Journalist

Jong Eun Lee

-

SpaceX IPO Approaches as $1 Billion Flows into Space-Themed ETFs As the initial public offering (IPO) of U.S. space exploration company SpaceX approaches, significant investments are flowing into domestic space-themed exchange-traded funds (ETFs). Over the past week, more than 1 trillion won (approximately $1 billion) has been invested in these space-themed ETFs in South Korea. According to Koscom ETF Check on June 2, the TIGER U.S. Space Tech ETF saw a net inflow of 1.2725 trillion won, ranking second among all ETFs for fund inflows. Notably, on the previous day alone, 255.5 billion won was invested, demonstrating strong interest from investors. Individual investors were particularly active, with net purchases of 972.8 billion won, placing this ETF fourth among all ETFs during the same period. Other space industry ETFs also attracted significant funds. The KODEX U.S. Aerospace ETF received 169.9 billion won, ranking eighth in inflows, while the SOL U.S. Aerospace TOP10 saw an inflow of 36 billion won. With domestic investors unable to directly participate in the IPO, the growing demand for indirect investments through ETFs is evident. The surge in fund inflows is linked to SpaceX's upcoming investor roadshow starting June 4. The company is expected to clarify its funding size and final offering price, with plans to list on the Nasdaq as early as June 12. Market evaluations place the company's value between $1.75 trillion and $2 trillion, with the offering size estimated around $800 million, potentially setting a record for the largest IPO ever, surpassing the previous record held by Saudi Aramco at $29.4 billion. Attention is also focused on how this IPO might absorb investments in AI-related companies. Given the scale of the IPO, there are concerns that global institutional investors may liquidate some of their growth stocks to participate in the offering. Kim Il-hyuk, a researcher at KB Securities, noted, "Several companies in the same sector are likely to face supply shocks due to SpaceX's entry into the market." However, some analysts caution against interpreting this as a negative signal for the semiconductor industry as a whole. Due to the nature of SpaceX's business model, it could actually expand the demand base for the semiconductor ecosystem in the long term. Kim added, "SpaceX is expected to continue its focus on AI infrastructure investments, which may benefit semiconductor, equipment, and power infrastructure companies."* This article has been translated by AI. 2026-06-02 16:24:00

SpaceX IPO Approaches as $1 Billion Flows into Space-Themed ETFs As the initial public offering (IPO) of U.S. space exploration company SpaceX approaches, significant investments are flowing into domestic space-themed exchange-traded funds (ETFs). Over the past week, more than 1 trillion won (approximately $1 billion) has been invested in these space-themed ETFs in South Korea. According to Koscom ETF Check on June 2, the TIGER U.S. Space Tech ETF saw a net inflow of 1.2725 trillion won, ranking second among all ETFs for fund inflows. Notably, on the previous day alone, 255.5 billion won was invested, demonstrating strong interest from investors. Individual investors were particularly active, with net purchases of 972.8 billion won, placing this ETF fourth among all ETFs during the same period. Other space industry ETFs also attracted significant funds. The KODEX U.S. Aerospace ETF received 169.9 billion won, ranking eighth in inflows, while the SOL U.S. Aerospace TOP10 saw an inflow of 36 billion won. With domestic investors unable to directly participate in the IPO, the growing demand for indirect investments through ETFs is evident. The surge in fund inflows is linked to SpaceX's upcoming investor roadshow starting June 4. The company is expected to clarify its funding size and final offering price, with plans to list on the Nasdaq as early as June 12. Market evaluations place the company's value between $1.75 trillion and $2 trillion, with the offering size estimated around $800 million, potentially setting a record for the largest IPO ever, surpassing the previous record held by Saudi Aramco at $29.4 billion. Attention is also focused on how this IPO might absorb investments in AI-related companies. Given the scale of the IPO, there are concerns that global institutional investors may liquidate some of their growth stocks to participate in the offering. Kim Il-hyuk, a researcher at KB Securities, noted, "Several companies in the same sector are likely to face supply shocks due to SpaceX's entry into the market." However, some analysts caution against interpreting this as a negative signal for the semiconductor industry as a whole. Due to the nature of SpaceX's business model, it could actually expand the demand base for the semiconductor ecosystem in the long term. Kim added, "SpaceX is expected to continue its focus on AI infrastructure investments, which may benefit semiconductor, equipment, and power infrastructure companies."* This article has been translated by AI. 2026-06-02 16:24:00 -

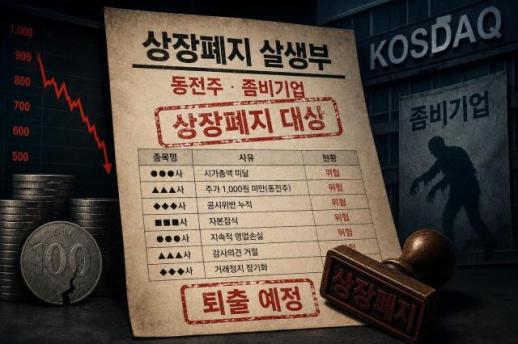

July Marks Critical Month for KOSDAQ as Delisting Risks Rise for 200 Companies The critical month of July is approaching, bringing with it a strengthened delisting system for KOSDAQ companies. Starting July 1, the new regulations will intensify efforts to weed out underperforming firms. Currently, over 200 companies are at risk of delisting due to factors such as insufficient market capitalization, penny stock status, and repeated disclosure violations. According to financial authorities, the enhanced delisting criteria will take effect on July 1. Companies with a market capitalization below 20 billion won, stocks priced under 1,000 won, or those accumulating 10 or more penalty points for disclosure violations (down from the previous threshold of 15 points) will be targeted for delisting. As of July 1, among the 1,822 KOSDAQ-listed companies (excluding SPACs), 134 have a market capitalization below 20 billion won, and 109 are classified as penny stocks. After excluding duplicates, approximately 203 companies are expected to fall into the potential delisting category. In addition to market capitalization criteria, many companies are also facing challenges due to disclosure violations. Currently, 70 KOSDAQ companies have been penalized under exchange management standards, with 16 of them accumulating 10 or more penalty points. The company with the highest penalty points is Coas, with a total of 42 points, followed by Daewon Sys with 23 points, CCS with 22.5 points, and Korea Union Pharma with over 21 points. Concerns about financial stability are also rising, as three KOSDAQ companies have been newly designated as management issues this year due to capital impairment rates exceeding 50%: AB Pro Bio, Iwon Compo Tech, and DAP. Market analysts predict that if delistings begin in July, the impact on retail shareholders could be significant. As of the end of last year, there were approximately 2.63 million retail investors holding shares in companies with a market capitalization below 20 billion won and classified as penny stocks. Some of these companies have thousands of individual investors, raising concerns that many will suffer losses if delistings occur. A securities industry representative stated, "The authorities aim to eliminate companies that have only maintained their listings while increasing investor losses." However, given the high proportion of retail investors in the KOSDAQ market, it is essential to establish protective measures for minority shareholders during the delisting process.* This article has been translated by AI. 2026-06-02 16:21:00

July Marks Critical Month for KOSDAQ as Delisting Risks Rise for 200 Companies The critical month of July is approaching, bringing with it a strengthened delisting system for KOSDAQ companies. Starting July 1, the new regulations will intensify efforts to weed out underperforming firms. Currently, over 200 companies are at risk of delisting due to factors such as insufficient market capitalization, penny stock status, and repeated disclosure violations. According to financial authorities, the enhanced delisting criteria will take effect on July 1. Companies with a market capitalization below 20 billion won, stocks priced under 1,000 won, or those accumulating 10 or more penalty points for disclosure violations (down from the previous threshold of 15 points) will be targeted for delisting. As of July 1, among the 1,822 KOSDAQ-listed companies (excluding SPACs), 134 have a market capitalization below 20 billion won, and 109 are classified as penny stocks. After excluding duplicates, approximately 203 companies are expected to fall into the potential delisting category. In addition to market capitalization criteria, many companies are also facing challenges due to disclosure violations. Currently, 70 KOSDAQ companies have been penalized under exchange management standards, with 16 of them accumulating 10 or more penalty points. The company with the highest penalty points is Coas, with a total of 42 points, followed by Daewon Sys with 23 points, CCS with 22.5 points, and Korea Union Pharma with over 21 points. Concerns about financial stability are also rising, as three KOSDAQ companies have been newly designated as management issues this year due to capital impairment rates exceeding 50%: AB Pro Bio, Iwon Compo Tech, and DAP. Market analysts predict that if delistings begin in July, the impact on retail shareholders could be significant. As of the end of last year, there were approximately 2.63 million retail investors holding shares in companies with a market capitalization below 20 billion won and classified as penny stocks. Some of these companies have thousands of individual investors, raising concerns that many will suffer losses if delistings occur. A securities industry representative stated, "The authorities aim to eliminate companies that have only maintained their listings while increasing investor losses." However, given the high proportion of retail investors in the KOSDAQ market, it is essential to establish protective measures for minority shareholders during the delisting process.* This article has been translated by AI. 2026-06-02 16:21:00 -

Syangyong Construction Wins 123 Billion Won Contract for Mapo Redevelopment Project Syangyong Construction is expanding its contracts for housing redevelopment projects in Seoul and the surrounding metropolitan area. On June 2, the company announced that it was selected as the construction firm during a general assembly of the Changjeon-dong housing redevelopment association held on May 31. The project involves constructing six apartment buildings named 'The Platinum,' consisting of 292 units, along with community facilities, on the site located at 46-1 Changjeon-dong. The construction cost is estimated at 123 billion won, with a projected timeline of approximately 44 months from the start of construction. The site is part of Seoul's Moa Town initiative and is conveniently located near Sinchon Station on Line 2 and Gwangheungchang and Daehyeong Stations on Line 6, with Gwangheungchang Station just a four-minute walk away. Including this project, Syangyong Construction has been accumulating contracts in major redevelopment projects across Seoul, such as the Hong-eun-dong housing redevelopment, the Siheung 5-dong Moa Town project, the Cheonho-dong housing redevelopment, and the Noryangjin Eunha Mansion area redevelopment. A representative from Syangyong Construction stated in a phone interview, "We plan to continue securing contracts for housing redevelopment projects in the future." Meanwhile, due to a recent downturn in the construction market and a contraction in the project financing sector, mid-sized construction companies are increasingly focusing on smaller-scale redevelopment projects like housing redevelopment.* This article has been translated by AI. 2026-06-02 16:21:00

Syangyong Construction Wins 123 Billion Won Contract for Mapo Redevelopment Project Syangyong Construction is expanding its contracts for housing redevelopment projects in Seoul and the surrounding metropolitan area. On June 2, the company announced that it was selected as the construction firm during a general assembly of the Changjeon-dong housing redevelopment association held on May 31. The project involves constructing six apartment buildings named 'The Platinum,' consisting of 292 units, along with community facilities, on the site located at 46-1 Changjeon-dong. The construction cost is estimated at 123 billion won, with a projected timeline of approximately 44 months from the start of construction. The site is part of Seoul's Moa Town initiative and is conveniently located near Sinchon Station on Line 2 and Gwangheungchang and Daehyeong Stations on Line 6, with Gwangheungchang Station just a four-minute walk away. Including this project, Syangyong Construction has been accumulating contracts in major redevelopment projects across Seoul, such as the Hong-eun-dong housing redevelopment, the Siheung 5-dong Moa Town project, the Cheonho-dong housing redevelopment, and the Noryangjin Eunha Mansion area redevelopment. A representative from Syangyong Construction stated in a phone interview, "We plan to continue securing contracts for housing redevelopment projects in the future." Meanwhile, due to a recent downturn in the construction market and a contraction in the project financing sector, mid-sized construction companies are increasingly focusing on smaller-scale redevelopment projects like housing redevelopment.* This article has been translated by AI. 2026-06-02 16:21:00 -

Small Asset Managers Target ETF Market Beyond Samsung and Mirae Asset Domestic exchange-traded funds (ETFs) have entered a 500 trillion won era, prompting small and mid-sized asset management firms to actively pursue opportunities in the ETF market. While Samsung Asset Management and Mirae Asset Management dominate with over 70% market share, these smaller firms are seeking new growth avenues, particularly through active ETFs. According to the financial investment industry on June 2, firms such as DS Asset Management, Life Asset Management, Daol Asset Management, and iM Asset Management are exploring entry or expansion into the ETF business. DS Asset Management has completed its ETF organizational setup by hiring Jeong Seong-in, who previously led the ETF business at Kiwoom Investment Management, and aims to launch an active ETF on the KOSDAQ by July. The firm plans to introduce up to three ETF products in the second half of the year. Life Asset Management has applied for a public fund management license. Currently holding only a private fund license, the firm plans to enter the ETF market as soon as it receives approval for public funds. Daol Asset Management is also in the process of hiring staff with an eye on entering the ETF market. Meanwhile, iM Asset Management is reviewing the launch of new products after releasing a KOSPI 200 ETF in February of last year. Just a few years ago, skepticism prevailed regarding the entry of small and mid-sized asset managers into the ETF market. The prevailing belief was that the business required economies of scale, making it difficult for latecomers to survive. Currently, Samsung Asset Management and Mirae Asset Management together hold a combined market share of 70% in the domestic ETF market. Despite this, small and mid-sized firms cannot ignore the ETF market, as it has become a core business in asset management. With the ETF market capitalization exceeding 500 trillion won, it has emerged as a key vehicle for individual investors to channel significant funds into the stock market. The growth of active ETFs is particularly encouraging smaller firms to enter the market. Unlike passive ETFs, which simply track an index, active ETFs allow fund managers' investment decisions to directly influence returns. Firms with extensive experience in private equity management are seen as well-positioned to identify specific industries or stocks and implement concentrated investment strategies through active ETFs. Profitability is also an attractive factor. While scale competition is crucial in the ETF market, active ETFs can command relatively higher fees based on differentiated management performance. Investors, expecting higher returns, are generally less resistant to higher fees. The business model is shifting toward securing profitability based on management performance rather than competing solely on assets under management (AUM). A notable example is Timefolio Asset Management. By focusing on active ETFs, Timefolio's market share jumped from 10th place at the end of 2024 to 7th place in March of this year. Its profitability has also significantly increased, with a net profit of 85.1 billion won for the 2025 fiscal year, a 145% rise from 34.7 billion won the previous year. Industry experts believe that the performance of DS Asset Management will be a pivotal factor in determining the speed at which small and mid-sized firms enter the ETF market. Despite the increasing polarization in the ETF market, the emergence of additional success stories through active ETFs could lead to more private equity firms entering the ETF space. An industry insider remarked, "In the past, the ETF market was seen as the domain of large firms, but now there is a new option with active ETFs. As firms with private equity management experience begin to incorporate their unique investment strategies into ETFs, the competitive landscape may gradually change." 2026-06-02 16:21:00

Small Asset Managers Target ETF Market Beyond Samsung and Mirae Asset Domestic exchange-traded funds (ETFs) have entered a 500 trillion won era, prompting small and mid-sized asset management firms to actively pursue opportunities in the ETF market. While Samsung Asset Management and Mirae Asset Management dominate with over 70% market share, these smaller firms are seeking new growth avenues, particularly through active ETFs. According to the financial investment industry on June 2, firms such as DS Asset Management, Life Asset Management, Daol Asset Management, and iM Asset Management are exploring entry or expansion into the ETF business. DS Asset Management has completed its ETF organizational setup by hiring Jeong Seong-in, who previously led the ETF business at Kiwoom Investment Management, and aims to launch an active ETF on the KOSDAQ by July. The firm plans to introduce up to three ETF products in the second half of the year. Life Asset Management has applied for a public fund management license. Currently holding only a private fund license, the firm plans to enter the ETF market as soon as it receives approval for public funds. Daol Asset Management is also in the process of hiring staff with an eye on entering the ETF market. Meanwhile, iM Asset Management is reviewing the launch of new products after releasing a KOSPI 200 ETF in February of last year. Just a few years ago, skepticism prevailed regarding the entry of small and mid-sized asset managers into the ETF market. The prevailing belief was that the business required economies of scale, making it difficult for latecomers to survive. Currently, Samsung Asset Management and Mirae Asset Management together hold a combined market share of 70% in the domestic ETF market. Despite this, small and mid-sized firms cannot ignore the ETF market, as it has become a core business in asset management. With the ETF market capitalization exceeding 500 trillion won, it has emerged as a key vehicle for individual investors to channel significant funds into the stock market. The growth of active ETFs is particularly encouraging smaller firms to enter the market. Unlike passive ETFs, which simply track an index, active ETFs allow fund managers' investment decisions to directly influence returns. Firms with extensive experience in private equity management are seen as well-positioned to identify specific industries or stocks and implement concentrated investment strategies through active ETFs. Profitability is also an attractive factor. While scale competition is crucial in the ETF market, active ETFs can command relatively higher fees based on differentiated management performance. Investors, expecting higher returns, are generally less resistant to higher fees. The business model is shifting toward securing profitability based on management performance rather than competing solely on assets under management (AUM). A notable example is Timefolio Asset Management. By focusing on active ETFs, Timefolio's market share jumped from 10th place at the end of 2024 to 7th place in March of this year. Its profitability has also significantly increased, with a net profit of 85.1 billion won for the 2025 fiscal year, a 145% rise from 34.7 billion won the previous year. Industry experts believe that the performance of DS Asset Management will be a pivotal factor in determining the speed at which small and mid-sized firms enter the ETF market. Despite the increasing polarization in the ETF market, the emergence of additional success stories through active ETFs could lead to more private equity firms entering the ETF space. An industry insider remarked, "In the past, the ETF market was seen as the domain of large firms, but now there is a new option with active ETFs. As firms with private equity management experience begin to incorporate their unique investment strategies into ETFs, the competitive landscape may gradually change." 2026-06-02 16:21:00 -

Stock Consolidation Surge: One-Third of Companies Remain Penny Stocks KOSDAQ-listed company Kespion, a manufacturer of wireless communication devices, has struggled with stagnant stock prices for years. On February 23, the company announced a 2-for-1 stock consolidation (from 500 won to 1,000 won per share). While the stated purpose was to stabilize stock prices and enhance corporate value by maintaining an appropriate number of circulating shares, the real motivation was to avoid the so-called "penny stock delisting" criteria announced by financial authorities in mid-February. After a trading suspension lasting over two months, trading resumed on May 4, but Kespion's stock closed at 751 won on June 1. The company's discussion forums are filled with anxious shareholders worried about delisting. This year, the KOSDAQ market has seen a surge in stock consolidation announcements. Following the government's announcement of measures to eliminate penny stocks and reform delisting regulations in February, related disclosures have skyrocketed. The number of stock consolidation announcements from January to May has increased more than twenty-fold compared to the same period last year. This move is seen as a survival tactic to artificially inflate stock prices. However, the limitations are evident. It is estimated that one in three companies that decided to consolidate their stocks this year still remain penny stocks with prices below 1,000 won, putting them at risk of being listed on the "delisting blacklist." According to the Financial Supervisory Service's electronic disclosure system, 159 KOSDAQ companies announced stock consolidation decisions from January to May this year. This marks an increase of over twenty times compared to just seven announcements during the same period last year. Excluding six companies that had their proposals rejected at shareholder meetings, a total of 153 companies are currently pursuing or have completed stock consolidations. This represents about 8.4% of the total 1,822 KOSDAQ-listed companies (excluding SPACs). The urgency behind these consolidations stems from the impending delisting of penny stocks. According to revised KOSDAQ listing regulations, companies whose stock prices fall below 1,000 won for 30 consecutive trading days will be designated as management items. If they fail to exceed this threshold for 45 out of the next 90 trading days, they will face final delisting procedures. The revisions also include measures to prevent circumvention. Companies that have conducted stock consolidations or reductions in the past year are prohibited from further consolidations or reductions for 90 trading days after being designated as management items. Additionally, any consolidation or reduction exceeding a 10-to-1 ratio is not allowed during this 90-day period. Violating these rules will result in immediate delisting. The problem is that stock consolidation is not a fundamental solution for escaping penny stock status. Among the 153 companies that have pursued or completed stock consolidations, 49 (32.0%) still had stock prices below 1,000 won as of the end of last month. For instance, Wonpung Moolsan, which decided on a stock consolidation in March, had a closing price of just 524 won on June 1. Other KOSDAQ companies at risk of delisting due to two consecutive years of delisting criteria include Samyoung ENC and Tubesoft, both of which have market capitalizations below 20 billion won. Currently, Samyoung ENC has been granted a three-month improvement period, while Tubesoft is awaiting a decision on its delisting from the Corporate Review Committee. A securities industry insider noted, "It is not easy for companies to improve their performance or financial structure in the short term, so many companies are likely to become candidates for delisting. Companies that cannot escape penny stock status through consolidation are at a significant crossroads for survival." Market analysts caution against interpreting stock consolidation as a signal of improved corporate value. Stock consolidation merely reduces the number of circulating shares while increasing the price per share, without changing the market capitalization or actual value of the company. For example, Aptun, which resumed trading on May 8, saw its stock price surge close to the upper limit immediately after trading resumed, but it ultimately closed down 17.54% from the previous trading day due to profit-taking. In addition to KOSDAQ, there are companies in the KOSPI market facing delisting risks. There are a significant number of potential risk companies in the KOSPI market as well. Currently, there are 99 companies with market capitalizations below 30 billion won and 39 penny stocks with prices below 1,000 won. Excluding duplicates, a total of 129 companies fall under at least one of these criteria. Notably, the KOSPI market has also seen an increase in forced delisting cases this year. In the past three years (2023-2025), only five companies were delisted due to reasons such as rejection of audit opinions, but this year, five companies, including Daedong Electronics, Kukbo, Well Biotech, IHQ, and Philux, have already been delisted. Recently, the delisting of Geumyang, which has 240,000 shareholders, has caused a stir. Geumyang is currently seeking legal action against the Korea Exchange's delisting decision by filing for a suspension of the decision's effectiveness. 2026-06-02 16:21:00

Stock Consolidation Surge: One-Third of Companies Remain Penny Stocks KOSDAQ-listed company Kespion, a manufacturer of wireless communication devices, has struggled with stagnant stock prices for years. On February 23, the company announced a 2-for-1 stock consolidation (from 500 won to 1,000 won per share). While the stated purpose was to stabilize stock prices and enhance corporate value by maintaining an appropriate number of circulating shares, the real motivation was to avoid the so-called "penny stock delisting" criteria announced by financial authorities in mid-February. After a trading suspension lasting over two months, trading resumed on May 4, but Kespion's stock closed at 751 won on June 1. The company's discussion forums are filled with anxious shareholders worried about delisting. This year, the KOSDAQ market has seen a surge in stock consolidation announcements. Following the government's announcement of measures to eliminate penny stocks and reform delisting regulations in February, related disclosures have skyrocketed. The number of stock consolidation announcements from January to May has increased more than twenty-fold compared to the same period last year. This move is seen as a survival tactic to artificially inflate stock prices. However, the limitations are evident. It is estimated that one in three companies that decided to consolidate their stocks this year still remain penny stocks with prices below 1,000 won, putting them at risk of being listed on the "delisting blacklist." According to the Financial Supervisory Service's electronic disclosure system, 159 KOSDAQ companies announced stock consolidation decisions from January to May this year. This marks an increase of over twenty times compared to just seven announcements during the same period last year. Excluding six companies that had their proposals rejected at shareholder meetings, a total of 153 companies are currently pursuing or have completed stock consolidations. This represents about 8.4% of the total 1,822 KOSDAQ-listed companies (excluding SPACs). The urgency behind these consolidations stems from the impending delisting of penny stocks. According to revised KOSDAQ listing regulations, companies whose stock prices fall below 1,000 won for 30 consecutive trading days will be designated as management items. If they fail to exceed this threshold for 45 out of the next 90 trading days, they will face final delisting procedures. The revisions also include measures to prevent circumvention. Companies that have conducted stock consolidations or reductions in the past year are prohibited from further consolidations or reductions for 90 trading days after being designated as management items. Additionally, any consolidation or reduction exceeding a 10-to-1 ratio is not allowed during this 90-day period. Violating these rules will result in immediate delisting. The problem is that stock consolidation is not a fundamental solution for escaping penny stock status. Among the 153 companies that have pursued or completed stock consolidations, 49 (32.0%) still had stock prices below 1,000 won as of the end of last month. For instance, Wonpung Moolsan, which decided on a stock consolidation in March, had a closing price of just 524 won on June 1. Other KOSDAQ companies at risk of delisting due to two consecutive years of delisting criteria include Samyoung ENC and Tubesoft, both of which have market capitalizations below 20 billion won. Currently, Samyoung ENC has been granted a three-month improvement period, while Tubesoft is awaiting a decision on its delisting from the Corporate Review Committee. A securities industry insider noted, "It is not easy for companies to improve their performance or financial structure in the short term, so many companies are likely to become candidates for delisting. Companies that cannot escape penny stock status through consolidation are at a significant crossroads for survival." Market analysts caution against interpreting stock consolidation as a signal of improved corporate value. Stock consolidation merely reduces the number of circulating shares while increasing the price per share, without changing the market capitalization or actual value of the company. For example, Aptun, which resumed trading on May 8, saw its stock price surge close to the upper limit immediately after trading resumed, but it ultimately closed down 17.54% from the previous trading day due to profit-taking. In addition to KOSDAQ, there are companies in the KOSPI market facing delisting risks. There are a significant number of potential risk companies in the KOSPI market as well. Currently, there are 99 companies with market capitalizations below 30 billion won and 39 penny stocks with prices below 1,000 won. Excluding duplicates, a total of 129 companies fall under at least one of these criteria. Notably, the KOSPI market has also seen an increase in forced delisting cases this year. In the past three years (2023-2025), only five companies were delisted due to reasons such as rejection of audit opinions, but this year, five companies, including Daedong Electronics, Kukbo, Well Biotech, IHQ, and Philux, have already been delisted. Recently, the delisting of Geumyang, which has 240,000 shareholders, has caused a stir. Geumyang is currently seeking legal action against the Korea Exchange's delisting decision by filing for a suspension of the decision's effectiveness. 2026-06-02 16:21:00 -

Samsung Electronics Surges Past Meta to Join Global Top 10 by Market Cap The KOSPI index experienced significant fluctuations, swinging over 400 points before closing higher. Amid this volatility, Samsung Electronics saw its stock rise by more than 3%, securing a spot among the top 10 global companies by market capitalization. On June 2, according to data from the global market capitalization tracking site CompaniesMarketCap, Samsung Electronics' market cap reached $1.526 trillion, surpassing Meta to rank 10th globally. At one point during the trading session, it even exceeded Tesla, which ranked 9th. Samsung Electronics closed at 360,500 won, up 11,500 won (3.30%) from the previous trading day. Its market capitalization increased to 2,107.58 trillion won, setting a new record for the highest closing price. In contrast, the domestic stock market exhibited extreme volatility. The KOSPI closed up 13.11 points (0.15%) at 8,801.49. The index opened at 8,883.19 and briefly rose to 8,933.62, attempting to break through the 8,900 mark. However, heavy selling by foreign investors pushed it down to the 8,503 level, resulting in a drop of 4.9% from its intraday high. The index managed to recover most of its losses, finishing in positive territory. In the securities market, individual and institutional investors made net purchases of 8.1191 trillion won and 237 billion won, respectively, while foreign investors sold off 8.0505 trillion won. Among the top market cap stocks, Samsung Electronics provided crucial support to the market. SK Hynix closed slightly lower at -0.13%, while SK Square (7.17%), Samsung Life (17.07%), and Samsung C&T (6.70%) showed strong gains. Conversely, Hyundai Motor (-2.80%), LG Energy Solution (-2.75%), HD Hyundai Heavy Industries (-1.61%), and Samsung Electro-Mechanics (-9.58%) saw declines. Market analysts suggest that funds have been concentrated in Samsung Electronics, viewed as a major beneficiary of the recent rally in AI semiconductors. Kang Jin-hyuk, a researcher at Shinhan Investment Corp, noted, "The volatility of the index has increased due to profit-taking ahead of local elections, but Samsung Electronics has maintained relative strength, drawing significant investor interest as it reached the 10th position in global market capitalization during the session." Indeed, Samsung Electronics' stock has surged over 60% in the past month. The stock price, which was in the 220,000 won range at the end of April, surpassed 360,000 won on this day. During the same period, its market capitalization increased by approximately 800 trillion won. In the global market cap rankings, Nvidia remains in first place with a valuation of $5.4 trillion, followed by Alphabet, Apple, Microsoft, and Amazon. Among Asian companies, Samsung Electronics and SK Hynix both have market capitalizations exceeding $1 trillion, following TSMC. The KOSDAQ index closed down 24.00 points (2.29%) at 1,026.03. Foreign and institutional investors made net purchases of 337.3 billion won and 126.2 billion won, respectively, while individuals sold off 449.6 billion won.* This article has been translated by AI. 2026-06-02 16:18:00

Samsung Electronics Surges Past Meta to Join Global Top 10 by Market Cap The KOSPI index experienced significant fluctuations, swinging over 400 points before closing higher. Amid this volatility, Samsung Electronics saw its stock rise by more than 3%, securing a spot among the top 10 global companies by market capitalization. On June 2, according to data from the global market capitalization tracking site CompaniesMarketCap, Samsung Electronics' market cap reached $1.526 trillion, surpassing Meta to rank 10th globally. At one point during the trading session, it even exceeded Tesla, which ranked 9th. Samsung Electronics closed at 360,500 won, up 11,500 won (3.30%) from the previous trading day. Its market capitalization increased to 2,107.58 trillion won, setting a new record for the highest closing price. In contrast, the domestic stock market exhibited extreme volatility. The KOSPI closed up 13.11 points (0.15%) at 8,801.49. The index opened at 8,883.19 and briefly rose to 8,933.62, attempting to break through the 8,900 mark. However, heavy selling by foreign investors pushed it down to the 8,503 level, resulting in a drop of 4.9% from its intraday high. The index managed to recover most of its losses, finishing in positive territory. In the securities market, individual and institutional investors made net purchases of 8.1191 trillion won and 237 billion won, respectively, while foreign investors sold off 8.0505 trillion won. Among the top market cap stocks, Samsung Electronics provided crucial support to the market. SK Hynix closed slightly lower at -0.13%, while SK Square (7.17%), Samsung Life (17.07%), and Samsung C&T (6.70%) showed strong gains. Conversely, Hyundai Motor (-2.80%), LG Energy Solution (-2.75%), HD Hyundai Heavy Industries (-1.61%), and Samsung Electro-Mechanics (-9.58%) saw declines. Market analysts suggest that funds have been concentrated in Samsung Electronics, viewed as a major beneficiary of the recent rally in AI semiconductors. Kang Jin-hyuk, a researcher at Shinhan Investment Corp, noted, "The volatility of the index has increased due to profit-taking ahead of local elections, but Samsung Electronics has maintained relative strength, drawing significant investor interest as it reached the 10th position in global market capitalization during the session." Indeed, Samsung Electronics' stock has surged over 60% in the past month. The stock price, which was in the 220,000 won range at the end of April, surpassed 360,000 won on this day. During the same period, its market capitalization increased by approximately 800 trillion won. In the global market cap rankings, Nvidia remains in first place with a valuation of $5.4 trillion, followed by Alphabet, Apple, Microsoft, and Amazon. Among Asian companies, Samsung Electronics and SK Hynix both have market capitalizations exceeding $1 trillion, following TSMC. The KOSDAQ index closed down 24.00 points (2.29%) at 1,026.03. Foreign and institutional investors made net purchases of 337.3 billion won and 126.2 billion won, respectively, while individuals sold off 449.6 billion won.* This article has been translated by AI. 2026-06-02 16:18:00 -

Global Protectionism Challenges K-Defense Exports Amid Local Production Demands As countries accelerate their defense self-sufficiency, the export formula for K-Defense is facing significant challenges. The environment has become increasingly difficult, where quick delivery and price competitiveness alone may not guarantee large contracts. Experts suggest that securing new competitive advantages, such as local production and technology transfer, is essential. Price and Localization Leave K-Defense Vulnerable to 'Buy European' Policies According to industry sources, Hanwha Aerospace recently failed to secure a contract for Romania's next-generation infantry fighting vehicle (IFV) project. The Romanian Ministry of Defense announced on May 29 that it had selected Germany's Rheinmetall as the final contractor through the European Security Action (SAFE) program. This project, aimed at replacing the aging infantry fighting vehicles currently in use by the Romanian military, has a total budget of €3.337 billion (approximately 5.9 trillion won). Hanwha Aerospace and Rheinmetall were in competition for the final contractor selection. In terms of competitiveness, Hanwha Aerospace was not at a disadvantage. It proposed supplying 298 AS21 Redback vehicles for €2.8 billion, while Rheinmetall offered 232 KF41 Lynx vehicles for €2.59 billion. On a per-unit basis, the Redback (approximately €9.35 million) was cheaper than the Lynx (€11.16 million). Hanwha Aerospace also met the Romanian government's requirement for 'complete localization,' proposing to increase local production from 80% to 90% in the long term. In contrast, Rheinmetall reportedly proposed a localization rate of around 40%. Despite this, the Romanian government chose Rheinmetall. Industry analysts note that the European Union's policy to foster domestic defense industries may have influenced this decision. The growing 'Buy European' sentiment is raising the barriers for foreign companies seeking contracts. In the Middle East, the trend of prioritizing domestic production is also intensifying. For instance, Saudi Arabia has committed to procuring over 50% of its defense spending through domestic defense companies as part of its Vision 2030 initiative. As a result, local production and industrial cooperation are becoming key factors in major projects pursued by domestic defense firms, including Hanwha Aerospace's K9 self-propelled howitzer and Redback, Hyundai Rotem's K2 tank, and LIG Nex1's L-SAM. K-Defense Must Revise Export Strategy The increasing demands for local production and technology transfer in Europe and the Middle East stem from a heightened awareness of defense self-sufficiency following the Russia-Ukraine war. Initially, European countries relied on South Korean weapons due to a lack of production capacity. Quick delivery and reasonable pricing enabled K-Defense to penetrate the European market. However, as the war has prolonged, European nations have recognized the importance of expanding production facilities and establishing joint procurement systems, diminishing the 'gap-filler' role that South Korean defense had previously enjoyed. Choi Gi-il, a professor at Sangji University, stated, "Just a few years ago, European defense companies lacked sufficient production capacity, allowing K-Defense to fill the gaps. However, with Germany and France rapidly recovering their production capabilities, the competitive landscape is changing." Germany, a leading defense power in Europe, is increasing its total defense spending to €108.2 billion (approximately 170 trillion won) this year to enhance its domestic defense production capabilities. France is also expanding its defense investments and production capacity. Experts argue that K-Defense needs to find new breakthroughs to succeed in Europe and the Middle East, emphasizing the need for enhanced local cooperation and cross-industry collaborations. Nam Myung-ryul, head of the K-Defense Center at Korea University, remarked, "We must go beyond merely selling weapons to establishing local production facilities and proposing industrial cooperation models. A package cooperation strategy that links defense with industries where Korea has strengths, such as energy, artificial intelligence, and information and communication technology, is essential." 2026-06-02 16:12:00

Global Protectionism Challenges K-Defense Exports Amid Local Production Demands As countries accelerate their defense self-sufficiency, the export formula for K-Defense is facing significant challenges. The environment has become increasingly difficult, where quick delivery and price competitiveness alone may not guarantee large contracts. Experts suggest that securing new competitive advantages, such as local production and technology transfer, is essential. Price and Localization Leave K-Defense Vulnerable to 'Buy European' Policies According to industry sources, Hanwha Aerospace recently failed to secure a contract for Romania's next-generation infantry fighting vehicle (IFV) project. The Romanian Ministry of Defense announced on May 29 that it had selected Germany's Rheinmetall as the final contractor through the European Security Action (SAFE) program. This project, aimed at replacing the aging infantry fighting vehicles currently in use by the Romanian military, has a total budget of €3.337 billion (approximately 5.9 trillion won). Hanwha Aerospace and Rheinmetall were in competition for the final contractor selection. In terms of competitiveness, Hanwha Aerospace was not at a disadvantage. It proposed supplying 298 AS21 Redback vehicles for €2.8 billion, while Rheinmetall offered 232 KF41 Lynx vehicles for €2.59 billion. On a per-unit basis, the Redback (approximately €9.35 million) was cheaper than the Lynx (€11.16 million). Hanwha Aerospace also met the Romanian government's requirement for 'complete localization,' proposing to increase local production from 80% to 90% in the long term. In contrast, Rheinmetall reportedly proposed a localization rate of around 40%. Despite this, the Romanian government chose Rheinmetall. Industry analysts note that the European Union's policy to foster domestic defense industries may have influenced this decision. The growing 'Buy European' sentiment is raising the barriers for foreign companies seeking contracts. In the Middle East, the trend of prioritizing domestic production is also intensifying. For instance, Saudi Arabia has committed to procuring over 50% of its defense spending through domestic defense companies as part of its Vision 2030 initiative. As a result, local production and industrial cooperation are becoming key factors in major projects pursued by domestic defense firms, including Hanwha Aerospace's K9 self-propelled howitzer and Redback, Hyundai Rotem's K2 tank, and LIG Nex1's L-SAM. K-Defense Must Revise Export Strategy The increasing demands for local production and technology transfer in Europe and the Middle East stem from a heightened awareness of defense self-sufficiency following the Russia-Ukraine war. Initially, European countries relied on South Korean weapons due to a lack of production capacity. Quick delivery and reasonable pricing enabled K-Defense to penetrate the European market. However, as the war has prolonged, European nations have recognized the importance of expanding production facilities and establishing joint procurement systems, diminishing the 'gap-filler' role that South Korean defense had previously enjoyed. Choi Gi-il, a professor at Sangji University, stated, "Just a few years ago, European defense companies lacked sufficient production capacity, allowing K-Defense to fill the gaps. However, with Germany and France rapidly recovering their production capabilities, the competitive landscape is changing." Germany, a leading defense power in Europe, is increasing its total defense spending to €108.2 billion (approximately 170 trillion won) this year to enhance its domestic defense production capabilities. France is also expanding its defense investments and production capacity. Experts argue that K-Defense needs to find new breakthroughs to succeed in Europe and the Middle East, emphasizing the need for enhanced local cooperation and cross-industry collaborations. Nam Myung-ryul, head of the K-Defense Center at Korea University, remarked, "We must go beyond merely selling weapons to establishing local production facilities and proposing industrial cooperation models. A package cooperation strategy that links defense with industries where Korea has strengths, such as energy, artificial intelligence, and information and communication technology, is essential." 2026-06-02 16:12:00 -

Korea sees 80% of summer crude secured as Mideast war strains supply SEOUL, June 02 (AJP) - South Korea expects to secure most of the crude oil it needs for August by next month, the energy minister said, seeking to quell fears of a supply crunch as the Middle East war drags into its fourth month. Industry Minister Kim Jung-kwan told a cabinet meeting chaired by President Lee Jae Myung that projected August crude volumes were climbing steadily and would reach the mid-80 percent range of normal levels during July, the 95th day of the conflict. From May to July, the country secured 86 percent of its usual crude and 83 percent of its naphtha, holding a stable course, the minister said. Naphtha plant utilization stood at about 75 percent as of late May, close to the prewar level of 80 percent. "We have already secured replacement volumes to last through the end of this year," Kim said of natural gas supplies, after Qatar's recent declaration of force majeure on liquefied natural gas shipments stirred concern. The government turned to the United States and Southeast Asia to plug the gap. Markets had feared an August squeeze should the blockade of the Strait of Hormuz, a chokehold on Korea's Middle East crude, persist into the peak summer demand season. The International Energy Agency had also warned that supply disruptions and seasonal demand could push the oil market into a danger zone in July and August. With no clear date for safe passage through the strait, the ministry extended its strategic stockpile swap scheme through this month from an earlier April-to-May window. Under the scheme, the government lends out reserve crude once a refiner proves it has sourced oil abroad, then recoups the barrels when replacement cargoes arrive. About 21 million barrels have been swapped and are now being repaid in stages. Supplies of medical materials such as intravenous-fluid packaging, syringes and surgical gloves remained at normal levels, the ministry said, while helium, hydrogen bromide and aluminum wheels feeding the semiconductor, auto and shipbuilding industries showed no signs of disruption. 2026-06-02 16:10:59

Korea sees 80% of summer crude secured as Mideast war strains supply SEOUL, June 02 (AJP) - South Korea expects to secure most of the crude oil it needs for August by next month, the energy minister said, seeking to quell fears of a supply crunch as the Middle East war drags into its fourth month. Industry Minister Kim Jung-kwan told a cabinet meeting chaired by President Lee Jae Myung that projected August crude volumes were climbing steadily and would reach the mid-80 percent range of normal levels during July, the 95th day of the conflict. From May to July, the country secured 86 percent of its usual crude and 83 percent of its naphtha, holding a stable course, the minister said. Naphtha plant utilization stood at about 75 percent as of late May, close to the prewar level of 80 percent. "We have already secured replacement volumes to last through the end of this year," Kim said of natural gas supplies, after Qatar's recent declaration of force majeure on liquefied natural gas shipments stirred concern. The government turned to the United States and Southeast Asia to plug the gap. Markets had feared an August squeeze should the blockade of the Strait of Hormuz, a chokehold on Korea's Middle East crude, persist into the peak summer demand season. The International Energy Agency had also warned that supply disruptions and seasonal demand could push the oil market into a danger zone in July and August. With no clear date for safe passage through the strait, the ministry extended its strategic stockpile swap scheme through this month from an earlier April-to-May window. Under the scheme, the government lends out reserve crude once a refiner proves it has sourced oil abroad, then recoups the barrels when replacement cargoes arrive. About 21 million barrels have been swapped and are now being repaid in stages. Supplies of medical materials such as intravenous-fluid packaging, syringes and surgical gloves remained at normal levels, the ministry said, while helium, hydrogen bromide and aluminum wheels feeding the semiconductor, auto and shipbuilding industries showed no signs of disruption. 2026-06-02 16:10:59 -

OPINION: The Strait of Hormuz Legal Aspects of the New Arrangements in Light of Aggression and Fundamental Change of Circumstances Prelude For a long period, maritime navigation through the Strait of Hormuz did not proceed on the basis of exercising an asserted right, but rather within the framework of an interaction founded upon comity and mutual good faith. Over years, the Islamic Republic of Iran, as the coastal State, facilitated the passage of vessels through a continuous and peaceful practice. However, this practice was never to be understood as an acceptance of a binding legal obligation or as a relinquishment of the coastal State’s sovereignty and sovereign rights over its own waterway. Nevertheless, today, due to a fundamental change of circumstances and the substantial transformation of security, the continuation of such unilateral comity is no longer possible, and the adoption of appropriate measures based on respect for the sovereign rights of the coastal State has become an inevitable necessity. Indeed, the Strait of Hormuz has long been regarded as a sensitive and strategic waterway—a status that has now been redefined in light of the repeated acts of aggression by the Zionist regime, the United States, and certain neighboring States in the region. Some neighboring States, by placing their territory at the disposal of aggressors for commission of acts of aggression against the Islamic Republic of Iran, have become complicit in such aggression. This conduct itself constitutes an act of aggression as defined by General Assembly Resolution 3314 (XXIX) and, consequently, those States have assumed the heavy burden of responsibility for this act, which is a manifest violation of the Charter of the United Nations and the peremptory norm of “prohibition of aggression”. As a result of this aggression and these hostile acts, the security and safety of the region, and in particular of the Strait of Hormuz, have suffered severe and widespread harm. It must not be forgotten that the aggressor and its regional military bases were supplied and equipped, inter alia, through that same strait. Therefore, preventing the recurrence of such internationally wrongful acts is an undeniable imperative. In the wake of the intensification of such acts, the circumstances have fundamentally changed, giving rise to a new and irreversible situation. In this situation, the Government of the Islamic Republic of Iran, as the coastal State, finds itself compelled to adopt practical and proportionate measures to manage the developments that have expanded into the maritime zones. These measures are taken with a view to preventing further risks from being imposed on vessels and seafarers in the Persian Gulf, the Strait of Hormuz, and the Gulf of Oman. Fundamental Change of Circumstances Since the commencement of acts of aggression against the Islamic Republic of Iran, the security environment of the Persian Gulf and the Strait of Hormuz has undergone significant transformations and has thereby become subject to a fundamental change of circumstances. In the current situation, the underlying circumstances governing the legal regime of the Strait, namely the existence of a minimum level of regional stability and security necessary to guarantee safe passage, have been severely undermined as a result of repeated threats and actions that violate Article 2 (4) of the Charter of the United Nations. One of the most significant factors that has disrupted the prior order is the persistent disregard for a peremptory norm of international law: the norm that prohibits any act of aggression. In addition to this, despite repeated violations of international law, the United Nations Security Council, as the primary body responsible for the maintenance of international peace and security, has remained practically incapable of condemning the aggressor and has consequently failed to discharge its primary responsibility to ensure international peace and security and to restore stability to the region. Accordingly, under the international law of the sea, the regime of passage through straits used for international navigation cannot be applied in a security vacuum. The coastal State’s obligation to facilitate passage is conditional upon the existence of circumstances in which the safety of navigation and maritime public order have not been seriously disrupted. In a situation where persistent military threats pose real dangers and transform the operational environment, the adoption of necessary measures based on the doctrine of fundamental change of circumstances is unavoidable. On this basis, the set of current measures and practices must be regarded as an adjustment of rights and obligations to adapt to the circumstances, in light of the fundamental change of circumstances, measures undertaken with the aim of establishing a balance between the security requirements of the coastal State and the continued safe passage of international navigation. Sovereignty over the territorial sea Under the international law of the sea, the sovereignty of coastal States over their territorial sea, including over that part which lies within an international strait, and the exercise of rights and jurisdiction derived from such sovereignty, constitutes a fundamental and well-established principle. Consequently, the arrangements for managing passage through the Strait of Hormuz are governed within the framework of the domestic laws of Iran and Oman, as well as customary and treaty-based rules and principles, including the 1958 Geneva Conventions, the relevant provisions of the 1982 United Nations Convention on the Law of the Sea, the principles of the Charter of the United Nations, and international judicial precedents (including the judgments of the International Court of Justice in the Corfu Channel and Oil Platforms cases). Within this framework, one essential principle is of particular importance: no right under international law, including the right of passage, may be exercised in such a way as to result in a threat, military aggression, or violation of the security of the coastal State. Accordingly, mere reliance on classical concepts is insufficient to address the exigencies of the current unprecedented situation and does not adequately meet the requirements of security and sovereignty. This situation is also premised upon the peremptory norm prohibiting the threat or use of force, as embodied in Article 2(4) of the Charter of the United Nations and recognized in international judicial precedents and the judgments of the International Court of Justice as an intransgressible rule. In the case concerning Military and Paramilitary Activities in and against Nicaragua (Nicaragua v. United States of America), the findings of the International Court of Justice clearly indicate that any foreign military presence or action that endangers the security or sovereignty of another State, even indirectly, is contrary to that principle. Furthermore, Article 2 of the 1982 United Nations Convention on the Law of the Sea affirms the sovereignty of the coastal State over its territorial sea, seabed, and subsoil, and grants no authorization for the stationing of foreign forces. Article 30 of the same Convention confirms the right to require any military ship that fails to comply with the laws and regulations of the coastal State to leave the territorial sea immediately. Moreover, the San Remo Manual on International Law Applicable to Armed Conflicts at Sea emphasizes the right of coastal States to restrict foreign military presence in order to preserve the neutrality of regional States and the security of the waterway. While preventing the reproduction of aggressive and interventionist patterns that have led to instability and insecurity, this approach establishes a balance between the freedom of navigation and the security rights of the coastal State as affirmed in established international judicial practice. Historic sovereignty over the Strait of Hormuz In formulating the arrangements for managing passage through the Strait of Hormuz, it is essential to emphasize the historic sovereignty of Iran and Oman over this waterway. This finding has been affirmed by various arbitral tribunals. Accordingly, the longstanding historic sovereignty of Iran over the Strait of Hormuz, which existed for centuries prior to the Convention and has been continuously exercised, remains valid. In the case of Qatar v. Bahrain, the International Court of Justice, upon examining historic rights in the Persian Gulf, took the view that the continuous exercise of sovereignty and historical activities by coastal States constitutes a valid basis for the recognition of a “historic title” over maritime areas. Given the similar geographic and historical situation of the Strait of Hormuz, this judicial precedent directly confirms the historic sovereignty of Iran and Oman over the strait. Both the 1958 Geneva Convention on the Territorial Sea and the Contiguous Zone and the 1982 United Nations Convention on the Law of the Sea recognize the full sovereignty of the coastal State over its territorial sea and preserve the historic rights of coastal States in gulfs and semi-enclosed waterways. Therefore, in light of the continuous and historic exercise of sovereignty by Iran and Oman over the Strait of Hormuz over many centuries, this strait possesses a historic title. Hierarchy of applicable rules In this regard, the rules governing this matter must be examined at three distinct but interrelated levels, given that each level possesses a higher rank and a more fundamental character, and rules at lower levels cannot be interpreted or applied in conflict with the principles of higher levels. The first level relates to the fundamental principles of international law, including peremptory norms (jus cogens), that is the prohibition of aggression, and those enshrined in the United Nations Charter including prohibition of threat or use of force (Article 2(4)) and the inherent right of self-defence (Article 51). These principles stand at the apex of the hierarchy of international legal norms and establish the framework and limitations for all other rules. The second level refers to international humanitarian law (the law of armed conflict), which governs conduct in armed hostilities and determines which conducts are permissible and which are prohibited in situations of armed conflict. This level of rules complements in hierarchical manner, the fundamental principles of the first level. At the third level, the law of the sea applies as a specialized body of law. The rules governing the regimes of passage through international straits, the rights of coastal States over their territorial sea, and other provisions of the 1982 United Nations Convention on the Law of the Sea cannot be applied in a vacuum or by disregarding the higher levels. In other words, the law of the sea must not be analyzed separately from the “root causes” that have shaped the current situation (including aggression, continuous military threats, and the inability of the Security Council to maintain peace), nor separately from the fundamental principles of international law; otherwise, this branch of law would become a tool for justifying aggression and disregarding the sovereign rights of coastal States. With respect to the third level, it must be noted that the Islamic Republic of Iran has not acceded to the 1958 Convention on the Territorial Sea and the Contiguous Zone, nor to the United Nations Convention on the Law of the Sea (UNCLOS). Therefore, Iran is not bound by their provisions, except insofar as they have become part of customary international law. The regime of “transit passage” set forth in the 1982 Convention does not meet the established criteria of customary international law. The conclusions of the International Law Commission’s 2018 work on the identification of customary international law contain key elements generally considered for determining whether a practice has become customary. Two of these conclusions are particularly relevant: first, under Conclusion 5, “State practice consists of conduct of the State, whether in the exercise of its executive, legislative, judicial or other functions”. Second, Conclusion 15 provides that “Where a State has objected to a rule of customary international law while that rule was in the process of formation, the rule is not opposable to the State concerned for so long as it maintains its objection”. Through its continuous and persistent objection to the regime of “transit passage” provided for in Articles 37 to 44 of the 1982 Convention, Iran has not recognized these rules as binding under customary international law. In this regard, Iran’s consistent legislative and diplomatic practice since 1982 has established its position as a persistent objector to the binding nature of these rules and has challenged the opinio juris necessary for the formation of a customary norm. The first notable document registered in the United Nations Treaty Series is Iran’s interpretative declaration made at the time of signing the Convention, in which it explicitly stated that certain provisions, including the regime of “transit passage” in Part III (Articles 37 to 44), do not represent established customary international law. Iran’s Maritime Law of 1963 (1342), its 2012 (1391) amendment, and Iran’s Law on Maritime Zones of the Persian Gulf and the Gulf of Oman of 1993 (1372) are further evidence of this practice. The latter law makes no reference to transit passage and thus does not recognize that regime; rather, it establishes specific regulatory provisions for the strait, including the requirement to obtain prior authorization for the passage of warships, submarines, and vessels carrying dangerous or environmentally harmful substances. Consequently, the applicable legal framework for passage through the Strait of Hormuz, in the absence of a binding treaty obligation and in the absence of a customary rule of “transit passage”, is the customary right of “innocent passage” through straits used for international navigation, as recognized by the International Court of Justice in the Corfu Channel case (1949). Within this framework, the coastal State has the right to regulate passage, collect fees for maritime services, require prior notification or authorization for the passage of warships, and adopt necessary measures for the protection of its security. The measures taken by the Islamic Republic of Iran are consistent with this customary framework. Accordingly, any legal analysis of the situation in the Strait of Hormuz that proceeds directly to the specific provisions of the law of the sea without first examining peremptory norms, the fundamental principles of the Charter, and international humanitarian law is not only incomplete but also misleading. The law of the sea does not operate in a vacuum and cannot be used as a shield to justify aggression, extra-regional military presence, or the disregard of the historic and contemporary sovereign rights of coastal States. 2026-06-02 16:10:44