As those habits harden, a growing list of institutions once considered too big to fail is discovering that their traditional business models no longer justify a physical trip.

The latest casualty is JoongAng Group, one of South Korea's largest media empires, whose holdings include the 61-year-old JoongAng Ilbo newspaper, broadcaster JTBC and cinema chain Megabox.

After JTBC defaulted on 20.6 billion won ($13.6 million) of debt this month, the group's holding company and five affiliates sought court-led rehabilitation.

The shock then spread further on Tuesday when JoongAng Ilbo disclosed an event of default on 137 billion won ($90 million) worth of corporate bonds, underscoring how quickly strains in one business line can ricochet across a conglomerate built for a pre-digital era.

The collapse echoes Homeplus' downfall a year earlier and points to a deeper restructuring underway: South Koreans increasingly buy the ordinary online and reserve offline trips only for the exceptional.

Yet the bigger question is whether these collapses signal a wholesale flight from physical stores, or something more selective: a market where consumers purchase commodities online and venture out only for experiences worth leaving home for.

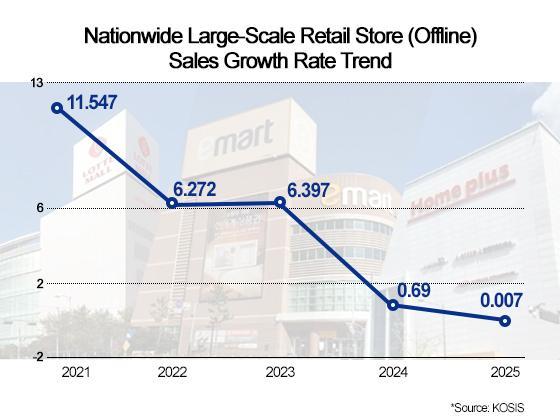

The hard numbers point to stagnation rather than freefall. Sales growth at large retailers, including hypermarkets and department stores, has flattened sharply, according to Korean Statistical Information Service data.

Once inflation is stripped out, that flat line arguably masks a real-terms contraction in revenue and margins — a slow bleed rather than a sudden wound.

Still, the downfall of Homeplus and Megabox owes as much to financial engineering and missed investment as to vanishing customers.

In Homeplus' case, labor unions and critics have pointed to MBK Partners' heavily leveraged 2015 buyout and a strategy of selling off prime stores to service debt, arguing that the chain missed its window to build online logistics while rivals such as Coupang poured in capital.

MBK has firmly rejected that account, saying it took no dividends from Homeplus after the acquisition and that buyout-related borrowing amounted to about 2.7 trillion won. It attributes the losses instead to regulatory restrictions on hypermarkets and the lingering impact of the pandemic.

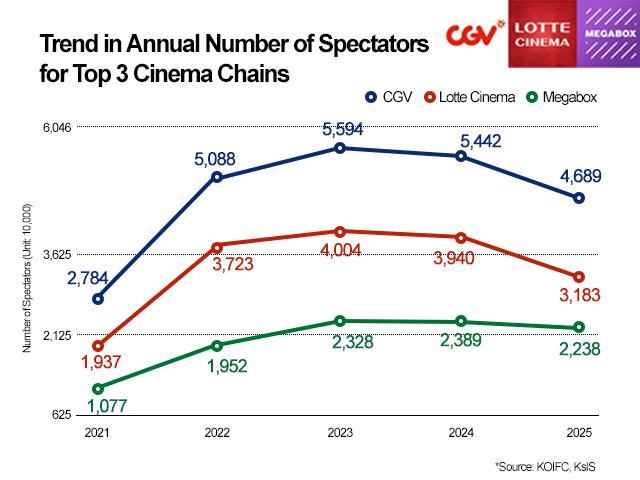

Megabox, meanwhile, lagged rivals CJ CGV and Lotte Cinema in core investment and lacked an in-house food-and-beverage affiliate to bolster concession margins, leaving it exposed as streaming platforms such as Netflix siphoned audiences away.

Its long-discussed merger with Lotte Cinema effectively collapsed once rehabilitation proceedings began.

The crisis has also widened beyond cinemas. JoongAng Ilbo said its corporate bonds became subject to early repayment after credit-rating downgrades triggered cross-default clauses tied to JTBC's debt default.

Under South Korean regulations, an event of default allows creditors to demand immediate repayment of principal and interest before maturity. The newspaper, which is pursuing a workout process, is expected to negotiate maturity extensions with creditors.

At a retail outlook seminar hosted by the Korea Chamber of Commerce and Industry in November, Ahn Tae-hee, managing director and partner at BCG Korea, described a sharp polarization of offline formats, with experience and price emerging as the only two viable poles.

"Only experiential stores that offer differentiated content or service, or transactional stores armed with overwhelming price competitiveness and high-turnover efficiency, are being chosen by consumers," Ahn said, adding that retailers stuck in between are "being pushed out of the market and facing restructuring pressure."

For hypermarkets, even their final stronghold is under siege.

"Fresh food, which had been the strength of large-format marts, is now shifting online," said Lee Chang-yeol, head of E-Mart's distribution research institute, at the same seminar.

He predicted the industry would concentrate even more heavily on delivery competitiveness, particularly quick commerce, in 2026.

Cinemas have absorbed a steady blow of their own.

"The shift of audiences to OTT is a stage we passed some time ago," a spokesperson for the Korean Film Council said, noting that even blockbuster hits can no longer reliably pull crowds back into theaters.

The council said it is working to have films released on streaming platforms formally recognized as films in their own right, while the three major theater chains, short of new hits, have increasingly leaned on re-releases of past blockbusters to entice viewers back.

The flip side of the story is a boom in experience-led retail, as consumers increasingly buy commodities online and venture out only for what a screen cannot replicate.

Pop-up stores have exploded as a result. The Popga platform logged 3,077 pop-ups between January and November 2025, up 79.6 percent from a year earlier.

Venues such as The Hyundai Seoul and Seoul's Seongsu-dong district have recast the store as a content space — built around AI-driven personalization and intellectual-property immersion — rather than a place merely to move boxes off shelves.

The crisis at South Korea's big-box retailers and multiplexes is therefore a twin failure: a distribution channel squeezed by online migration, compounded by managements that failed to invest in reinvention.

Offline retail has not died so much as changed its purpose. South Korea is becoming an early test case for a post-destination economy, where consumers no longer leave home to buy things, but only to do something worth leaving home for.

Copyright ⓒ Aju Press All rights reserved.