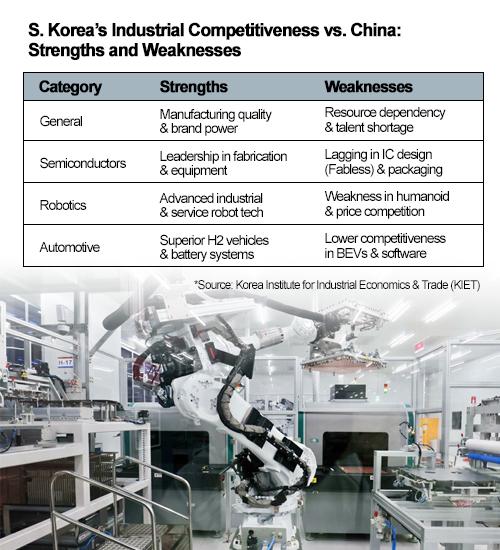

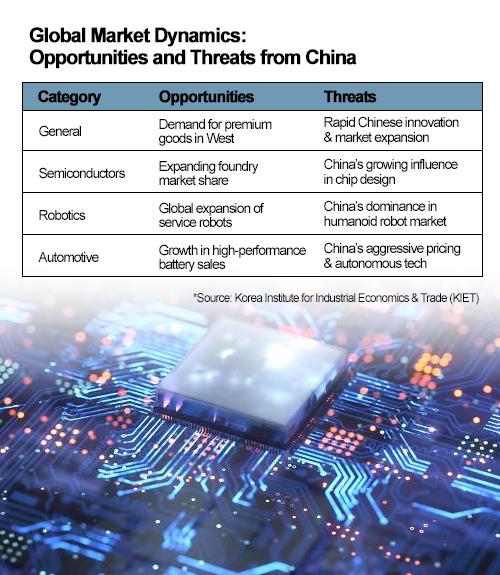

A study released by the Korea Institute for Industrial Economics and Trade (KIET) found that China now holds comprehensive value-chain advantages over Korea in core advanced manufacturing sectors, with chipmaking emerging as the country's lone remaining area of relative strength.

Based on expert surveys and focus group interviews conducted in September 2025, the report said competition between the two countries has moved beyond technological catch-up into a structural phase involving ecosystems, supply chains and global markets.

"Competition between Korea and China has now shifted from simple catch-up to structural rivalry," said Cho Eun-kyo, head of KIET's China analysis team. "China has built integrated industrial systems that Korea is struggling to match."

China's rapid ascent in future industries has redrawn the regional landscape, leaving Korean manufacturers increasingly on the defensive in sectors they once viewed as core growth engines.

Robotics: China almost a monopoly in humanoid market

The gap is most pronounced in robotics.

Chinese firms accounted for about 87 percent of the roughly 13,000 humanoid robots shipped worldwide in 2025, according to Omdia.

Shanghai-based AgiBot captured about 39 percent of global shipments, followed by Unitree Robotics with 32 percent.

KIET said that while Korea retains limited strengths in research and development for manufacturing robots, China leads in mass production, procurement and overseas market expansion. In humanoid and personal service robots, China holds advantages in technology, pricing and infrastructure.

"Yes, to be candid, South Korea does lag behind in the humanoid race," said Han Jeak-weon, a professor of robotics at Hanyang University.

"But Korea still has long-term potential if it can translate manufacturing know-how into new platforms."

Batteries: scale and localization favor China

The battery sector presents a similar picture.

According to SNE Research, six major Chinese companies controlled about 69 percent of global electric-vehicle battery installations in the first 10 months of 2025.

CATL and BYD together accounted for roughly 55 percent of the total.

KIET noted that China's lithium battery industry has achieved localization rates exceeding 90 percent across raw materials, components and equipment.

South Korea, meanwhile, continues to rely heavily on imports for key materials such as cathodes, anodes and electrolytes, leaving it vulnerable to supply disruptions and cost pressures.

EVs and autonomous driving

In electric vehicles, China has surpassed even its own industrial targets.

Under the "Made in China 2025" strategy, new energy vehicles were meant to account for 20 percent of total auto sales by 2025. The actual figure reached 45.3 percent in 2024.

Korea's EV penetration stood at about 13 percent in 2025, crossing into double digits for the first time but remaining far behind China.

The gap is widest in autonomous driving.

KIET said China leads across every segment of the value chain, supported by massive road-testing data, advanced artificial intelligence capabilities and extensive government-backed infrastructure.

In contrast, Korea's autonomous driving sector remains fragmented, with limited large-scale commercialization.

Semiconductors: the lone bright spot

Its dominance in memory chips continues to offset China's growing presence in non-memory areas such as AI processor design and system chips.

Even here, however, KIET described the balance as "contested," warning that China's heavy investment and policy support are steadily narrowing the gap.

"The semiconductor sector is no longer a guaranteed safe zone," the report said.

KIET urged policymakers and corporate leaders to fundamentally reassess Korea's industrial strategy toward China.

Rather than focusing solely on narrowing technology gaps, the institute recommended what it called "competitive cooperation" — leveraging China's massive industrial ecosystem as a testing ground for next-generation technologies, while protecting Korea's niche strengths in premium markets in the United States and Europe.

China should no longer be viewed simply as a low-cost production base or a rival to be outrun, the report said, but as a strategic learning environment.

Without structural reforms, sustained investment and clearer industrial priorities, the country risks becoming increasingly dependent on semiconductors as its last remaining pillar in the global technology race, it concluded.

Copyright ⓒ Aju Press All rights reserved.