Journalist

Kwon,sung jin

mark1312@ajunews.com

-

Korea Racing Authority Discusses Relocation of Headquarters and LetsRun Park In line with the government's second phase of public institution relocations, the Korea Racing Authority (KRA) is undergoing organizational restructuring, intensifying discussions about relocating its headquarters and LetsRun Park. However, the selection of a new site, funding, and regional conflicts present significant challenges that may delay the actual move. According to the public institution management information disclosure system, Alio, KRA's board of directors approved the establishment of a new "Future Strategy Headquarters" on April 30. This headquarters, which will consist of about 100 personnel, is set to launch on May 13 and will handle key functions including planning, coordination, budgeting, performance management, and overseeing the relocation of the headquarters and LetsRun Park. Alongside the organizational changes, KRA is also expanding its regional offices. The existing Busan-Gyeongnam Regional Headquarters will be restructured into the Yeongnam Regional Headquarters, with plans to increase staffing by about 40 personnel. This move is in preparation for the upcoming opening of the Yeongcheon Racecourse later this year. The head of the regional headquarters will be a senior-level employee. This restructuring is seen as a response to increasing pressure to relocate LetsRun Park, particularly in light of the government's housing supply policies in Gwacheon. The site of LetsRun Park in Gwacheon has been frequently mentioned as a potential location for new housing developments due to its prime location in the metropolitan area. Consequently, there are growing concerns within KRA about the lack of viable alternatives to relocation. A KRA official stated, "While the government emphasizes the need to relocate LetsRun Park, there has been insufficient discussion regarding the constraints of the horse racing industry and operational realities. We plan to explore necessary support and realistic alternatives through the Future Strategy Headquarters during the relocation process." Currently, the most discussed scenario involves separating the relocation of the headquarters and LetsRun Park. The headquarters may move to a regional area such as Yeongcheon or Jeju, while LetsRun Park could relocate to another area within Gyeonggi Province, considering accessibility to the metropolitan area. However, industry consensus suggests that separating the two locations poses challenges due to the need for large spectator turnout and transportation accessibility. In this context, competition among local governments to attract the horse racing venue is intensifying. In some southern Gyeonggi areas like Siheung and Ansan, local election candidates are pledging to attract a racetrack, while in Uijeongbu, proposals have emerged to locate LetsRun Park at Camp Stanley, a former U.S. military base. The active involvement of local governments is driven by the substantial tax revenue potential. In 2023, LetsRun Park contributed approximately 315.7 billion won in leisure taxes and 126.3 billion won in local allocation taxes to Gyeonggi Province. Notably, under current local finance laws, a portion of the leisure tax is distributed to municipalities where racetracks and off-track betting locations are situated, making successful relocation a pathway to stable local financial resources. There is a growing sentiment within and outside KRA that Siheung City is a realistic candidate for relocation. Its excellent accessibility from the southwestern metropolitan area and the potential for securing a large site are key factors. One industry insider noted, "The northern Gyeonggi area faces significant risks for race operations due to winter cold snaps and ground freezing issues. Considering accessibility and climate conditions, the southern Gyeonggi area is more practical, with Siheung appearing to be the most promising option." * This article has been translated by AI. 2026-05-12 04:20:54

Korea Racing Authority Discusses Relocation of Headquarters and LetsRun Park In line with the government's second phase of public institution relocations, the Korea Racing Authority (KRA) is undergoing organizational restructuring, intensifying discussions about relocating its headquarters and LetsRun Park. However, the selection of a new site, funding, and regional conflicts present significant challenges that may delay the actual move. According to the public institution management information disclosure system, Alio, KRA's board of directors approved the establishment of a new "Future Strategy Headquarters" on April 30. This headquarters, which will consist of about 100 personnel, is set to launch on May 13 and will handle key functions including planning, coordination, budgeting, performance management, and overseeing the relocation of the headquarters and LetsRun Park. Alongside the organizational changes, KRA is also expanding its regional offices. The existing Busan-Gyeongnam Regional Headquarters will be restructured into the Yeongnam Regional Headquarters, with plans to increase staffing by about 40 personnel. This move is in preparation for the upcoming opening of the Yeongcheon Racecourse later this year. The head of the regional headquarters will be a senior-level employee. This restructuring is seen as a response to increasing pressure to relocate LetsRun Park, particularly in light of the government's housing supply policies in Gwacheon. The site of LetsRun Park in Gwacheon has been frequently mentioned as a potential location for new housing developments due to its prime location in the metropolitan area. Consequently, there are growing concerns within KRA about the lack of viable alternatives to relocation. A KRA official stated, "While the government emphasizes the need to relocate LetsRun Park, there has been insufficient discussion regarding the constraints of the horse racing industry and operational realities. We plan to explore necessary support and realistic alternatives through the Future Strategy Headquarters during the relocation process." Currently, the most discussed scenario involves separating the relocation of the headquarters and LetsRun Park. The headquarters may move to a regional area such as Yeongcheon or Jeju, while LetsRun Park could relocate to another area within Gyeonggi Province, considering accessibility to the metropolitan area. However, industry consensus suggests that separating the two locations poses challenges due to the need for large spectator turnout and transportation accessibility. In this context, competition among local governments to attract the horse racing venue is intensifying. In some southern Gyeonggi areas like Siheung and Ansan, local election candidates are pledging to attract a racetrack, while in Uijeongbu, proposals have emerged to locate LetsRun Park at Camp Stanley, a former U.S. military base. The active involvement of local governments is driven by the substantial tax revenue potential. In 2023, LetsRun Park contributed approximately 315.7 billion won in leisure taxes and 126.3 billion won in local allocation taxes to Gyeonggi Province. Notably, under current local finance laws, a portion of the leisure tax is distributed to municipalities where racetracks and off-track betting locations are situated, making successful relocation a pathway to stable local financial resources. There is a growing sentiment within and outside KRA that Siheung City is a realistic candidate for relocation. Its excellent accessibility from the southwestern metropolitan area and the potential for securing a large site are key factors. One industry insider noted, "The northern Gyeonggi area faces significant risks for race operations due to winter cold snaps and ground freezing issues. Considering accessibility and climate conditions, the southern Gyeonggi area is more practical, with Siheung appearing to be the most promising option." * This article has been translated by AI. 2026-05-12 04:20:54 -

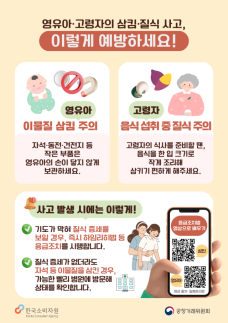

Increase in Choking Incidents Among Infants and Seniors Prompts Consumer Safety Alert As incidents of choking due to foreign object ingestion among infants and seniors continue to rise, the government has issued a consumer safety alert.On May 11, the Fair Trade Commission reported that last year, the Korea Consumer Agency's Consumer Hazard Monitoring System (CISS) recorded 809 cases of foreign object ingestion. Over the past five years, the trend has shown fluctuations: 728 cases in 2021, 949 in 2022, 972 in 2023, and a temporary decrease to 655 in 2024, followed by a rise again last year.Among the foreign object ingestion incidents in the last five years, 67.6% involved children aged seven and under. Specifically, the highest number of incidents occurred with one-year-olds (25.2%), and more than half (56.3%) of the cases involved infants under two years old, who are more likely to put objects in their mouths.The primary hazardous items ingested by infants included magnets (13.8%, 384 cases), toys (10.0%, 279 cases), and coins (9.6%, 266 cases). Other causes of incidents included marbles, stickers, and batteries. The Fair Trade Commission has urged caution, noting that foreign objects can lead to severe injuries such as intestinal perforation or airway obstruction.In contrast, seniors aged 65 and older are at greater risk of choking incidents due to diminished physical abilities, such as reduced coughing reflexes associated with aging. Many choking incidents among seniors have occurred while consuming foods like rice cakes, sweet potatoes, and tangerines. According to the Fire Agency, a total of 1,196 patients were transported due to airway obstruction from food consumption over the past five years.The Fair Trade Commission emphasized that while infant choking incidents often arise from curiosity during play, choking incidents among seniors frequently occur during meals, highlighting the importance of adjusting food sizes.To prevent choking incidents among infants and seniors, the Fair Trade Commission and the Korea Consumer Agency recommend: keeping small items like magnets and coins out of reach of infants; preparing food for seniors in bite-sized pieces and encouraging slow chewing; and immediately performing emergency measures such as the Heimlich maneuver if choking symptoms occur.* This article has been translated by AI. 2026-05-11 12:10:31

Increase in Choking Incidents Among Infants and Seniors Prompts Consumer Safety Alert As incidents of choking due to foreign object ingestion among infants and seniors continue to rise, the government has issued a consumer safety alert.On May 11, the Fair Trade Commission reported that last year, the Korea Consumer Agency's Consumer Hazard Monitoring System (CISS) recorded 809 cases of foreign object ingestion. Over the past five years, the trend has shown fluctuations: 728 cases in 2021, 949 in 2022, 972 in 2023, and a temporary decrease to 655 in 2024, followed by a rise again last year.Among the foreign object ingestion incidents in the last five years, 67.6% involved children aged seven and under. Specifically, the highest number of incidents occurred with one-year-olds (25.2%), and more than half (56.3%) of the cases involved infants under two years old, who are more likely to put objects in their mouths.The primary hazardous items ingested by infants included magnets (13.8%, 384 cases), toys (10.0%, 279 cases), and coins (9.6%, 266 cases). Other causes of incidents included marbles, stickers, and batteries. The Fair Trade Commission has urged caution, noting that foreign objects can lead to severe injuries such as intestinal perforation or airway obstruction.In contrast, seniors aged 65 and older are at greater risk of choking incidents due to diminished physical abilities, such as reduced coughing reflexes associated with aging. Many choking incidents among seniors have occurred while consuming foods like rice cakes, sweet potatoes, and tangerines. According to the Fire Agency, a total of 1,196 patients were transported due to airway obstruction from food consumption over the past five years.The Fair Trade Commission emphasized that while infant choking incidents often arise from curiosity during play, choking incidents among seniors frequently occur during meals, highlighting the importance of adjusting food sizes.To prevent choking incidents among infants and seniors, the Fair Trade Commission and the Korea Consumer Agency recommend: keeping small items like magnets and coins out of reach of infants; preparing food for seniors in bite-sized pieces and encouraging slow chewing; and immediately performing emergency measures such as the Heimlich maneuver if choking symptoms occur.* This article has been translated by AI. 2026-05-11 12:10:31 -

Rising Grain Prices Due to Middle East Conflict May Impact Livestock Costs International grain prices are rising due to the blockade of the Strait of Hormuz amid the conflict between the U.S. and Iran. This increase is expected to drive up domestic feed prices, raising concerns that livestock prices may follow suit. Additionally, the prices of cooking oils and other fats are also climbing, making dining out less affordable. According to relevant authorities on May 10, the United Nations Food and Agriculture Organization (FAO) reported that the global food price index rose by 1.6% last month, reaching 130.7. This index compares current prices to the average from 2014 to 2016, and after five consecutive months of decline until January, it has now increased for three straight months since rebounding in February. Specifically, the international grain price index led the increase, rising 0.8% to 111.3. Wheat prices were affected by drought in some regions of the U.S., contributing to a 0.8% increase in the wheat price index. The blockade of the Strait of Hormuz has also led to higher fertilizer prices, prompting farmers to reduce wheat cultivation, which further drives up prices. The corn price index rose 0.7% compared to the previous month due to supply shortages in Brazil and drought conditions in the U.S. The rice price index also increased by 1.9% over the month, influenced by soaring crude oil and petroleum derivative prices, which raised production and distribution costs. The rise in international grain prices is expected to exert pressure on domestic feed prices over time, as more than 95% of the grains used in feed for livestock farms are imported. Additionally, the won-dollar exchange rate has significantly increased compared to a year ago (averaging 1,394 won in May 2025), further raising import costs. The feed industry is also reaching its limits. A representative from the feed sector stated, "With the exchange rate rising and shipping costs increasing due to the Middle East conflict, grain prices are also climbing. While we are trying to hold off on price increases due to demands from the agricultural sector, we cannot allow losses to accumulate indefinitely, so we are considering various alternatives." When feed prices rise, livestock prices are also affected, as feed costs constitute a significant portion of production expenses. It is reported that about 40% of the production costs for Hanwoo, a popular breed among farmers, are attributed to feed. Currently, both domestic farmers and the feed industry anticipate a high likelihood of price increases in the second half of the year. As a result, concerns are growing that already soaring livestock prices may become even more unstable. According to the Korea Institute of Animal Products Quality Evaluation, the price of grade 1 beef sirloin was 9,980 won per 100 grams, an 11.1% increase compared to a year ago. The price of pork belly also rose to 2,742 won per 100 grams, up 9.6% from the previous year. With the added pressure of rising feed costs, there is a strong possibility that this upward price trend will continue. Imported beef prices are also rising, putting pressure on consumer prices. As of the previous day, the price of U.S. beef short ribs (chilled) and chuck eye roll (chilled) was 4,724 won and 4,123 won per 100 grams, respectively, marking increases of 13.7% and 18.0% compared to a year ago. The prices of cooking oils and other fats, which impact overall dining costs, are also concerning. According to the FAO, the price index for oils and fats rose by 5.9% last month, reaching 193.9. The international palm oil price, a key ingredient for cooking oil, has continued to rise for five consecutive months due to increased demand for biofuels. A representative from the Ministry of Agriculture, Food and Rural Affairs stated, "Given the ongoing uncertainties in international raw material prices, we will strengthen monitoring of supply and demand conditions for various items and will make every effort to manage the supply of agricultural and livestock products using available means." * This article has been translated by AI. 2026-05-11 05:05:22

Rising Grain Prices Due to Middle East Conflict May Impact Livestock Costs International grain prices are rising due to the blockade of the Strait of Hormuz amid the conflict between the U.S. and Iran. This increase is expected to drive up domestic feed prices, raising concerns that livestock prices may follow suit. Additionally, the prices of cooking oils and other fats are also climbing, making dining out less affordable. According to relevant authorities on May 10, the United Nations Food and Agriculture Organization (FAO) reported that the global food price index rose by 1.6% last month, reaching 130.7. This index compares current prices to the average from 2014 to 2016, and after five consecutive months of decline until January, it has now increased for three straight months since rebounding in February. Specifically, the international grain price index led the increase, rising 0.8% to 111.3. Wheat prices were affected by drought in some regions of the U.S., contributing to a 0.8% increase in the wheat price index. The blockade of the Strait of Hormuz has also led to higher fertilizer prices, prompting farmers to reduce wheat cultivation, which further drives up prices. The corn price index rose 0.7% compared to the previous month due to supply shortages in Brazil and drought conditions in the U.S. The rice price index also increased by 1.9% over the month, influenced by soaring crude oil and petroleum derivative prices, which raised production and distribution costs. The rise in international grain prices is expected to exert pressure on domestic feed prices over time, as more than 95% of the grains used in feed for livestock farms are imported. Additionally, the won-dollar exchange rate has significantly increased compared to a year ago (averaging 1,394 won in May 2025), further raising import costs. The feed industry is also reaching its limits. A representative from the feed sector stated, "With the exchange rate rising and shipping costs increasing due to the Middle East conflict, grain prices are also climbing. While we are trying to hold off on price increases due to demands from the agricultural sector, we cannot allow losses to accumulate indefinitely, so we are considering various alternatives." When feed prices rise, livestock prices are also affected, as feed costs constitute a significant portion of production expenses. It is reported that about 40% of the production costs for Hanwoo, a popular breed among farmers, are attributed to feed. Currently, both domestic farmers and the feed industry anticipate a high likelihood of price increases in the second half of the year. As a result, concerns are growing that already soaring livestock prices may become even more unstable. According to the Korea Institute of Animal Products Quality Evaluation, the price of grade 1 beef sirloin was 9,980 won per 100 grams, an 11.1% increase compared to a year ago. The price of pork belly also rose to 2,742 won per 100 grams, up 9.6% from the previous year. With the added pressure of rising feed costs, there is a strong possibility that this upward price trend will continue. Imported beef prices are also rising, putting pressure on consumer prices. As of the previous day, the price of U.S. beef short ribs (chilled) and chuck eye roll (chilled) was 4,724 won and 4,123 won per 100 grams, respectively, marking increases of 13.7% and 18.0% compared to a year ago. The prices of cooking oils and other fats, which impact overall dining costs, are also concerning. According to the FAO, the price index for oils and fats rose by 5.9% last month, reaching 193.9. The international palm oil price, a key ingredient for cooking oil, has continued to rise for five consecutive months due to increased demand for biofuels. A representative from the Ministry of Agriculture, Food and Rural Affairs stated, "Given the ongoing uncertainties in international raw material prices, we will strengthen monitoring of supply and demand conditions for various items and will make every effort to manage the supply of agricultural and livestock products using available means." * This article has been translated by AI. 2026-05-11 05:05:22 -

Korea's Fair Trade Commission Investigates Myungnyun Jinsagalbi for Loan Practices The Fair Trade Commission (FTC) has initiated disciplinary proceedings against Myungnyun Jinsagalbi's franchise headquarters, Myungnyun-dang, over allegations of high-interest lending and coercive practices towards franchisees. The investigation stems from claims that the company effectively forced franchise owners to use specific suppliers and omitted critical loan-related information. On May 10, the FTC's secretariat announced that it had sent a review report detailing the alleged violations of the Franchise Business Fairness Act to the accused party on May 8, which included findings on the actions, legality, and recommendations for corrective measures. Myungnyun-dang has been under investigation by the FTC since September 2025, following allegations that it provided high-interest loans to franchise owners through a lending company it established after securing low-interest loans from the Industrial Bank of Korea. According to the FTC, Myungnyun-dang allegedly offered loans for franchise setup without adequately considering the financial situations of franchisees. Notably, franchise owners were reportedly burdened with costs for interior construction and equipment that exceeded actual payments. Evidence also suggests that Myungnyun-dang coerced franchisees into using specific suppliers for necessary services, including interior construction and equipment installation. Furthermore, despite providing credit or facilitating loans for franchisees, Myungnyun-dang inaccurately reported 'no relevant information' in the disclosure documents regarding credit provision and facilitation, which are mandatory disclosures. The examiner classified Myungnyun-dang's actions as providing unfair disadvantages, restricting trading partners, and offering false and misleading information. Recommendations for corrective orders, fines, and prosecution have been proposed. An FTC official stated, "We are ensuring that the accused party has ample opportunity to defend itself by allowing the submission of written opinions and requests for evidence review and copying. The committee will make a final decision after deliberation."* This article has been translated by AI. 2026-05-10 12:10:29

Korea's Fair Trade Commission Investigates Myungnyun Jinsagalbi for Loan Practices The Fair Trade Commission (FTC) has initiated disciplinary proceedings against Myungnyun Jinsagalbi's franchise headquarters, Myungnyun-dang, over allegations of high-interest lending and coercive practices towards franchisees. The investigation stems from claims that the company effectively forced franchise owners to use specific suppliers and omitted critical loan-related information. On May 10, the FTC's secretariat announced that it had sent a review report detailing the alleged violations of the Franchise Business Fairness Act to the accused party on May 8, which included findings on the actions, legality, and recommendations for corrective measures. Myungnyun-dang has been under investigation by the FTC since September 2025, following allegations that it provided high-interest loans to franchise owners through a lending company it established after securing low-interest loans from the Industrial Bank of Korea. According to the FTC, Myungnyun-dang allegedly offered loans for franchise setup without adequately considering the financial situations of franchisees. Notably, franchise owners were reportedly burdened with costs for interior construction and equipment that exceeded actual payments. Evidence also suggests that Myungnyun-dang coerced franchisees into using specific suppliers for necessary services, including interior construction and equipment installation. Furthermore, despite providing credit or facilitating loans for franchisees, Myungnyun-dang inaccurately reported 'no relevant information' in the disclosure documents regarding credit provision and facilitation, which are mandatory disclosures. The examiner classified Myungnyun-dang's actions as providing unfair disadvantages, restricting trading partners, and offering false and misleading information. Recommendations for corrective orders, fines, and prosecution have been proposed. An FTC official stated, "We are ensuring that the accused party has ample opportunity to defend itself by allowing the submission of written opinions and requests for evidence review and copying. The committee will make a final decision after deliberation."* This article has been translated by AI. 2026-05-10 12:10:29 -

Rural Basic Income Pilot Program Sees High Demand with 8.8 to 1 Competition Ratio Interest in the rural basic income pilot program is heating up, with 44 counties applying for five additional slots, resulting in a competition ratio exceeding 8 to 1. The government plans to finalize the selection of additional regions next month.On May 10, the Ministry of Agriculture, Food and Rural Affairs announced that 44 counties had applied for the expanded pilot program aimed at providing basic income in rural areas.The rural basic income pilot program aims to combat the crisis of rural depopulation by providing monthly payments of 150,000 won in local love gift certificates to stimulate local consumption.To mitigate the impact of high inflation due to geopolitical risks in the Middle East and to strengthen support for vulnerable rural areas, the ministry secured additional budget funding last month. As a result, a call for applications was made to select five more counties from 59 designated areas experiencing population decline. The response was robust, with 44 counties expressing interest, leading to a competition ratio of 8.8 to 1.Specifically, the applicants include one county from Gyeonggi, eight from Gangwon, four from Chungbuk, four from Chungnam, five from Jeonbuk, eleven from Jeonnam, five from Gyeongbuk, and six from Gyeongnam, totaling 44 counties.The ministry will form an evaluation committee composed of private experts in rural policy, basic income, balanced development, and local finance, and plans to announce the selection of the five additional counties next month.Kang Dong-yoon, director of the Rural Income and Energy Policy Division at the Ministry of Agriculture, Food and Rural Affairs, stated, "We will actively support the rural basic income pilot program to ensure it takes root in the selected areas and leads to tangible results."* This article has been translated by AI. 2026-05-10 11:28:57

Rural Basic Income Pilot Program Sees High Demand with 8.8 to 1 Competition Ratio Interest in the rural basic income pilot program is heating up, with 44 counties applying for five additional slots, resulting in a competition ratio exceeding 8 to 1. The government plans to finalize the selection of additional regions next month.On May 10, the Ministry of Agriculture, Food and Rural Affairs announced that 44 counties had applied for the expanded pilot program aimed at providing basic income in rural areas.The rural basic income pilot program aims to combat the crisis of rural depopulation by providing monthly payments of 150,000 won in local love gift certificates to stimulate local consumption.To mitigate the impact of high inflation due to geopolitical risks in the Middle East and to strengthen support for vulnerable rural areas, the ministry secured additional budget funding last month. As a result, a call for applications was made to select five more counties from 59 designated areas experiencing population decline. The response was robust, with 44 counties expressing interest, leading to a competition ratio of 8.8 to 1.Specifically, the applicants include one county from Gyeonggi, eight from Gangwon, four from Chungbuk, four from Chungnam, five from Jeonbuk, eleven from Jeonnam, five from Gyeongbuk, and six from Gyeongnam, totaling 44 counties.The ministry will form an evaluation committee composed of private experts in rural policy, basic income, balanced development, and local finance, and plans to announce the selection of the five additional counties next month.Kang Dong-yoon, director of the Rural Income and Energy Policy Division at the Ministry of Agriculture, Food and Rural Affairs, stated, "We will actively support the rural basic income pilot program to ensure it takes root in the selected areas and leads to tangible results."* This article has been translated by AI. 2026-05-10 11:28:57 -

New Agricultural Land Law Mandates Leasing for Non-Operating Owners Owners of inherited or abandoned farmland must now lease their land to the Korea Rural Community Corporation under a new agricultural land law that has passed the National Assembly. Additionally, local governments are required to issue disposal orders for any violations of the Agricultural Land Law. According to the Ministry of Agriculture, Food and Rural Affairs, the revised law aims to support comprehensive land surveys and promote efficient land use. The amendment eliminates the maximum size limit (10,000 square meters) for farmland owned by non-farmers, preventing further fragmentation of agricultural land. It mandates that such land be leased to the Korea Rural Community Corporation. The law also expands the permissible uses of agricultural land to include 'agricultural and rural experience facilities' and 'agricultural solar power installations.' Furthermore, the use of amenities like bathhouses and cold shelters in agricultural promotion areas is now allowed for both farmers and rural residents. Enforcement of the law will be stricter, with local governments now required to issue disposal orders for violations, a shift from previous discretionary authority. The law also prevents landowners from evading regulations by selling to close relatives or corporations they represent. If local governments fail to manage compliance, the Minister of Agriculture, Food and Rural Affairs will have the authority to issue disposal orders directly. The revised law will be implemented gradually following approval from the Cabinet. Yoon Won-seop, the agricultural policy director at the ministry, stated, "With the passage of this law, we are prepared for thorough land surveys to ensure that farmland is preserved as a means of production for farmers, not as a target for speculation."* This article has been translated by AI. 2026-05-07 23:30:53

New Agricultural Land Law Mandates Leasing for Non-Operating Owners Owners of inherited or abandoned farmland must now lease their land to the Korea Rural Community Corporation under a new agricultural land law that has passed the National Assembly. Additionally, local governments are required to issue disposal orders for any violations of the Agricultural Land Law. According to the Ministry of Agriculture, Food and Rural Affairs, the revised law aims to support comprehensive land surveys and promote efficient land use. The amendment eliminates the maximum size limit (10,000 square meters) for farmland owned by non-farmers, preventing further fragmentation of agricultural land. It mandates that such land be leased to the Korea Rural Community Corporation. The law also expands the permissible uses of agricultural land to include 'agricultural and rural experience facilities' and 'agricultural solar power installations.' Furthermore, the use of amenities like bathhouses and cold shelters in agricultural promotion areas is now allowed for both farmers and rural residents. Enforcement of the law will be stricter, with local governments now required to issue disposal orders for violations, a shift from previous discretionary authority. The law also prevents landowners from evading regulations by selling to close relatives or corporations they represent. If local governments fail to manage compliance, the Minister of Agriculture, Food and Rural Affairs will have the authority to issue disposal orders directly. The revised law will be implemented gradually following approval from the Cabinet. Yoon Won-seop, the agricultural policy director at the ministry, stated, "With the passage of this law, we are prepared for thorough land surveys to ensure that farmland is preserved as a means of production for farmers, not as a target for speculation."* This article has been translated by AI. 2026-05-07 23:30:53 -

Government Seeks Farmer Input on Agricultural Cooperative Reforms The government, which is pushing for reforms in agricultural cooperatives, gathered feedback from farmers on May 7. Officials expressed intentions to address concerns about election fervor and rising costs.According to the Ministry of Agriculture, Food and Rural Affairs, Vice Minister Kim Jong-gu held a meeting with agricultural organization leaders at the aT Center in Seoul. He discussed the reform plans announced during government discussions on March 11 and April 1.Attendees included over 30 representatives from various agricultural organizations, such as Lee Seung-ho, president of the Korean Federation of Agricultural and Livestock Organizations, and Noh Man-ho, permanent representative of the Korean Comprehensive Agricultural Organizations Council.During the meeting, the ministry outlined key reform proposals, including the introduction of direct elections for members and the establishment of an Agricultural Cooperative Audit Committee. They also shared feedback gathered from previous meetings with cooperative leaders and regional briefings.Last month, the government held regional briefings in Daegu, Cheongju, and Suwon to collect opinions from cooperative leaders, members, agricultural organizations, and experts. Concerns raised included the potential for election fervor and politicization with direct elections, as well as worries about organizational expansion and financial burdens from the new audit committee.In response, Vice Minister Kim stated that they are considering alternatives such as strengthening the eligibility for candidates and introducing public elections, as well as simultaneous elections for the president and cooperative leaders. He also assured that they would explore cost-saving measures through organizational efficiency to address concerns about increased expenses from the independent audit committee.Kim emphasized, "This reform aims to improve the abnormal operational structure of agricultural cooperatives revealed in special audits and ultimately restore these organizations to serve their members and farmers. We will address the concerns raised in today's meeting during the legislative process."* This article has been translated by AI. 2026-05-07 22:14:45

Government Seeks Farmer Input on Agricultural Cooperative Reforms The government, which is pushing for reforms in agricultural cooperatives, gathered feedback from farmers on May 7. Officials expressed intentions to address concerns about election fervor and rising costs.According to the Ministry of Agriculture, Food and Rural Affairs, Vice Minister Kim Jong-gu held a meeting with agricultural organization leaders at the aT Center in Seoul. He discussed the reform plans announced during government discussions on March 11 and April 1.Attendees included over 30 representatives from various agricultural organizations, such as Lee Seung-ho, president of the Korean Federation of Agricultural and Livestock Organizations, and Noh Man-ho, permanent representative of the Korean Comprehensive Agricultural Organizations Council.During the meeting, the ministry outlined key reform proposals, including the introduction of direct elections for members and the establishment of an Agricultural Cooperative Audit Committee. They also shared feedback gathered from previous meetings with cooperative leaders and regional briefings.Last month, the government held regional briefings in Daegu, Cheongju, and Suwon to collect opinions from cooperative leaders, members, agricultural organizations, and experts. Concerns raised included the potential for election fervor and politicization with direct elections, as well as worries about organizational expansion and financial burdens from the new audit committee.In response, Vice Minister Kim stated that they are considering alternatives such as strengthening the eligibility for candidates and introducing public elections, as well as simultaneous elections for the president and cooperative leaders. He also assured that they would explore cost-saving measures through organizational efficiency to address concerns about increased expenses from the independent audit committee.Kim emphasized, "This reform aims to improve the abnormal operational structure of agricultural cooperatives revealed in special audits and ultimately restore these organizations to serve their members and farmers. We will address the concerns raised in today's meeting during the legislative process."* This article has been translated by AI. 2026-05-07 22:14:45 -

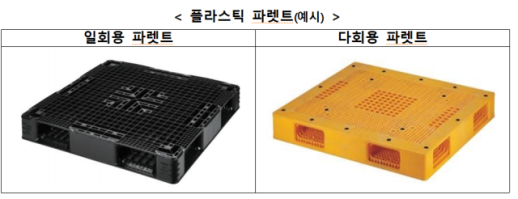

South Korea fines 18 plastic pallet firms 11.7 billion won for bid-rigging Eighteen manufacturers and sellers of plastic pallets that allegedly coordinated bid winners and prices have been fined by South Korea’s antitrust watchdog. The Fair Trade Commission said May 7 it will impose a combined 11.737 billion won ($11.7 billion won) in penalties and issue corrective orders against the 18 companies for avoiding competition and fixing prices. Pallets are platforms used in logistics to bundle and move multiple items as a single load. The companies took part in 165 bids run by 23 businesses and, through phone calls, in-person meetings and mobile messaging, agreed in advance on the expected winner, “cover” bidders and bid prices for each tender, the commission said. The cover bidders submitted bids at the agreed price level, and the designated winner shared part of the collusive profits with other firms. In particular, five of the firms also agreed on which company would supply pallets in transactions with NongHyup Economic Holdings and then split the profits, the commission said. When local NongHyup cooperatives asked to buy pallets, four other firms quoted prices higher than the NongHyup supply price to steer purchases through Economic Holdings. The collusion lasted 6 years and 8 months and involved 369.2 billion won in related sales, the commission said. It said 23 companies, including Lotte Chemical, DL Chemical and Seoul Milk Cooperative, were harmed. An FTC official said the agency will respond strictly to cartels that impose unnecessary costs on businesses and weaken industrial competitiveness. * This article has been translated by AI. 2026-05-07 12:04:39

South Korea fines 18 plastic pallet firms 11.7 billion won for bid-rigging Eighteen manufacturers and sellers of plastic pallets that allegedly coordinated bid winners and prices have been fined by South Korea’s antitrust watchdog. The Fair Trade Commission said May 7 it will impose a combined 11.737 billion won ($11.7 billion won) in penalties and issue corrective orders against the 18 companies for avoiding competition and fixing prices. Pallets are platforms used in logistics to bundle and move multiple items as a single load. The companies took part in 165 bids run by 23 businesses and, through phone calls, in-person meetings and mobile messaging, agreed in advance on the expected winner, “cover” bidders and bid prices for each tender, the commission said. The cover bidders submitted bids at the agreed price level, and the designated winner shared part of the collusive profits with other firms. In particular, five of the firms also agreed on which company would supply pallets in transactions with NongHyup Economic Holdings and then split the profits, the commission said. When local NongHyup cooperatives asked to buy pallets, four other firms quoted prices higher than the NongHyup supply price to steer purchases through Economic Holdings. The collusion lasted 6 years and 8 months and involved 369.2 billion won in related sales, the commission said. It said 23 companies, including Lotte Chemical, DL Chemical and Seoul Milk Cooperative, were harmed. An FTC official said the agency will respond strictly to cartels that impose unnecessary costs on businesses and weaken industrial competitiveness. * This article has been translated by AI. 2026-05-07 12:04:39 -

Korea Fair Trade Commission to Brief Big Conglomerates on Disclosure Rules South Korea’s antitrust regulator will hold tailored briefings online and in person for disclosure officers at major conglomerates, aiming to prevent repeat violations. The Korea Fair Trade Commission said May 7 it will host the sessions with the Korea Chamber of Commerce and Industry from May 11 to 13 for companies designated as disclosure-target business groups, commonly known as large conglomerates. The commission holds quarterly briefings each year to improve understanding of disclosure requirements and curb recurring violations. Groups that breach the disclosure system can face corrective orders and administrative fines of up to 100 million won. Last month, the commission newly designated 11 groups as large conglomerates: Line, the Korea Teachers’ Credit Union, Woongjin, Shielders, Daemyung Chemical, Toss, Kolmar Korea, Heesung, Orion, QCP Group and Iljin Global. Including the newly designated groups, the total number of large conglomerates in South Korea is 102. At the briefings, the commission will also explain obligations related to status disclosures, disclosures of large internal transactions, and disclosures of key matters for unlisted companies, reflecting cases in which the controlling person of some groups has changed to a natural person. It will provide additional guidance tied to this year’s group designations and set aside time for questions and answers, offering company-specific assistance. The commission said it will continue outreach online. In the first half of the year, it plans to produce explanatory videos on large internal transactions, key matters for unlisted companies and group status disclosures, and release them on its official YouTube channel. In the second half, it plans to hold “on-site disclosure briefings” for conglomerates based outside the capital region. * This article has been translated by AI. 2026-05-07 10:03:21

Korea Fair Trade Commission to Brief Big Conglomerates on Disclosure Rules South Korea’s antitrust regulator will hold tailored briefings online and in person for disclosure officers at major conglomerates, aiming to prevent repeat violations. The Korea Fair Trade Commission said May 7 it will host the sessions with the Korea Chamber of Commerce and Industry from May 11 to 13 for companies designated as disclosure-target business groups, commonly known as large conglomerates. The commission holds quarterly briefings each year to improve understanding of disclosure requirements and curb recurring violations. Groups that breach the disclosure system can face corrective orders and administrative fines of up to 100 million won. Last month, the commission newly designated 11 groups as large conglomerates: Line, the Korea Teachers’ Credit Union, Woongjin, Shielders, Daemyung Chemical, Toss, Kolmar Korea, Heesung, Orion, QCP Group and Iljin Global. Including the newly designated groups, the total number of large conglomerates in South Korea is 102. At the briefings, the commission will also explain obligations related to status disclosures, disclosures of large internal transactions, and disclosures of key matters for unlisted companies, reflecting cases in which the controlling person of some groups has changed to a natural person. It will provide additional guidance tied to this year’s group designations and set aside time for questions and answers, offering company-specific assistance. The commission said it will continue outreach online. In the first half of the year, it plans to produce explanatory videos on large internal transactions, key matters for unlisted companies and group status disclosures, and release them on its official YouTube channel. In the second half, it plans to hold “on-site disclosure briefings” for conglomerates based outside the capital region. * This article has been translated by AI. 2026-05-07 10:03:21 -

Calls Grow for NH Reform: Direct Election, Permanent Oversight Body Urged As the government moves ahead with a broad overhaul of NongHyup, calls are growing from academics, cooperative members and the public to move faster. Critics say repeated misconduct involving the chair of the National Agricultural Cooperative Federation reflects structural problems and requires changes such as direct elections by members and a permanent oversight body. According to relevant ministries on Tuesday, the National Assembly’s Agriculture, Food, Rural Affairs, Oceans and Fisheries Committee will hold a legislative hearing May 12 on revisions to the Agricultural Cooperatives Act. The hearing is expected to focus on an amendment proposed by Democratic Party lawmaker Yoon Jun-byeong that emerged from a ruling party-government consultation on April 1. The bill calls for introducing direct elections for the federation chair by cooperative members and creating an external audit body. The push follows repeated allegations of lax management and misconduct at the federation. A joint government audit announced in March found widespread problems, including corruption and abuses of power by key executives, preferential loans and contracts, and loose budget spending. The government referred 14 cases for investigation. A recent survey commissioned by the Korea Rural Economic Institute from Gallup Korea found strong support for reform: 94.5% of cooperative members and 95.1% of the general public said they favor changes. Many cited the need to address wrongdoing by executives and employees as the main reason, including 55.1% of members and 73% of the public. Experts have also argued for stronger checks on the federation. In a recent report titled “NongHyup Reform: Creative Destruction and Innovation,” KREI researcher Kim Tae-hoo said existing cooperative committees and audit committees have limits in ensuring independence because the federation chair can exert influence. He said that is why reforms are needed, including requiring the appointment of outside experts as compliance officers, mandating reporting of crimes by executives and employees, and creating a legal basis to suspend officials from duty upon conviction. Some cooperative heads, however, have raised concerns about direct elections and making audit bodies permanent. They argue direct elections could turn NongHyup into a political organization and weaken professionalism. Others say constant oversight runs counter to the cooperative principle of autonomy. Ha Seung-soo, a lawyer with the NongHyup Reform Promotion Group, rejected that argument. “It is true that cooperatives should be guaranteed autonomy, but autonomy at a level that enables corruption cannot be accepted,” he said. He said the current indirect election system, in which only cooperative heads vote, has produced behavior close to “dividing up positions.” He added that breaking what he called an exclusive privilege through direct elections would make the organization healthier. The government said it will accelerate work on a second package of reforms. A government official said the first package aimed to prevent misconduct by the federation and its chair, while the second will focus on remaking NongHyup into an organization for farmers. The official said the government plans to announce the second package next month, drawing in part on Japan’s agricultural cooperative reforms. * This article has been translated by AI. 2026-05-07 06:04:10

Calls Grow for NH Reform: Direct Election, Permanent Oversight Body Urged As the government moves ahead with a broad overhaul of NongHyup, calls are growing from academics, cooperative members and the public to move faster. Critics say repeated misconduct involving the chair of the National Agricultural Cooperative Federation reflects structural problems and requires changes such as direct elections by members and a permanent oversight body. According to relevant ministries on Tuesday, the National Assembly’s Agriculture, Food, Rural Affairs, Oceans and Fisheries Committee will hold a legislative hearing May 12 on revisions to the Agricultural Cooperatives Act. The hearing is expected to focus on an amendment proposed by Democratic Party lawmaker Yoon Jun-byeong that emerged from a ruling party-government consultation on April 1. The bill calls for introducing direct elections for the federation chair by cooperative members and creating an external audit body. The push follows repeated allegations of lax management and misconduct at the federation. A joint government audit announced in March found widespread problems, including corruption and abuses of power by key executives, preferential loans and contracts, and loose budget spending. The government referred 14 cases for investigation. A recent survey commissioned by the Korea Rural Economic Institute from Gallup Korea found strong support for reform: 94.5% of cooperative members and 95.1% of the general public said they favor changes. Many cited the need to address wrongdoing by executives and employees as the main reason, including 55.1% of members and 73% of the public. Experts have also argued for stronger checks on the federation. In a recent report titled “NongHyup Reform: Creative Destruction and Innovation,” KREI researcher Kim Tae-hoo said existing cooperative committees and audit committees have limits in ensuring independence because the federation chair can exert influence. He said that is why reforms are needed, including requiring the appointment of outside experts as compliance officers, mandating reporting of crimes by executives and employees, and creating a legal basis to suspend officials from duty upon conviction. Some cooperative heads, however, have raised concerns about direct elections and making audit bodies permanent. They argue direct elections could turn NongHyup into a political organization and weaken professionalism. Others say constant oversight runs counter to the cooperative principle of autonomy. Ha Seung-soo, a lawyer with the NongHyup Reform Promotion Group, rejected that argument. “It is true that cooperatives should be guaranteed autonomy, but autonomy at a level that enables corruption cannot be accepted,” he said. He said the current indirect election system, in which only cooperative heads vote, has produced behavior close to “dividing up positions.” He added that breaking what he called an exclusive privilege through direct elections would make the organization healthier. The government said it will accelerate work on a second package of reforms. A government official said the first package aimed to prevent misconduct by the federation and its chair, while the second will focus on remaking NongHyup into an organization for farmers. The official said the government plans to announce the second package next month, drawing in part on Japan’s agricultural cooperative reforms. * This article has been translated by AI. 2026-05-07 06:04:10