As K-Culture emerges as a new growth engine for the national economy, some experts warn that the K-content industry may be entering a decline phase, a theory referred to as the 'peak theory.' This concern stems from an increasing reliance on foreign OTT platforms, which complicates the acquisition of key intellectual property (IP), alongside the rapid expansion of Chinese short drama platforms into global markets, including Southeast Asia.

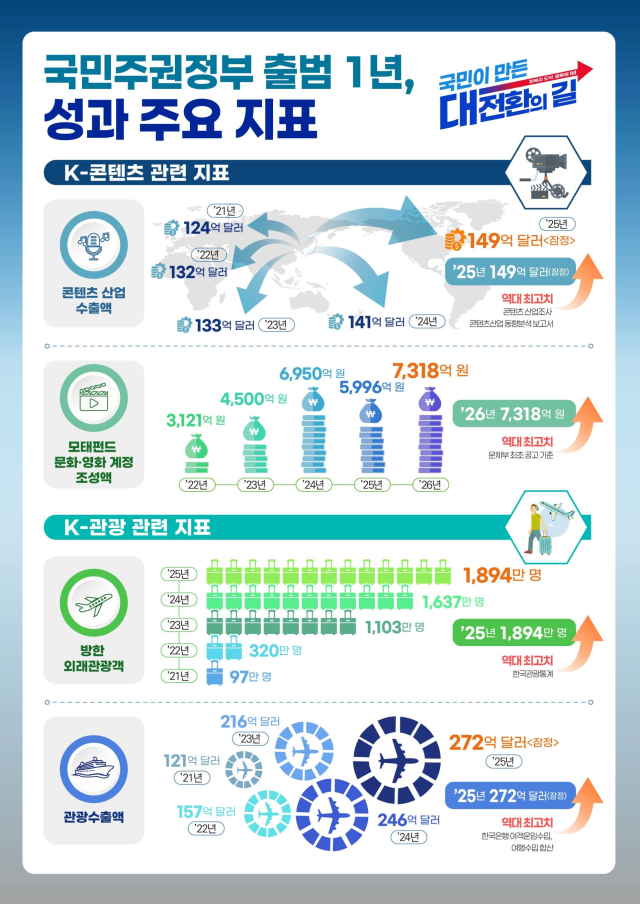

According to the Ministry of Culture, Sports and Tourism, K-content exports reached a record $14.9 billion (approximately 22.566 trillion won) last year. The influx of foreign tourists to South Korea also hit an all-time high of 18.94 million, driven by the spread of K-Culture.

The government is expanding support to enhance the competitiveness of the content industry. In 2026, it plans to establish the largest-ever cultural and film fund, totaling 731.8 billion won, and is preparing a global league fund based on foreign capital worth 150 billion won. In January of this year, a tax credit for webtoon production costs was introduced, and the expiration date for the tax credit on video content production costs has been extended to 2028.

The growth of K-content is positively impacting various sectors, including tourism, beauty, and food. The interest in South Korea generated through content is believed to enhance the country's brand value, creating a virtuous cycle that boosts demand for consumer goods and tourism. In fact, the Ministry of Culture estimates that when including beauty and food exports, the total K-Culture export scale reached approximately $71.8 billion last year, making it the third-largest export industry in the country, following semiconductors ($173.4 billion) and automobiles ($72 billion).

However, the mood in the industry is not entirely optimistic. The profitability of the content sector is declining due to intensified competition with global OTT platforms, rising production costs, and the proliferation of illegal distribution. Minister of Culture, Sports and Tourism Choi Hwi-young noted at a press conference on May 28 that during a previous briefing, he had mentioned, "K-Culture may have reached its peak," emphasizing the need for both the private sector and the government to seize current opportunities and collaborate.

The most pressing issue is the growing dependence on foreign OTT platforms. While the global status of K-content has improved, challenges such as reduced funding for the broadcasting industry, skyrocketing production costs, and limitations of advertising-based revenue models are hindering the competitiveness of domestic platforms. Notably, global OTT providers are adhering to a 'production investment model' that grants them exclusive rights to content IP, making it difficult for domestic producers to secure licensing revenue or secondary business rights, even if their works achieve global success.

Industry insiders express concern that the K-content sector could devolve into a 'subcontracting base for global platforms.' One industry source remarked, "Recently, we have seen a surge of Japanese and Chinese dramas on Netflix. These countries have lower production costs compared to Korea," adding that the success of the Chinese drama 'The Legend of the Jade Sword' is indicative of this trend.

Changes in content consumption patterns also present new variables. The short drama market from China is rapidly growing, particularly in Southeast Asia, putting pressure on the existing long-form streaming ecosystem. Chinese short drama platforms like RealShot and DramaBox have begun to aggressively target overseas markets in response to saturation in their domestic markets, resulting in a cumulative global download count exceeding 370 million as of the first quarter of last year.

Cultural critic Jeong Deok-hyun stated, "While interest and demand for K-content in overseas markets remain high, the internal foundation of the industry is not solid. Even if content is produced, securing sales and attracting investment is challenging." He further noted, "Just because some indicators have reached record highs does not mean the entire industry is thriving. The situation is difficult, as rising production costs and a market restructured around OTT platforms have made investors more cautious about risk management, leading to a reduction in production by traditional media outlets and a general contraction in content investment."

* This article has been translated by AI.

Copyright ⓒ Aju Press All rights reserved.