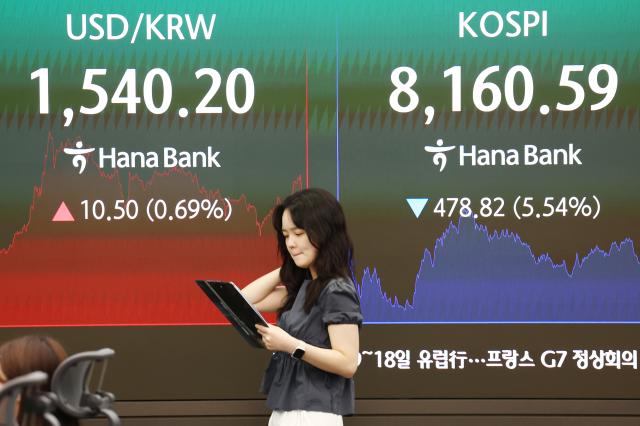

As tensions rise in the Middle East, international oil prices have surged, while U.S. stocks have experienced significant declines. In pre-market trading, major South Korean semiconductor companies, including Samsung Electronics and SK Hynix, saw their shares drop by 7% to 9%, indicating a downturn in investor sentiment and suggesting increased volatility for the KOSPI index.

On June 7, at 6 p.m. Eastern Time, West Texas Intermediate (WTI) crude oil for July delivery rose 3.39% to $93.61 per barrel. Similarly, Brent crude for August delivery also increased by the same percentage, reaching $96.25 per barrel. In contrast, futures for the Dow Jones fell by 0.34%, the S&P 500 by 0.42%, and the Nasdaq 100 by 0.44%, reflecting a growing aversion to riskier assets.

The U.S. stock market has been in a correction phase since late last week. On June 6, the Nasdaq Composite plummeted 4.18%, marking its largest single-day drop since April of the previous year. The S&P 500 and Dow Jones also fell by 2.64% and 695 points, respectively. Over the week, the Nasdaq dropped 4.7%, while the S&P 500 fell by more than 2%, highlighting a pronounced sell-off in technology stocks.

Market anxiety began with stronger-than-expected employment figures for May. A robust job market has led to rising Treasury yields, increasing speculation about further tightening by the Federal Reserve. Concerns have also grown regarding the funding burdens faced by tech companies heavily investing in artificial intelligence (AI). Additionally, Iran resumed missile attacks against Israel, reigniting geopolitical risks as a key market factor.

However, analysts believe the likelihood of this conflict escalating into a full-scale war remains limited. The ongoing negotiations for peace between the U.S. and Iran have not completely broken down, suggesting that the surge in oil prices may not be sustained. Investors are closely watching the upcoming U.S. Consumer Price Index (CPI) and Producer Price Index (PPI) reports, as well as SpaceX's anticipated IPO on June 12, to gauge future market direction.

Han Ji-young, a researcher at Kiwoom Securities, stated, "In the early part of the week, the aftershocks of the decline in U.S. semiconductor stocks will continue. However, midweek will bring significant events, including the U.S. May CPI report, Oracle's earnings, and the SpaceX listing, which will likely lead to increased volatility."

Despite this, he noted, "Following recent corrections, the KOSPI's forward price-to-earnings ratio (PER) has dropped to around 7.8, easing valuation pressures. Given that strong profit momentum in the semiconductor sector remains intact, the potential for a cascading decline is limited. Even if volatility increases during the week, it would be prudent to maintain existing positions rather than join in on panic selling."

As the U.S. stock market adjusts and geopolitical risks from the Middle East loom, South Korea's leading semiconductor firms, Samsung Electronics and SK Hynix, are both experiencing declines in pre-market trading.

As of 8:23 a.m. on June 8, Samsung Electronics was trading at 306,000 won, down 6.99% (23,000 won) from the previous trading day. SK Hynix also fell 9.23% to 1,879,000 won. Other companies, including LG Electronics, dropped 9.9% to 273,000 won, Naver fell 6.46% to 239,000 won, and Doosan Enerbility decreased by 8.58% to 87,400 won.

* This article has been translated by AI.

Copyright ⓒ Aju Press All rights reserved.