Journalist

Son Ji-ae

-

The Rise of Mobile Payments: A Shift in Financial Transactions Mobile payments are rapidly replacing cash and physical cards, becoming the central method for everyday transactions. As their use expands across online shopping, brick-and-mortar stores, and money transfers, experts say they are transforming overall financial consumer behavior. According to the financial sector, the average daily usage of mobile payment services last year reached 35.57 million transactions, totaling 1.1053 trillion won. This marks increases of 14.9% and 14.6%, respectively, from the previous year. Mobile payment services utilize biometric authentication methods such as fingerprints and facial recognition to process transactions. The average daily usage and amount for mobile remittance services also saw increases of 2.9% and 7.3%, reaching 7.42 million transactions and 978.5 billion won. Notably, the transaction amounts for electronic financial service providers like Naver Pay, Kakao Pay, and Toss Pay surged by 24.6%, totaling 606.41 billion won compared to 486.85 billion won the previous year. Prepaid balances within mobile payment platforms are also growing rapidly. As of the end of the first quarter of this year, the combined prepaid balance for Naver Pay, Kakao Pay, and Toss Pay reached 990.2 billion won, an 11.5% increase from 888.1 billion won during the same period last year. This increase indicates a shift beyond simple payment functions, as more funds are being retained and utilized within the platforms. Big tech companies like Naver, Kakao, and Toss are leveraging user data obtained through mobile payments to expand into broader financial services, including loans, investments, and insurance. Data accumulated during transactions, such as spending patterns and frequency of use, can be utilized for personalized financial product recommendations and enhanced credit evaluations. Industry analysts suggest that the payment features used daily by consumers are crucial touchpoints that increase platform engagement and encourage connections to other financial services. They predict that effectively linking payment data to financial services will be key to future platform competitiveness. In response to the diminishing presence of physical cards, card companies are accelerating their digital transformation and enhancing mobile payment services. Last year, the average daily transaction volume for physical cards fell by 0.4% to 1.4 trillion won, marking a decline for the second consecutive year. In contrast, non-physical card transactions using mobile devices increased by 7.3% to 1.7 trillion won. Card companies are not only strengthening their own app-based mobile payment features but also expanding integrations with external platforms like Apple Pay and Samsung Wallet. Major card issuers, including Shinhan Card and KB Kookmin Card, are focusing on enhancing their apps while integrating various services such as asset management, loans, and membership programs to boost platform competitiveness. Some card companies are enhancing user convenience by expanding features like asset tracking and benefit recommendations within their apps. They are also strengthening contactless payment services based on NFC and QR codes to adapt to the shift toward mobile-centric payment environments. The structure of card benefits is also being restructured around digital consumption patterns. There is ongoing competition to attract customers by enhancing discounts and rewards tailored to online shopping, delivery apps, streaming services, and mobile payment usage. Industry experts believe that future competition in the payment market will extend beyond simple fee collection to a battle for data and platform dominance. The ability to connect payment services with a diverse range of financial services is emerging as a critical factor in determining market competitiveness. An industry insider stated, "After successfully establishing mobile payment systems in the e-commerce market, mobile payment providers are now venturing into offline spaces to secure more merchants and users. The convenience already provided by online mobile payment services will be complemented by monetary benefits, while offline will focus on enhancing payment convenience as a key competitive advantage." 2026-05-13 17:15:41

The Rise of Mobile Payments: A Shift in Financial Transactions Mobile payments are rapidly replacing cash and physical cards, becoming the central method for everyday transactions. As their use expands across online shopping, brick-and-mortar stores, and money transfers, experts say they are transforming overall financial consumer behavior. According to the financial sector, the average daily usage of mobile payment services last year reached 35.57 million transactions, totaling 1.1053 trillion won. This marks increases of 14.9% and 14.6%, respectively, from the previous year. Mobile payment services utilize biometric authentication methods such as fingerprints and facial recognition to process transactions. The average daily usage and amount for mobile remittance services also saw increases of 2.9% and 7.3%, reaching 7.42 million transactions and 978.5 billion won. Notably, the transaction amounts for electronic financial service providers like Naver Pay, Kakao Pay, and Toss Pay surged by 24.6%, totaling 606.41 billion won compared to 486.85 billion won the previous year. Prepaid balances within mobile payment platforms are also growing rapidly. As of the end of the first quarter of this year, the combined prepaid balance for Naver Pay, Kakao Pay, and Toss Pay reached 990.2 billion won, an 11.5% increase from 888.1 billion won during the same period last year. This increase indicates a shift beyond simple payment functions, as more funds are being retained and utilized within the platforms. Big tech companies like Naver, Kakao, and Toss are leveraging user data obtained through mobile payments to expand into broader financial services, including loans, investments, and insurance. Data accumulated during transactions, such as spending patterns and frequency of use, can be utilized for personalized financial product recommendations and enhanced credit evaluations. Industry analysts suggest that the payment features used daily by consumers are crucial touchpoints that increase platform engagement and encourage connections to other financial services. They predict that effectively linking payment data to financial services will be key to future platform competitiveness. In response to the diminishing presence of physical cards, card companies are accelerating their digital transformation and enhancing mobile payment services. Last year, the average daily transaction volume for physical cards fell by 0.4% to 1.4 trillion won, marking a decline for the second consecutive year. In contrast, non-physical card transactions using mobile devices increased by 7.3% to 1.7 trillion won. Card companies are not only strengthening their own app-based mobile payment features but also expanding integrations with external platforms like Apple Pay and Samsung Wallet. Major card issuers, including Shinhan Card and KB Kookmin Card, are focusing on enhancing their apps while integrating various services such as asset management, loans, and membership programs to boost platform competitiveness. Some card companies are enhancing user convenience by expanding features like asset tracking and benefit recommendations within their apps. They are also strengthening contactless payment services based on NFC and QR codes to adapt to the shift toward mobile-centric payment environments. The structure of card benefits is also being restructured around digital consumption patterns. There is ongoing competition to attract customers by enhancing discounts and rewards tailored to online shopping, delivery apps, streaming services, and mobile payment usage. Industry experts believe that future competition in the payment market will extend beyond simple fee collection to a battle for data and platform dominance. The ability to connect payment services with a diverse range of financial services is emerging as a critical factor in determining market competitiveness. An industry insider stated, "After successfully establishing mobile payment systems in the e-commerce market, mobile payment providers are now venturing into offline spaces to secure more merchants and users. The convenience already provided by online mobile payment services will be complemented by monetary benefits, while offline will focus on enhancing payment convenience as a key competitive advantage." 2026-05-13 17:15:41 -

NH Nonghyup Bank Accelerates Digitalization with NH Pay NH Nonghyup Bank is advancing the digitalization of everyday life through its NH Pay service. NH Pay has launched a convenient payment service linked to both Nonghyup Bank accounts and agricultural cooperative accounts. When linked, payment amounts are settled directly from the bank account. The bank has revamped its existing app infrastructure to allow NH Pay to be used seamlessly across various apps from its affiliated companies. A notable example is the integration of the Nonghyup Card and NH Pay into a single mobile application. This integration is based on cloud technology, and a new integrated spending analysis service will be created by linking NH MyData. This aims to enhance the versatility of NH Pay, according to NH Nonghyup Bank. The bank is particularly focused on intuitively changing the app's user environment based on user behavior patterns. This approach is designed to reduce the time consumers spend navigating the app and to improve overall usability. NH Nonghyup Bank has a strong presence in rural areas across the country, particularly in agricultural regions, and has established a significant market share that other financial institutions do not possess. As NH Pay expands across all affiliates, it is expected to attract a more diverse customer base. Additionally, NH Pay is expanding its business by offering overseas payment services. Customers who register their UnionPay cards with NH Pay can easily make payments at local UnionPay merchants abroad.* This article has been translated by AI. 2026-05-13 17:15:00

NH Nonghyup Bank Accelerates Digitalization with NH Pay NH Nonghyup Bank is advancing the digitalization of everyday life through its NH Pay service. NH Pay has launched a convenient payment service linked to both Nonghyup Bank accounts and agricultural cooperative accounts. When linked, payment amounts are settled directly from the bank account. The bank has revamped its existing app infrastructure to allow NH Pay to be used seamlessly across various apps from its affiliated companies. A notable example is the integration of the Nonghyup Card and NH Pay into a single mobile application. This integration is based on cloud technology, and a new integrated spending analysis service will be created by linking NH MyData. This aims to enhance the versatility of NH Pay, according to NH Nonghyup Bank. The bank is particularly focused on intuitively changing the app's user environment based on user behavior patterns. This approach is designed to reduce the time consumers spend navigating the app and to improve overall usability. NH Nonghyup Bank has a strong presence in rural areas across the country, particularly in agricultural regions, and has established a significant market share that other financial institutions do not possess. As NH Pay expands across all affiliates, it is expected to attract a more diverse customer base. Additionally, NH Pay is expanding its business by offering overseas payment services. Customers who register their UnionPay cards with NH Pay can easily make payments at local UnionPay merchants abroad.* This article has been translated by AI. 2026-05-13 17:15:00 -

KOSPI flies to new highs after Lee clarifies controversial 'AI dividend' slip SEOUL, May 13 (AJP) - South Korea’s benchmark KOSPI returned to record-setting climb Wednesday after President Lee Jae Myung moved to calm investor concerns over controversial remarks by his top policy aide suggesting that gains from the country’s AI boom could be redistributed more broadly to the public. In a post on X on Wednesday, Lee accused some media outlets of distorting comments made by presidential policy chief Kim Yong-beom regarding a proposed “national dividend” linked to the artificial intelligence boom. Lee said Kim’s remarks referred to the possible redistribution of excess tax revenue generated from extraordinary profits in the AI sector — not the direct redistribution of corporate profits themselves. “What Kim Yong-beom referred to was a review of ways to distribute to the public part of the government’s excess tax revenue generated from extraordinary profits in the AI sector,” Lee wrote. Lee added that Kim had already clarified the proposal concerned excess tax revenue rather than corporate earnings, but “misleading reports” continued circulating despite follow-up explanations. “Political criticism and attacks that are not based on facts ultimately harm democracy,” Lee said. The clarification helped ease fears of possible government intervention in corporate earnings tied to South Korea’s booming semiconductor and AI sectors, which have driven much of the market’s recent rally. The KOSPI erased earlier losses and gained 2.63 percent to a new closing high 7,844.01. Chipmakers also renewed bull march, with Samsung Electronics rising 1.79 percent to 284,000 won and SK hynix surging 7.68 percent to 1,976,000 won. 2026-05-13 17:14:46

KOSPI flies to new highs after Lee clarifies controversial 'AI dividend' slip SEOUL, May 13 (AJP) - South Korea’s benchmark KOSPI returned to record-setting climb Wednesday after President Lee Jae Myung moved to calm investor concerns over controversial remarks by his top policy aide suggesting that gains from the country’s AI boom could be redistributed more broadly to the public. In a post on X on Wednesday, Lee accused some media outlets of distorting comments made by presidential policy chief Kim Yong-beom regarding a proposed “national dividend” linked to the artificial intelligence boom. Lee said Kim’s remarks referred to the possible redistribution of excess tax revenue generated from extraordinary profits in the AI sector — not the direct redistribution of corporate profits themselves. “What Kim Yong-beom referred to was a review of ways to distribute to the public part of the government’s excess tax revenue generated from extraordinary profits in the AI sector,” Lee wrote. Lee added that Kim had already clarified the proposal concerned excess tax revenue rather than corporate earnings, but “misleading reports” continued circulating despite follow-up explanations. “Political criticism and attacks that are not based on facts ultimately harm democracy,” Lee said. The clarification helped ease fears of possible government intervention in corporate earnings tied to South Korea’s booming semiconductor and AI sectors, which have driven much of the market’s recent rally. The KOSPI erased earlier losses and gained 2.63 percent to a new closing high 7,844.01. Chipmakers also renewed bull march, with Samsung Electronics rising 1.79 percent to 284,000 won and SK hynix surging 7.68 percent to 1,976,000 won. 2026-05-13 17:14:46 -

K-Bank Launches Lottery Ticket Sales with Easy Recharge Service K-Bank is entering the lottery ticket sales market by utilizing its easy recharge service, making it the only bank to offer such a service. K-Bank has partnered with Donghaeng Lottery to introduce a convenient recharge service that allows customers to quickly and easily top up their deposits for online lottery purchases. The easy recharge service enables customers to fund their K-Bank accounts with the desired deposit amount and recharge their accounts with just one click when purchasing lottery tickets, such as Lotto and Pension Lottery, on the Donghaeng Lottery website. Previously, customers had to create a virtual account after mobile authentication and deposit funds into that account to recharge their deposits. Now, customers can simply keep the amount they wish to recharge in their K-Bank account and recharge it instantly with a single click, without any additional procedures. Since February of this year, customers can also purchase Donghaeng Lottery tickets through mobile platforms, expanding access beyond online sales. The scale of online lottery sales is capped at 5% of the previous year's sales. This year, the online purchase limit for Lotto is approximately 380 billion won, which is expected to benefit K-Bank significantly. K-Bank is also expanding its payment services through collaborations with payment companies. Customers can register their K-Bank debit cards with Naver Pay and earn rewards when making purchases above a certain amount at Naver Pay merchants. Additionally, K-Bank has launched K-Bank Pay and a dedicated loan service called Shopping Money Loan. K-Bank Pay is a payment service based on account transfers using QR codes and barcodes. It can be used at all offline Zero Pay merchants and, unlike Zero Pay, is also available for online merchants.* This article has been translated by AI. 2026-05-13 17:12:25

K-Bank Launches Lottery Ticket Sales with Easy Recharge Service K-Bank is entering the lottery ticket sales market by utilizing its easy recharge service, making it the only bank to offer such a service. K-Bank has partnered with Donghaeng Lottery to introduce a convenient recharge service that allows customers to quickly and easily top up their deposits for online lottery purchases. The easy recharge service enables customers to fund their K-Bank accounts with the desired deposit amount and recharge their accounts with just one click when purchasing lottery tickets, such as Lotto and Pension Lottery, on the Donghaeng Lottery website. Previously, customers had to create a virtual account after mobile authentication and deposit funds into that account to recharge their deposits. Now, customers can simply keep the amount they wish to recharge in their K-Bank account and recharge it instantly with a single click, without any additional procedures. Since February of this year, customers can also purchase Donghaeng Lottery tickets through mobile platforms, expanding access beyond online sales. The scale of online lottery sales is capped at 5% of the previous year's sales. This year, the online purchase limit for Lotto is approximately 380 billion won, which is expected to benefit K-Bank significantly. K-Bank is also expanding its payment services through collaborations with payment companies. Customers can register their K-Bank debit cards with Naver Pay and earn rewards when making purchases above a certain amount at Naver Pay merchants. Additionally, K-Bank has launched K-Bank Pay and a dedicated loan service called Shopping Money Loan. K-Bank Pay is a payment service based on account transfers using QR codes and barcodes. It can be used at all offline Zero Pay merchants and, unlike Zero Pay, is also available for online merchants.* This article has been translated by AI. 2026-05-13 17:12:25 -

Toss's FacePay Surpasses 4.83 Million Users as Offline Payments Expand Viva Republica, the company behind Toss, is accelerating its expansion in the offline payment market with its facial recognition payment service, FacePay. The company is moving beyond simple payment solutions by designing its own terminals, POS systems, and payment infrastructure to create an integrated online and offline payment ecosystem. As of the end of last month, Toss announced that FacePay has reached 4.83 million subscribers. There are now 330,000 offline merchants that accept FacePay. FacePay is a facial recognition-based payment service that allows users to authenticate and approve payments with a single glance, eliminating the need to pull out a card or smartphone. Toss is the only domestic payment service provider to have passed the preliminary review by the Personal Information Protection Commission for its facial recognition payment technology. The company highlights its compliance in the processing, storage, and utilization of biometric data as a key differentiator. The company is also implementing a strategy to build its payment infrastructure by linking its subsidiary Toss Place's terminals with Toss Payments' PG services. Unlike other payment providers that have primarily focused on online growth, Toss has integrated offline payment experiences into its design. A reduction in merchant burdens is also cited as a factor in the service's expansion. Merchants already using Toss terminals can activate FacePay without needing to replace their devices, and no additional fees are charged. Looking ahead, Toss plans to expand FacePay into unmanned stores, late-night shops, and single-operator establishments to enhance both payment convenience and operational efficiency.* This article has been translated by AI. 2026-05-13 17:11:59

Toss's FacePay Surpasses 4.83 Million Users as Offline Payments Expand Viva Republica, the company behind Toss, is accelerating its expansion in the offline payment market with its facial recognition payment service, FacePay. The company is moving beyond simple payment solutions by designing its own terminals, POS systems, and payment infrastructure to create an integrated online and offline payment ecosystem. As of the end of last month, Toss announced that FacePay has reached 4.83 million subscribers. There are now 330,000 offline merchants that accept FacePay. FacePay is a facial recognition-based payment service that allows users to authenticate and approve payments with a single glance, eliminating the need to pull out a card or smartphone. Toss is the only domestic payment service provider to have passed the preliminary review by the Personal Information Protection Commission for its facial recognition payment technology. The company highlights its compliance in the processing, storage, and utilization of biometric data as a key differentiator. The company is also implementing a strategy to build its payment infrastructure by linking its subsidiary Toss Place's terminals with Toss Payments' PG services. Unlike other payment providers that have primarily focused on online growth, Toss has integrated offline payment experiences into its design. A reduction in merchant burdens is also cited as a factor in the service's expansion. Merchants already using Toss terminals can activate FacePay without needing to replace their devices, and no additional fees are charged. Looking ahead, Toss plans to expand FacePay into unmanned stores, late-night shops, and single-operator establishments to enhance both payment convenience and operational efficiency.* This article has been translated by AI. 2026-05-13 17:11:59 -

Woori Bank and Samsung Wallet Money Surpass 2 Million Users in Six Months Woori Bank, in partnership with Samsung Electronics, announced that its Samsung Wallet Money service has exceeded 2 million new users within six months of its launch. The service differentiates itself from existing payment options by allowing users to make online and offline transactions using only their smartphones, as well as offering ATM withdrawals and money transfer capabilities. Samsung Wallet Money is automatically registered in the Samsung Wallet, enabling payments with just a smartphone tap without needing to open a separate app. Unlike some payment services that only work at QR code merchants, it can be used at regular card merchant locations, utilizing existing card payment infrastructure without requiring additional devices. The registration process has also been simplified. Users can sign up with just a mobile phone verification, and those aged 14 and older can directly recharge and make payments. The integration with Samsung Wallet, a standard service on Samsung smartphones, enhances accessibility by eliminating the need for a separate app installation. Recently, the service introduced a mobile transit card top-up feature to improve convenience. Users of Samsung Wallet Money can recharge their T-money mobile transit card balance without fees through an update to the Samsung Wallet app. Additionally, a top-up service for the Izle (formerly Cashbee) mobile transit card is in development, aiming for a launch in early the third quarter of this year. "Beyond simply expanding payment methods, the significance of Samsung Wallet Money lies in enhancing financial convenience in daily life," said Heo Min-woo, a manager in Woori Bank's platform business division. "We will continue to provide a broad financial experience for all customer segments."* This article has been translated by AI. 2026-05-13 17:11:14

Woori Bank and Samsung Wallet Money Surpass 2 Million Users in Six Months Woori Bank, in partnership with Samsung Electronics, announced that its Samsung Wallet Money service has exceeded 2 million new users within six months of its launch. The service differentiates itself from existing payment options by allowing users to make online and offline transactions using only their smartphones, as well as offering ATM withdrawals and money transfer capabilities. Samsung Wallet Money is automatically registered in the Samsung Wallet, enabling payments with just a smartphone tap without needing to open a separate app. Unlike some payment services that only work at QR code merchants, it can be used at regular card merchant locations, utilizing existing card payment infrastructure without requiring additional devices. The registration process has also been simplified. Users can sign up with just a mobile phone verification, and those aged 14 and older can directly recharge and make payments. The integration with Samsung Wallet, a standard service on Samsung smartphones, enhances accessibility by eliminating the need for a separate app installation. Recently, the service introduced a mobile transit card top-up feature to improve convenience. Users of Samsung Wallet Money can recharge their T-money mobile transit card balance without fees through an update to the Samsung Wallet app. Additionally, a top-up service for the Izle (formerly Cashbee) mobile transit card is in development, aiming for a launch in early the third quarter of this year. "Beyond simply expanding payment methods, the significance of Samsung Wallet Money lies in enhancing financial convenience in daily life," said Heo Min-woo, a manager in Woori Bank's platform business division. "We will continue to provide a broad financial experience for all customer segments."* This article has been translated by AI. 2026-05-13 17:11:14 -

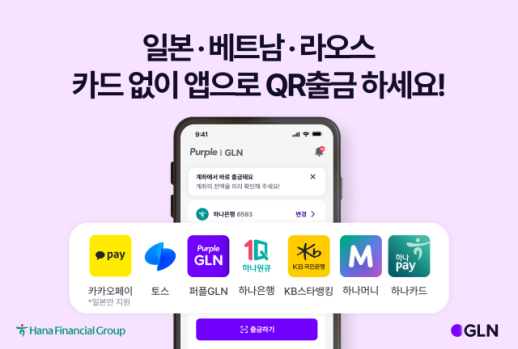

Hana Bank's GLN Expands Overseas QR Withdrawal Partnerships, Enabling Cash Withdrawals via KakaoPay in Japan Hana Bank's subsidiary, GLN International, is expanding its overseas QR withdrawal service in Japan, Vietnam, and Laos. This enhancement allows users of major domestic financial and platform apps to withdraw local currency without the need for currency exchange. The expansion focuses on the Japanese market, increasing the number of partner app channels from three to seven. Notably, KakaoPay, which enjoys high usage rates in Japan's mobile payment sector, has been added to the list of domestic partner apps. As a result, travelers to Japan can now access QR withdrawal services through not only Hana OneQ, Hana Money, and Toss apps but also Hana Pay, KakaoPay, Purple GLN, and KB Star Banking apps. Withdrawals can be made at Seven-Eleven convenience store ATMs and Seven Bank ATMs located in airports throughout Japan. QR payments are also accepted at various merchants, including convenience stores, clothing shops, and health and beauty stores. In Vietnam and Laos, users can access QR withdrawal services through six apps: Hana OneQ, Hana Money, Hana Pay, Toss, Purple GLN, and KB Star Banking. In Vietnam, local currency can be withdrawn at BIDV Bank ATMs, while in Laos, withdrawals can be made at BCEL Bank ATMs. Lee Seok, CEO of GLN, stated, "With the expansion of the QR withdrawal service in Japan, Vietnam, and Laos, more customers can enjoy cash withdrawal services abroad using familiar domestic apps without inconvenience. We will continue to lead the way in providing a simple withdrawal experience for travelers without the need for currency exchange or physical cards."* This article has been translated by AI. 2026-05-13 17:11:01

Hana Bank's GLN Expands Overseas QR Withdrawal Partnerships, Enabling Cash Withdrawals via KakaoPay in Japan Hana Bank's subsidiary, GLN International, is expanding its overseas QR withdrawal service in Japan, Vietnam, and Laos. This enhancement allows users of major domestic financial and platform apps to withdraw local currency without the need for currency exchange. The expansion focuses on the Japanese market, increasing the number of partner app channels from three to seven. Notably, KakaoPay, which enjoys high usage rates in Japan's mobile payment sector, has been added to the list of domestic partner apps. As a result, travelers to Japan can now access QR withdrawal services through not only Hana OneQ, Hana Money, and Toss apps but also Hana Pay, KakaoPay, Purple GLN, and KB Star Banking apps. Withdrawals can be made at Seven-Eleven convenience store ATMs and Seven Bank ATMs located in airports throughout Japan. QR payments are also accepted at various merchants, including convenience stores, clothing shops, and health and beauty stores. In Vietnam and Laos, users can access QR withdrawal services through six apps: Hana OneQ, Hana Money, Hana Pay, Toss, Purple GLN, and KB Star Banking. In Vietnam, local currency can be withdrawn at BIDV Bank ATMs, while in Laos, withdrawals can be made at BCEL Bank ATMs. Lee Seok, CEO of GLN, stated, "With the expansion of the QR withdrawal service in Japan, Vietnam, and Laos, more customers can enjoy cash withdrawal services abroad using familiar domestic apps without inconvenience. We will continue to lead the way in providing a simple withdrawal experience for travelers without the need for currency exchange or physical cards."* This article has been translated by AI. 2026-05-13 17:11:01 -

BC Card's Paybook Grows to 15 Million Users as a Lifestyle Finance Platform BC Card's lifestyle finance platform, Paybook, is expanding its customer reach by focusing on convenient payment options and lifestyle-oriented app technology services. As of this month, BC Card reports that Paybook has accumulated approximately 15 million members. The monthly active user count for the first quarter of this year has also increased by over 16% compared to the same period last year. The user demographic is diverse, spanning not only those in their 20s and 30s but also individuals aged 40 and above, indicating its growth as an all-age platform. Paybook allows users to manage card products issued by over 40 BC Card partner companies within a single app. Users can make QR code payments at various offline and online merchants, including convenience stores, cafes, and supermarkets, without needing a physical card, simply by linking their bank accounts. The platform has also enhanced its convenience features. Users can register mobile vouchers within the app and connect their frequently used brand memberships for easy point accumulation by simply presenting a barcode. Recently, Paybook has expanded its app technology features aimed at helping users save on living expenses. The 'MyTag' service allows customers to select desired brand or industry benefits and receive discounts when paying with BC Card. The 'Shopping Rewards' feature provides additional points when shopping at major online retailers like Coupang and Ali. Additionally, the 'AI Hot Deal' service recommends special offers and discounts based on customer spending patterns. Paybook also offers a spare change investment service that collects change from card payments to invest in domestic and international stocks, along with an AI-based robo-advisor investment service.* This article has been translated by AI. 2026-05-13 17:10:14

BC Card's Paybook Grows to 15 Million Users as a Lifestyle Finance Platform BC Card's lifestyle finance platform, Paybook, is expanding its customer reach by focusing on convenient payment options and lifestyle-oriented app technology services. As of this month, BC Card reports that Paybook has accumulated approximately 15 million members. The monthly active user count for the first quarter of this year has also increased by over 16% compared to the same period last year. The user demographic is diverse, spanning not only those in their 20s and 30s but also individuals aged 40 and above, indicating its growth as an all-age platform. Paybook allows users to manage card products issued by over 40 BC Card partner companies within a single app. Users can make QR code payments at various offline and online merchants, including convenience stores, cafes, and supermarkets, without needing a physical card, simply by linking their bank accounts. The platform has also enhanced its convenience features. Users can register mobile vouchers within the app and connect their frequently used brand memberships for easy point accumulation by simply presenting a barcode. Recently, Paybook has expanded its app technology features aimed at helping users save on living expenses. The 'MyTag' service allows customers to select desired brand or industry benefits and receive discounts when paying with BC Card. The 'Shopping Rewards' feature provides additional points when shopping at major online retailers like Coupang and Ali. Additionally, the 'AI Hot Deal' service recommends special offers and discounts based on customer spending patterns. Paybook also offers a spare change investment service that collects change from card payments to invest in domestic and international stocks, along with an AI-based robo-advisor investment service.* This article has been translated by AI. 2026-05-13 17:10:14 -

The Evolving Landscape of Payment Methods: Competition Intensifies in Offline Transactions The competition in the mobile payment market is shifting from securing app users to establishing dominance in offline payment infrastructure. As the mobile app market reaches saturation, the battle for control over payment terminals and networks is intensifying.According to a report released in January by global market research firm Mordor Intelligence, near-field communication (NFC) payment methods accounted for 54.2% of South Korea's mobile payment market last year.As a result, the penetration rate of NFC terminals in South Korea is expected to have increased significantly this year. The country's card payment infrastructure has primarily been built around magnetic secure transmission (MST) and integrated circuit (IC) terminals. Even after the introduction of Apple Pay, NFC-based payments remained at around 10% as of the end of last year.Recently, major tech companies Naver Pay and Toss have ramped up their competition to distribute their own NFC terminals. Toss is leading the charge, expanding its reach through its subsidiary Toss Place, which has been distributing the smart terminal Toss Front since 2023. As of April, the number of Toss Front installations surpassed 330,000. Initially focused on popular areas in Seoul, such as Seongsu and Hongdae, the infrastructure is now expanding to traditional markets and regions outside the metropolitan area.Naver Pay, a latecomer in the offline market, is accelerating its efforts. Its smart terminal, Npay Connect, launched in November, supports card payments, mobile payments, QR codes, and facial recognition payment service Face Sign. The company is employing a two-track strategy targeting both small businesses and franchises. A Naver Pay representative stated, "While we cannot disclose specific distribution figures, we believe we have exceeded our internal targets within five months of launch," adding that they are also working to introduce terminals at Paris Baguette in the second half of the year, which will increase availability in offline stores.Kakao Pay is focusing on expanding its QR-based payment network rather than distributing its own terminals. The company has opted to collaborate with existing point-of-sale (POS) and value-added network (VAN) providers instead of building its own hardware. A Kakao Pay representative emphasized, "The key is not to own the terminals but to enable Kakao Pay transactions anywhere," noting that they are expanding offline touchpoints through QR orders, kiosk payments, and international QR payments.Industry experts believe that control over offline payment data will be a crucial factor in determining the future success of the mobile payment market. As mobile payments expand beyond online transactions into the offline consumer landscape, companies that secure payment infrastructure can achieve both user lock-in effects and data competitiveness.Jeong Yu-shin, a professor at Sogang University's Business School, stated, "Fintech platforms have traditionally grown around non-face-to-face services, but they are now transitioning to strengthen offline touchpoints to enhance customer loyalty. Online services allow users to switch easily to better platforms, so there is a trend to combine offline infrastructure to solidify customer bases."The competition in offline payments is expected to intensify further if Apple Pay expands its partnerships with card issuers. Seo Ji-yong, a professor at Sangmyung University’s Business School, remarked, "Once Apple Pay is introduced, fintech companies will seek partnerships to expand in the offline market, leading to intensified competition for market share in face-to-face payment channels."* This article has been translated by AI. 2026-05-13 17:09:46

The Evolving Landscape of Payment Methods: Competition Intensifies in Offline Transactions The competition in the mobile payment market is shifting from securing app users to establishing dominance in offline payment infrastructure. As the mobile app market reaches saturation, the battle for control over payment terminals and networks is intensifying.According to a report released in January by global market research firm Mordor Intelligence, near-field communication (NFC) payment methods accounted for 54.2% of South Korea's mobile payment market last year.As a result, the penetration rate of NFC terminals in South Korea is expected to have increased significantly this year. The country's card payment infrastructure has primarily been built around magnetic secure transmission (MST) and integrated circuit (IC) terminals. Even after the introduction of Apple Pay, NFC-based payments remained at around 10% as of the end of last year.Recently, major tech companies Naver Pay and Toss have ramped up their competition to distribute their own NFC terminals. Toss is leading the charge, expanding its reach through its subsidiary Toss Place, which has been distributing the smart terminal Toss Front since 2023. As of April, the number of Toss Front installations surpassed 330,000. Initially focused on popular areas in Seoul, such as Seongsu and Hongdae, the infrastructure is now expanding to traditional markets and regions outside the metropolitan area.Naver Pay, a latecomer in the offline market, is accelerating its efforts. Its smart terminal, Npay Connect, launched in November, supports card payments, mobile payments, QR codes, and facial recognition payment service Face Sign. The company is employing a two-track strategy targeting both small businesses and franchises. A Naver Pay representative stated, "While we cannot disclose specific distribution figures, we believe we have exceeded our internal targets within five months of launch," adding that they are also working to introduce terminals at Paris Baguette in the second half of the year, which will increase availability in offline stores.Kakao Pay is focusing on expanding its QR-based payment network rather than distributing its own terminals. The company has opted to collaborate with existing point-of-sale (POS) and value-added network (VAN) providers instead of building its own hardware. A Kakao Pay representative emphasized, "The key is not to own the terminals but to enable Kakao Pay transactions anywhere," noting that they are expanding offline touchpoints through QR orders, kiosk payments, and international QR payments.Industry experts believe that control over offline payment data will be a crucial factor in determining the future success of the mobile payment market. As mobile payments expand beyond online transactions into the offline consumer landscape, companies that secure payment infrastructure can achieve both user lock-in effects and data competitiveness.Jeong Yu-shin, a professor at Sogang University's Business School, stated, "Fintech platforms have traditionally grown around non-face-to-face services, but they are now transitioning to strengthen offline touchpoints to enhance customer loyalty. Online services allow users to switch easily to better platforms, so there is a trend to combine offline infrastructure to solidify customer bases."The competition in offline payments is expected to intensify further if Apple Pay expands its partnerships with card issuers. Seo Ji-yong, a professor at Sangmyung University’s Business School, remarked, "Once Apple Pay is introduced, fintech companies will seek partnerships to expand in the offline market, leading to intensified competition for market share in face-to-face payment channels."* This article has been translated by AI. 2026-05-13 17:09:46 -

KB Pay Expands Beyond Payments to Integrate Financial and Daily Services KB Kookmin Card's payment platform, KB Pay, is evolving from a payment app into a comprehensive platform that connects financial and daily services offered by KB Financial Group. Building on its payment capabilities, KB Kookmin Card is enhancing its asset management services. Through MyData, users can link accounts, cards, insurance, loans, and investment information scattered across various financial institutions, allowing them to manage their assets and spending. The service also provides personalized asset and spending analysis reports, free remittances, free currency exchanges, and credit score management. The platform features services linked to KB Financial Group affiliates. The automotive service, KB Autofit, supports vehicle price inquiries, used car transactions, and automotive product shopping. Users can also access car selling and home delivery services through KB Capital's KB Chachacha. KB Real Estate offers features such as property registration, sales information, housing recommendations based on conditions, and price inquiries. KB Pay is also expanding its non-financial services. The number of customers using KB Pay's shopping and travel services surpassed 10 million just two and a half years after its official launch. The shopping tab offers special deals, local community collaboration sections, gift options, and rewards from partner shopping malls, while the travel tab provides access to flights, accommodations, car rentals, and domestic and international travel packages. Thanks to this service expansion, the number of KB Pay subscribers exceeded 16 million in January of this year. Monthly active users increased from 7.36 million in 2023 to 9.33 million in 2025.* This article has been translated by AI. 2026-05-13 17:09:00

KB Pay Expands Beyond Payments to Integrate Financial and Daily Services KB Kookmin Card's payment platform, KB Pay, is evolving from a payment app into a comprehensive platform that connects financial and daily services offered by KB Financial Group. Building on its payment capabilities, KB Kookmin Card is enhancing its asset management services. Through MyData, users can link accounts, cards, insurance, loans, and investment information scattered across various financial institutions, allowing them to manage their assets and spending. The service also provides personalized asset and spending analysis reports, free remittances, free currency exchanges, and credit score management. The platform features services linked to KB Financial Group affiliates. The automotive service, KB Autofit, supports vehicle price inquiries, used car transactions, and automotive product shopping. Users can also access car selling and home delivery services through KB Capital's KB Chachacha. KB Real Estate offers features such as property registration, sales information, housing recommendations based on conditions, and price inquiries. KB Pay is also expanding its non-financial services. The number of customers using KB Pay's shopping and travel services surpassed 10 million just two and a half years after its official launch. The shopping tab offers special deals, local community collaboration sections, gift options, and rewards from partner shopping malls, while the travel tab provides access to flights, accommodations, car rentals, and domestic and international travel packages. Thanks to this service expansion, the number of KB Pay subscribers exceeded 16 million in January of this year. Monthly active users increased from 7.36 million in 2023 to 9.33 million in 2025.* This article has been translated by AI. 2026-05-13 17:09:00