Bank of Korea: Stock Wealth Effect Lags Advanced Economies, Could Grow as KOSPI Hits 7,000

by Jang SunaPosted : May 7, 2026, 12:03Updated : May 7, 2026, 12:03

Share

facebook

twitter

URL

Text size

A sign marking KOSPI 7,000 is posted on the exterior wall of the Korea Exchange's Seoul office in Yeouido, Seoul, after the benchmark closed above 7,000 for the first time on May 6. [Photo=Yonhap]

South Korea’s stock market generates a much smaller “wealth effect” on household spending than major advanced economies, the Bank of Korea said, though the impact could grow as the KOSPI enters the 7,000 era and stock ownership broadens.

In a report released Wednesday titled “BOK Issue Note: An Assessment of Korea’s Stock Wealth Effect,” the central bank estimated that when rising share prices increase household wealth, consumption rises by about 1.3% of capital gains.

That implies that a 10,000-won increase in stock prices translates into roughly 130 won available for consumption. In the United States and Europe, about 3% to 4% of capital gains typically feeds into consumption, the report said.

The BOK attributed the gap largely to structural factors, including a relatively narrow investor base. As of 2024, stock assets equaled 77% of disposable income, far below the U.S. level of 256% and 184% in major European countries. Stock holdings are also concentrated among high-income, high-asset households, which tend to have a lower propensity to consume, limiting spillover to spending.

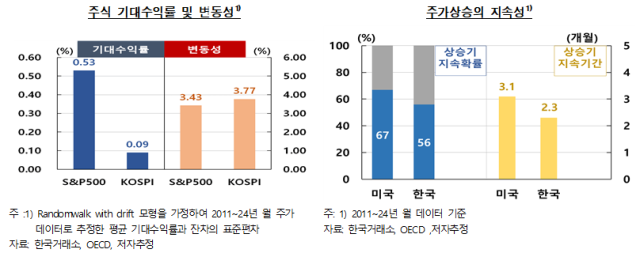

Market performance has also weighed on the effect. From 2011 to 2024, the S&P 500’s average expected monthly return was 0.53%, compared with 0.09% for the KOSPI, while volatility was 3.43% for the S&P 500 versus 3.77% for the KOSPI, about 10% higher. The probability that gains persist was 67% in the U.S. and 56% in South Korea, and the average duration of gains was 3.1 months in the U.S. versus 2.3 months in South Korea.

Investment behavior also constrains consumption, the report said, as stock profits tend to flow first into real estate rather than spending. For households without a home, about 70% of stock capital gains are estimated to move into property. Kim Min-su, deputy head of the BOK’s macro analysis team, said capital gains have tended to shift into real estate because in the past the property market had lower volatility and higher returns, raising the opportunity cost of consumption.

[Table=Bank of Korea]

Still, the BOK said the wealth effect could strengthen as share prices rise rapidly on factors including expanding global demand for artificial intelligence, increasing household stock holdings and drawing more young and middle- and lower-income investors into the market.

Household stock capital gains totaled 429 trillion won last year, about 22 times the average for 2011-2024, the report said. Because new investors tend to show a relatively larger wealth effect, the BOK said the gains could translate into stronger consumption.

The central bank also warned that a sharp market correction could produce a larger negative wealth effect. With leveraged investing such as margin loans increasing, a drop in asset prices alongside heavier debt burdens could add to downside pressure on the economy, it said.

Kim said it is important over the medium to long term to create a stable investment environment so the stock market can serve as a foundation for household wealth formation. He said policy efforts should curb the concentration of stock gains into real estate and strengthen incentives for long-term stock holding so that companies’ economic performance can translate into household asset accumulation and greater capacity to spend.