Sleep tech — applying artificial intelligence, home appliances and health care technology to sleep management — is drawing attention as a next-generation growth industry. But as major conglomerates move in, concerns are also rising that they could squeeze out smaller players.

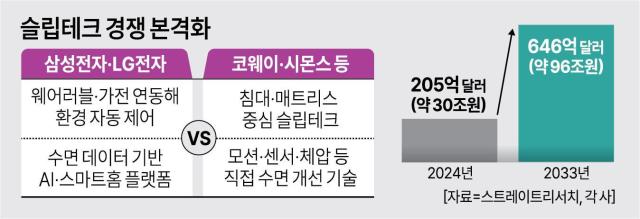

According to market research firm Straits Research on the 21st, the global sleep tech market topped $20.5 billion in 2024 and is projected to grow to $64.6918 billion by 2033.

Samsung Electronics and LG Electronics are approaching sleep tech as a connected lifestyle data business. The term combines “sleep” and “technology” and refers to measuring and analyzing sleep data using AI, the internet of things and big data to help people sleep better.

Samsung is upgrading a system centered on SmartThings that links sleep data collected from wearables such as the Galaxy Watch with air conditioners, air purifiers and lighting to automatically create an optimal sleep environment. The system adjusts temperature and brightness based on sleep stages, and changes air quality and lighting around wake-up time.

LG is also focusing on expanding sleep data across its broader appliance lineup under its “AI Home” strategy. It aims to provide personalized sleep environments by connecting appliances that control air quality, temperature and humidity, and to tie sleep data into health management through integration with health care platforms. LG is also reviewing the possibility of offering sleep management services bundled with its subscription-based appliance business.

As big companies enter the market with data and appliance ecosystems, competition is shifting quickly from individual products to platforms. Analysts say that if a structure takes hold in which multiple devices are connected around sleep data, market leadership could move toward appliance and platform companies.

That shift is also fueling criticism that large firms could disrupt the existing ecosystem. With sleep tech still in an early growth stage, industry watchers warn that companies with deep pockets and established platforms could rapidly tilt the competitive landscape.

Existing sleep tech players are responding by upgrading their technology. Coway, seen as a leading player, is strengthening a “full sleep-cycle management” strategy through its sleep and healing care brand BEREX, building out product lines that include motion beds, massage mattresses and sleep-sensor mattresses.

Simmons is also bolstering capabilities through premium mattresses, motion beds and experiential consulting. Jangsu Dolchimdae is pursuing business plans that combine heating technology with sleep and health care functions.

“Sleep tech has strong potential to grow into a high value-added industry by combining sleep data with health care,” an industry official said. “But if major companies take control of platforms, existing bed makers could be pushed into the role of simple hardware suppliers, making conflict unavoidable as the market is reshaped.”

* This article has been translated by AI.

Copyright ⓒ Aju Press All rights reserved.