less reassuring against the reality of vulnerability to external shocks.

South Korea imports all of its crude oil and relies on Middle Eastern producers for more than 70 percent of supply. When the region becomes unstable or prices surge, the country has limited buffers. After each bout of Middle East turmoil since the oil shocks of the 1970s, South Korea has pledged to diversify suppliers, only to ease off once the immediate pressure faded.

As industry has become more advanced, sensitivity to oil prices has grown. Semiconductors, petrochemicals, steel and autos — pillars of manufacturing — are closely tied to energy supply, leaving export competitiveness vulnerable to higher oil costs. What initially looked like a threat concentrated in refining and petrochemicals has spread across industries including autos, home appliances and chips, as concerns rise over a possible closure of the Strait of Hormuz.

If global consumption weakens and sales of finished goods such as cars and smartphones slow, the broader parts ecosystem would also suffer. Even the semiconductor supercycle that helped lead the recovery and lifted the Kospi could lose momentum.

After the Kospi crossed 6,000, South Korea briefly ranked ninth globally by total market capitalization. The latest turmoil has underscored the limits of an emerging market prone to sharp swings and heavily influenced by foreign investors. While nearby markets in China, Japan and Taiwan moved within roughly 2 to 3 percent, the Kospi posted roller-coaster sessions with daily moves of around 10 percent. Even if panic subsides once the war eases, questions may linger about whether the market’s investment mechanisms are functioning as they should.

The exchange rate has neared the psychological threshold of 1,500 won per dollar, its highest level since the 2008 global financial crisis. Rising oil prices, a falling Kospi, foreign outflows, energy supply-chain risks and fears of production disruptions in key export industries have combined to weaken the won. As uncertainty over the economic outlook grows, the currency has struggled to maintain stability in foreign-exchange markets.

World oil prices have surged amid threats to close the Strait of Hormuz, through which about one-fifth of global crude supply passes. Higher fuel costs are already feeding into everyday prices. Under government pressure as it steps up price monitoring, food companies have lowered or plan to lower prices for items including flour, cooking oil, bread and instant noodles. Still, many consumers say grocery bills already feel far higher than official figures suggest.

The war has left South Korea grappling with a “three highs” problem: high oil prices, a high exchange rate and high inflation. If policymakers fail to contain this combination, the risk of stagflation — inflation alongside economic stagnation — could rise.

These three pressures reinforce one another. Higher oil prices worsen the current account and place further pressure on the won while also raising household fuel and energy costs. A weaker currency combined with higher crude prices lifts import costs and inflation, while expensive oil can intensify demand for safe assets, adding further downward pressure on the won.

The “three highs” can curb consumption, shrink the current account surplus and slow economic growth. The Bank of Korea has forecast 1.9 percent growth this year, but that estimate assumed oil prices at around $62 per barrel.

Hyundai Research Institute warned that if oil rises to $100 a barrel, growth could fall by 0.3 percentage points, and if it reaches $150, growth could drop by 0.8 points. The International Energy Agency has announced the release of a record 400 million barrels from strategic reserves, yet oil has remained above $100 as Iran repeatedly declares it could close the Strait of Hormuz.

When the Middle East has produced an oil shock in the past, South Korea has often faced severe economic strain.

During the second oil shock triggered by Iran’s 1979 revolution, global oil prices jumped from $15 a barrel to $39, while domestic prices rose nearly 30 percent in 1980 alone. In July 2008, oil climbed to $150 amid rising energy demand in emerging markets and heightened geopolitical risks in the Middle East. The surge contributed to a global pullback in consumption and investment, culminating in a financial crisis that also hit South Korea hard.

This time, the risk is compounded by simultaneous turmoil in financial markets and potential damage to the real economy. If the conflict drags on, the shock to the global economy could prove far larger than expected, and familiar crisis playbooks may not work. As military clashes between the United States and Iran intensify, some fear an economic tsunami from what could become the first oil shock of the 21st century.

For energy-importing countries such as South Korea, even a short-term oil spike can worsen trade terms and reduce the current account surplus, slowing growth. It can sharply raise costs across industry, triggering a chain reaction that weakens production, consumption, investment and employment. If authorities respond too slowly, the country could fall into a stagflation spiral — higher oil prices leading to a weaker current account, a weaker currency, rising import prices and an economic downturn.

When growth slows, policymakers typically cut rates or expand fiscal spending. But if inflation rises simultaneously, they may instead need to raise rates or tighten policy. That creates a difficult dilemma between supporting growth and stabilizing prices. The Bank of Korea said on March 12 that Middle East instability could push prices higher but that it would maintain a “cautious neutral stance,” reflecting the difficulty of setting a clear monetary-policy direction.

In emergencies such as war or major disasters, the government may need to act pre-emptively and decisively beyond normal market expectations. The immediate priority is to contain the “three highs” early and prevent stagflation from taking hold. Authorities should make efficient use of the 100 trillion won financial market stabilization fund to maintain liquidity while directing support toward vulnerable groups and small business owners hit by rising fuel costs.

The crisis also represents the first major economic test for the Lee Jae Myung government since it took office. The administration’s move to prepare an early supplementary budget of up to 20 trillion won is a rapid step to secure policy resources. Lee said, “We must not waste the golden time to ease the shock to the people’s livelihoods,” urging officials to accelerate the execution of the supplementary budget.

The supplementary budget should remain focused on its stated purpose as an “oil-price supplementary budget” while carefully monitoring inflation pressures, to avoid criticism of election-driven spending ahead of local elections. The government has cited several areas requiring fiscal support, including freezing public utility fees, cutting fuel taxes, expanding discounts for agricultural, livestock and fisheries products, and providing fuel subsidies for freight trucks.

To minimize the fallout from the Middle East crisis and soften the blow to the real economy from higher oil prices, spending should remain selective and targeted. How the budget is drafted and implemented will test the government’s policy capacity and credibility.

Even if delayed, South Korea should not postpone diversifying crude oil and natural gas import sources beyond the Middle East to regions such as Africa and South America. Energy diversification must remain a long-term national priority.

The Middle East crisis has once again exposed structural weaknesses hidden behind headline economic numbers. It underscores the need for a sober reassessment of South Korea’s economy — including its stock market — and for building greater resilience against external shocks.

*The author is an editorial adviser for the Aju Business Daily.

![[박원재 논설고문]](https://image.ajunews.com/content/image/2025/05/15/20250515081937591195.jpg)

About the author:

▷MBA, Aalto University, Finland ▷Former Tokyo correspondent, editorial writer and business editor at The Dong-A Ilbo ▷Former CEO of Donga.com ▷Former president, Korea Online Newspaper Association ▷Professor at Kyungsung University (current)

Copyright ⓒ Aju Press All rights reserved.