SEOUL, Mar. 17 (AJP) - South Korea’s National Assembly is scrambling to fast-track a package of exchange-rate support bills after sitting on them for months as the won comes under renewed pressure from the widening Gulf war.

The urgency reflects not just broad dollar strength but a sharper loss of confidence in the won itself.

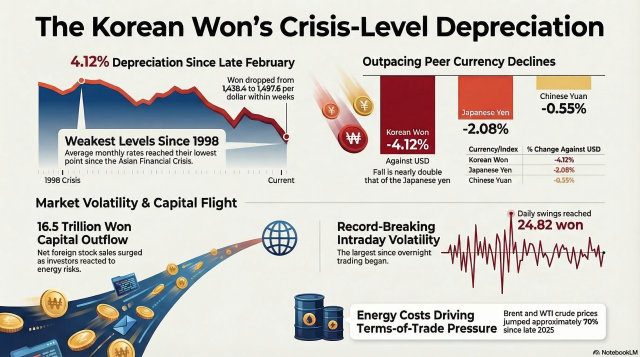

According to the Financial Supervisory Service, the won weakened 4.12 percent against the dollar as of Monday from end-February, before the war erupted, with the rate rising from 1,438.4 won to 1,497.6 won.

That compares with a 2.82 percent rise in the Dollar Index over the same period and a 2.08 percent gain in the dollar against the Japanese yen — even as the two neighboring economies share similar exposure to disruptions in the Strait of Hormuz. China’s yuan, also dependent on Gulf shipping routes, moved only 0.55 percent.

The scale of the move has reinforced market concerns that Korea is being punished more severely than its peers, reflecting heavier foreign outflows from local equities that had outperformed prior to the war.

The won-dollar exchange rate averaged 1,476.9 won this month, the highest monthly level since the 1998 Asian financial crisis, while last week’s average climbed to 1,480.7 won.

The currency briefly breached the 1,500 won threshold in daytime trading on Monday for the first time since the global financial crisis, triggering speculation authorities may have given up 1,500-won defense.

"We are not 100 percent sure about intervention. But the dollar has retreated. It can be attributed to the easing in bond yields," said one trader on Tuesday.

The dollar eased to 1,493.40 won as of 4:00 p.m. in Seoul.

Volatility still has been topping peers. The won’s average daily swing widened to 14.24 won, the largest since the 2010 euro-area sovereign debt crisis, while intraday moves stretched to 24.82 won — the biggest since Korea introduced overnight foreign-exchange trading.

Foreign investors are reacting more sensitively to Korea’s exposure to Gulf energy risks and surging oil prices.

Brent crude jumped 42.3 percent from end-February to March 16, to $103.14 a barrel, while WTI surged 47.28 percent to $98.71. Compared with end-2025, Brent is up 69.5 percent and WTI 71.91 percent.

Those terms-of-trade pressures are now feeding directly into Korean asset markets. Foreign investors sold a net 16.5 trillion won worth of Korean stocks in March through March 16, including 16.1 trillion won from the KOSPI alone, according to the same FSS data.

Korea’s five-year sovereign CDS premium also widened to 28.9 basis points from 24.6 basis points at end-February.

Only after the exchange rate broke above 1,500 won did the legislature move to advance the so-called “Triple Exchange Rate Stability Acts.”

On Monday, the Tax Subcommittee of the Strategy and Finance Committee approved the package, which includes amendments to the Restriction of Special Taxation Act and the Special Tax for Rural Development Act. Having cleared the subcommittee, the bills are expected to go before the full committee on Tuesday and then to a plenary session on March 19.

The measures were first proposed on Jan. 3 by Rep. Jung Tae-ho of the Democratic Party, after the finance ministry outlined the plan in December when the won slid toward crisis-era levels. They were further stalled by political wrangling over tax fairness and broader legislative disputes.

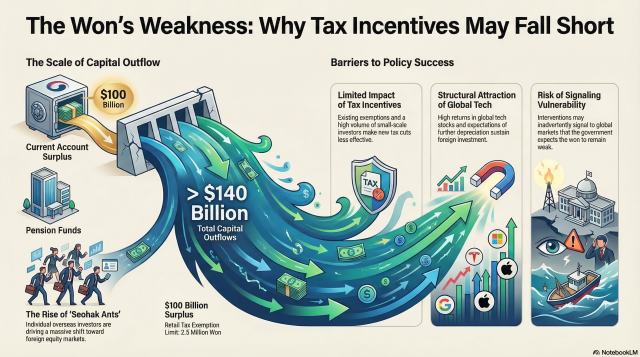

The centerpiece of the package is an amendment to the Restriction of Special Taxation Act that would grant a 50 to 100 percent deduction on capital gains taxes for investments in domestic stocks made through Return to Korea Investment Accounts, or RIAs. The aim is to encourage capital repatriation and stem the outflow of won-denominated funds.

The package also includes income deductions for investments in currency-hedging products and raises the exclusion rate for dividends received from overseas subsidiaries to as much as 100 percent. Lawmakers say the measures are designed to attract foreign currency holdings back onshore while promoting financial products that cushion exchange-rate volatility.

Given the won’s weakening trend, economists remain skeptical about the effectiveness of the incentives.

“Capital outflows from the National Pension Service and individual overseas investors exceeded $140 billion last year, surpassing the current account surplus of around $100 billion,” said Lee Seung-ho, a senior research fellow at the Korea Capital Market Institute.

While acknowledging the need to attract capital back into domestic markets, he questioned whether the tax breaks would be sufficient to alter investor behavior.

He noted that overseas equity investments already benefit from an annual tax exemption of up to 2.5 million won and that many retail investors operate on a relatively small scale, limiting the likely policy impact.

Other KCMI researchers, including Kim Min-ki and Kang So-hyun, argue that the shift toward foreign assets reflects deeper fundamentals: stronger returns in global technology stocks, lower barriers to overseas investing and persistent expectations of further won depreciation. Until those conditions change, they say, the outflow trend is unlikely to reverse.

Some in the market also warn that the legislation could send an unintended signal.

“Currency-related tax support can itself be read by the market as a signal that the authorities expect the won to remain weak,” a foreign-exchange market source said on condition of anonymity. “If it is seen as defensive rather than confidence-building, it could have the opposite effect.”

Copyright ⓒ Aju Press All rights reserved.