Broadcom, a semiconductor company based in California, was once a dominant player in the wireless communication chip market. However, during the smartphone era of the 2000s, it struggled against Qualcomm, the reigning champion. With the advent of the AI era, Broadcom has regained prominence, creating network chips that connect the "brain" developed by Nvidia to data centers. This has led to Broadcom being dubbed the "hidden infrastructure king of the AI era," enjoying growth comparable to Nvidia.

The company's stock has soared, rising from $119 two years ago to $495 this year. However, following its second-quarter earnings report on June 3, the stock plummeted by about 13%. This decline was not due to poor performance; Broadcom reported $22.19 billion in revenue and earnings per share (EPS) of $2.44 for the second quarter, marking increases of 48% and 88%, respectively, compared to the previous year. Notably, AI semiconductor sales reached $10.8 billion in the second quarter, a staggering 148% increase year-over-year, with third-quarter projections at $16 billion, a 200% rise.

So why did the stock drop? The reason lies in the company's guidance, or its future earnings outlook, which fell short of market expectations. Broadcom projected third-quarter AI chip sales at $16 billion, below the anticipated $17.2 billion, prompting market reassessment. The "Broadcom shock" also sent shockwaves through the Korean stock market, which saw a drop of over 6% during trading on June 5, reflecting broader global market impacts.

The "Broadcom shock" highlights the immense expectations surrounding AI and the underlying concerns about a potential bubble. The assessment that "even doubling year-over-year growth is insufficient" underscores the high bar set for AI-related performance.

Ray Dalio, founder of the world's largest hedge fund, Bridgewater Associates, shared insights during a Bloomberg TV interview on June 3, stating, "All great technological innovations create bubbles, and no one can predict them accurately." He suggested that, similar to the internet boom, the AI revolution may also be accompanied by a bubble. Dalio noted, "Bubbles burst when people try to convert their wealth into cash." Currently, investments are being made based on the future potential of AI innovations, but at some point, investors will demand actual returns, leading to the exit of companies that cannot meet these expectations.

Dalio's comments reflect a recurring argument regarding the "AI bubble." In summary, he pointed out:

"In the past two to three years, there has been a global AI investment boom, primarily led by major U.S. tech companies. These so-called 'hyperscalers,' which operate large-scale AI data centers, have poured astronomical amounts of money into maintaining their leadership in the AI era. Key players include Meta Platforms, Microsoft, Amazon, and Alphabet (Google). The combined capital expenditure (CAPEX) forecast for these four companies from fiscal years 2025 to 2030 is estimated at $5.3 trillion, equivalent to approximately 8,000 trillion won. To sustain such massive investments, they need to generate revenue from AI operations. While some funding may come from loans or equity offerings, fundamentally, profits must be realized to cover expenses. If AI-generated revenues fall short of expectations, planned CAPEX could be disrupted, leading investors who bought stocks based on vague optimism to reconsider their positions."

Concerns about the AI bubble extend to the semiconductor sector. The significant capital expenditures (CAPEX) by hyperscalers like Meta, Amazon, and Microsoft are ultimately investments in semiconductor purchases. The soaring demand for Nvidia's GPUs and Broadcom's network chips, along with the rising performance and stock prices of companies like Samsung Electronics and SK Hynix, which produce components like HBM needed for AI chip manufacturing, is driven by the purchasing power of these hyperscalers.

Ultimately, investors are keenly interested in whether the semiconductor supercycle driven by AI is sustainable. If the proponents of the AI bubble are correct, hyperscaler companies may face a period of negative growth, leading to a disruption in their extensive capital expenditure plans and a decline in semiconductor purchase demand. A reduction in semiconductor demand by hundreds of trillions could have significant repercussions for the market. This is why semiconductor stocks in the U.S. and Korea experience sharp declines whenever concerns about the AI bubble arise.

So, how long will the semiconductor supercycle last? Will it begin to decline the moment the AI bubble bursts?

There are alternative perspectives on this issue, supported by robust arguments. Some assert that the AI bubble does not imply limitations on the innovations AI can achieve, and that demand for AI-driven semiconductors will continue to grow at an extraordinary pace. Recently, TSMC Chairman Wei Zhejia expressed this view, stating, "It will take a long time to meet customer demand for AI chips." The expectation is that the supply of semiconductors will lag behind AI demand for several years.

Analyses suggesting that the semiconductor cycle differs from past cycles further bolster this outlook. Historically, the semiconductor cycle during the PC era lasted about four to five years, driven by demand from PCs, which dictated the market's ups and downs. This cycle followed a pattern of corporate IT investment leading to rising memory prices, increased supply, decreased demand, oversupply, and subsequent recession. During downturns, semiconductor companies' profits declined, and investments were curtailed. Samsung's rise as a DRAM powerhouse was due to its aggressive investment strategy during downturns, preparing for future booms.

The cycle during the smartphone era was shorter than that of the PC era, but still followed a roughly three-year pattern, with semiconductor (memory) demand fluctuating in line with the expansion of smartphone adoption and the introduction of new form factors.

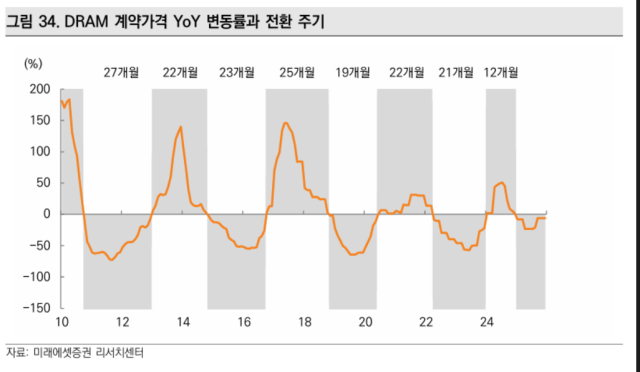

However, entering the AI era has distinctly altered the semiconductor cycle. The amplitude of fluctuations is decreasing, and the cycles are becoming narrower. According to analysis by Mirae Asset Securities, the semiconductor cycle, which was around 27 months in 2010, has recently shortened to 12 months. This change has been driven by the explosive demand for AI-related semiconductors. In addition to consumer demand from PCs and smartphones, the emergence of hyperscalers has transformed the cycle itself.

Moreover, AI is evolving. The realm of AI, once centered on web pages, is now expanding into the physical domain (Physical AI). Kim Jin-guk, CEO of VIP Asset Management, noted, "If we enter the era of robots, semiconductor demand could explode even further," highlighting the uncertainty surrounding how many GPUs, CPUs, and communication chips will be used in each robot and how many robots will be produced.

Concerns about the AI bubble will likely persist. Each time earnings forecasts fall short of market expectations, as seen with the Broadcom shock, semiconductor stocks may experience significant volatility. Some hyperscaler companies may falter, and certain investment plans may be revised. The market will react accordingly.

However, it is also evident that historically, great technological innovations have always grown alongside bubbles. This was true for railroads and the internet. While bubbles may burst, innovations endure. The same will hold true for the AI era. While caution is warranted regarding the existence of bubbles, it is crucial to observe who will reap the benefits of these innovations. This may well be the path to successful investing in the age of AI revolution and innovation.

* This article has been translated by AI.

Copyright ⓒ Aju Press All rights reserved.