South Korea's economic narrative has been dictated by silicon in recent years. Memory giants have propelled the KOSPI past stock markets in cities such as London and Toronto while joining the exclusive trillion-dollar market-capitalization club.

In contrast, some of the country's oldest industrial pillars have been quietly fighting for survival.

Korea's refiners and petrochemical producers remain among the world's most sophisticated operators, supplying everything from jet fuel to high-value industrial materials. Yet they have found themselves squeezed between two forces beyond their control: a prolonged Middle East crisis that disrupted their feedstock lifeline and a flood of low-cost Chinese supply that has upended the naphtha-based business model on which the industry was built.

It is a reckoning for an industry that has long punched far above its weight.

South Korea hosts three of the world's ten largest refineries by single-site capacity, anchored by SK Energy's 840,000-barrel-per-day Ulsan complex and GS Caltex's 800,000-barrel-per-day Yeosu plant. Their facilities boast some of Asia's highest Nelson Complexity ratings, a measure of how much premium product a refinery can extract from each barrel of crude.

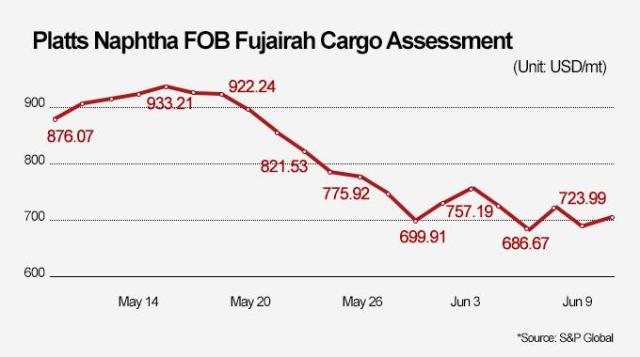

At the center of the strain sits naphtha, the feedstock so essential to the sector that industry executives often call it their "rice."

South Korea imported 237.5 million barrels of naphtha in 2025, more than any other country in Asia. That dependence left the industry acutely exposed when disruptions in the Strait of Hormuz squeezed supplies of the medium and heavy crude grades that generate the richest refining margins.

The shock rippled quickly through the market. Daily vessel transits through the strait fell to around 10 from a prewar average of 135, while Brent crude surged toward $94 a barrel.

For refiners that import nearly all of their feedstock and sell into an increasingly saturated market, every dollar increase in crude prices became harder to pass on to customers.

Then came the second blow.

Chinese producers, backed by an aggressive state-supported expansion expected to continue through at least 2028, flooded regional markets with low-cost ethylene and polymers. The result has been a structural glut that hollowed out margins on the very commodity-grade products Korean petrochemical companies were designed to mass-produce.

Ethylene, the bellwether of the chemicals industry, tells the story.

Prices that once approached $1,400 a ton have fallen below $1,000, erasing the cushion that had long kept aging crackers profitable.

Industry analysts expect Chinese capacity growth to outpace demand expansion for years to come.

"Without a normalization of the Strait of Hormuz, a sharp rebound in oil prices must be kept in mind at any moment. It may prove temporary, but in petrochemicals, where inventories were relatively thin, a belated rebound began to surface from late May," said Chun Woo-je, an analyst at KB Securities.

"Margins long mired in chronic oversupply are now at their highest in four years."

Seoul has responded with one of the industry's most sweeping restructuring efforts in decades.

"Unless the war ends on reasonable and viable terms sufficient to reassure shipowners and insurers, it may be extremely difficult for oil prices to return to prewar levels even in the long run," said Chung Tae-hun, an associate research fellow at the Korea Energy Economics Institute.

For many companies, the clearest path out of the squeeze runs straight into the sky.

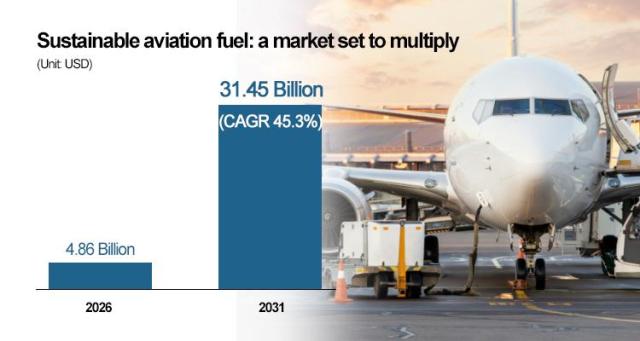

Refiners are betting heavily on sustainable aviation fuel, or SAF, a low-carbon alternative capable of reducing lifecycle emissions by up to 80 percent while commanding premium pricing under increasingly stringent global decarbonization mandates.

SK Energy has installed co-processing facilities at its Ulsan refinery and plans to expand its SAF supply network across the Asia-Pacific this year. GS Caltex is building a 500,000-ton annual SAF supply chain centered on an Indonesian biodiesel project, while S-Oil is refining its production processes to secure global certification.

The shift is spreading beyond refiners to chemical companies once thought immune to such transformations.

LG Chem, crossing from chemicals into fuel production, is constructing a 300,000-ton SAF plant in Daesan scheduled for completion in 2027 — a move that would have seemed unthinkable for a company built on plastics.

Diversification extends well beyond aviation.

LG Chem is steering toward advanced materials, battery cathodes and environmentally friendly products. Lotte Chemical is investing in super-engineering plastics used in robots and electric vehicles. Hanwha Solutions is expanding into insulation materials and specialty products for the power grids feeding AI data centers.

The pressure facing Korea is hardly unique.

Across Asia, manufacturing-heavy economies that never enjoyed a semiconductor windfall are struggling with the consequences of higher energy costs and structural oversupply. Japan, once a petrochemical powerhouse, is preparing to retire more than a quarter of its ethylene capacity by 2030. The center of gravity in Asian petrochemicals is visibly shifting.

For Korean firms, the calculation is stark.

They cannot win a price war fought on volume, nor can they insulate themselves from geopolitical shocks.

Their future lies in doing what they have always done best: turning engineering expertise into higher-value chemistry.

In an industry increasingly shaped by Chinese overcapacity and Middle East instability, the next chapter will be defined not by scale, but by sophistication.

Copyright ⓒ Aju Press All rights reserved.