The benchmark KOSPI surged nearly 50 percent in the first two months of the year, pushing past the 6,300 level after an extraordinary 76 percent gain in 2025, making it one of the world’s strongest equity markets.

The mood reversed abruptly when investors returned from a long holiday weekend to the shocking news of U.S.–Israeli strikes on Iran that killed the country’s supreme leader and senior military officials.

Within days, the Korean equity market experienced one of the most dramatic swings in its history.

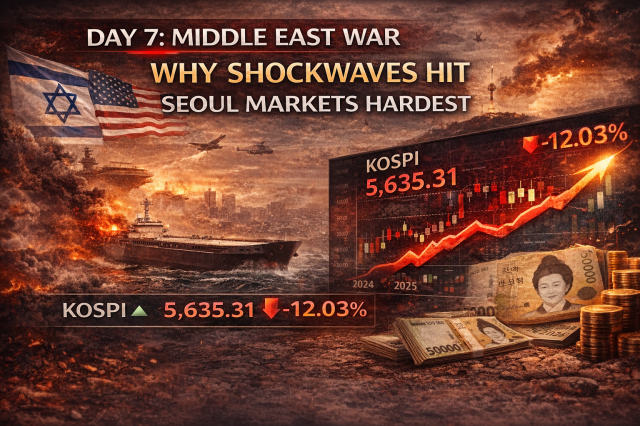

The first week of the Middle East war triggered a historic whipsaw in Seoul, sending the KOSPI plunging 12 percent in a single session — the worst crash on record — before rebounding nearly 10 percent the next day as oil prices, the Korean won and foreign investor positioning repriced simultaneously.

By the end of the first week of March, the market was still roughly 10 percent lower than before the war began.

On Wednesday — the second trading day after the weekend strikes — the KOSPI collapsed 12 percent. The index then surged back the following day in a near mirror-image rebound.

The tug-of-war continued through Friday as retail investors and foreign funds battled for control of the market, producing one of the most volatile trading weeks in decades.

“This market is not for the faint of heart,” veteran investor Jim Bianco wrote on X.

Part of the turbulence reflected timing. Korea’s market had been closed for a three-day holiday from Feb. 28 to March 2, compressing the geopolitical shock into the first two trading sessions of March.

But the magnitude of the swings also revealed how quickly risk premiums can be repriced in Korea — a market where oil prices, the currency and foreign investor flows often move together.

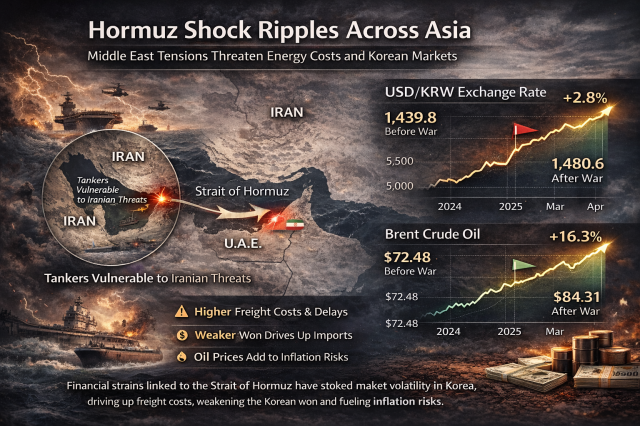

Hormuz shock ripples across Asia

The war’s financial shock spread quickly across Asia, a region heavily dependent on Middle Eastern energy shipments passing through the Strait of Hormuz.

Although the strait was not formally closed, Iranian threats against vessels and heightened military tensions effectively slowed shipping traffic and increased the perceived risk of disruption.

For global markets, the mere possibility of disruption was enough.

Even without a full blockade, the risk feeds into energy costs through multiple channels: higher war-risk insurance premiums, tanker rerouting, delivery delays and rising freight rates.

Those costs ultimately raise the landed price of oil and industrial inputs.

For Korea, those risks translate directly into market volatility. The country imports about 70.7 percent of its crude oil and roughly 20.4 percent of its liquefied natural gas from the Middle East, leaving it unusually exposed to geopolitical disruptions in the Gulf.

When global investors move into risk-off mode, those structural vulnerabilities quickly become an equity story.

Energy is priced in dollars. When oil rises while the Korean won weakens, the import bill increases twice — lifting inflation risks and squeezing corporate margins.

That dynamic was visible throughout the week.

The dollar-won exchange rate climbed from 1,439.8 before the war to 1,480.6 by Thursday, briefly touching 1,506.7, a level widely seen by investors as a psychological stress threshold.

Meanwhile Brent crude jumped from $72.48 to $84.31, reaching an intraday high of $86.27.

For Korea, oil and foreign exchange tend to reinforce each other. When both move at once, the market typically reprices risk more aggressively than peers with lower energy exposure or weaker FX sensitivity.

Foreign selling amplifies the drop

Foreign investor flows amplified the volatility.

Korea’s equity market has one of the highest foreign participation rates among major markets, meaning global portfolio shifts can move the index rapidly.

Foreign investors had already been trimming positions after Korea’s extraordinary rally.

Data from the Korea Exchange show foreign investors sold 26.1 trillion won worth of shares in the benchmark market this year as of March 3.

The selling was concentrated in the large-cap stocks that had led the rally — particularly Samsung Electronics and SK Hynix, the backbone of the KOSPI.

Foreign investors sold 22 trillion won worth of Samsung Electronics shares and 10.5 trillion won of SK Hynix, while also trimming positions in Hyundai Motor and Hyundai Mobis.

Individuals bought 12.8 trillion won of Samsung Electronics and 6.7 trillion won of SK Hynix, absorbing much of the foreign selling pressure.

According to Noh Dong-gil, a researcher at Shinhan Securities, foreign investors were not abandoning Korea entirely but were rebalancing their portfolios.

“They reduced exposure to semiconductors — the key driver of KOSPI volatility — while adding defensive or policy-related stocks,” he said.

“The problem was the scale and speed of the selling, which amplified the market’s decline.”

Base case vs. Stress case

For strategists, the week’s violent swings reflected a rapid shift between base-case and stress-case geopolitical scenarios.

Kim Do-un, a senior analyst at Hana Securities, described the whipsaw as a market briefly pricing in an extreme energy shock.

Historically, he said, Middle East crises often create buying opportunities — provided the conflict does not escalate into a prolonged oil shock.

“If the conflict doesn’t escalate into an all-out regional war and oil does not move into the $100 to $120 range, then the pullback at these levels can be interpreted as a healthy correction,” Kim said.

“What we saw was the market’s center of gravity shifting — at least temporarily — from the base scenario toward the worst-case scenario.”

Kim mapped those scenarios into index levels.

“If the conflict remains contained within roughly two months and the currency stabilizes, the KOSPI’s lower bound would likely be around 5,600,” he said.

“But if Hormuz disruption intensifies, the won breaks above 1,500 again and oil approaches $120, then a move toward 5,000 becomes plausible.”

Copyright ⓒ Aju Press All rights reserved.