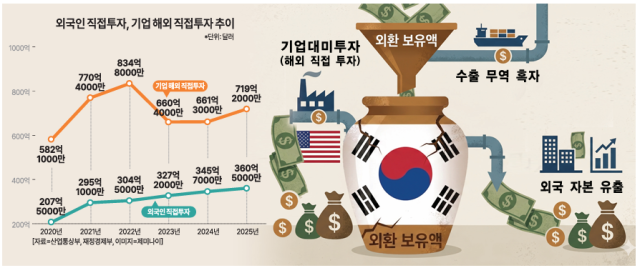

According to the Ministry of Trade, Industry and Energy, foreign direct investment (FDI) flowing into South Korea totaled $36.05 billion last year, while South Korean companies' overseas direct investment (ODI) reached $71.9 billion, more than double the FDI figure. FDI refers to investments where foreign entities acquire at least 10% of a domestic company's shares or participate in its management, serving as an indicator of South Korea's long-term investment appeal.

High exchange rates could potentially increase FDI inflows. A higher exchange rate allows foreign investors to secure more won-denominated assets and facilities for fewer dollars, lowering initial investment costs. An increase in FDI would lead to more dollars entering the domestic market, strengthening the won and contributing to exchange rate stability. However, FDI in 2025 saw only a slight increase from the previous year ($34.57 billion), suggesting that foreign investors maintain a negative long-term outlook on South Korea's economic fundamentals despite the high exchange rates.

Additionally, since the onset of the Trump administration's second term, the trend of reshaping supply chains and increasing investments in the U.S. has accelerated the relocation of domestic companies' production bases overseas. Major South Korean corporations have significantly increased local factory investments in North America to meet U.S. subsidy requirements and avoid high tariffs. The number of overseas direct investments has steadily risen from 10,657 in 2020 to 13,190 in 2024.

The outflow of direct investments is compounded by foreign capital withdrawal from the securities market. As of June 5 this year, foreign investors have net sold a total of 119 trillion won in domestic securities. The stock market briefly surpassed 8,000 points, prompting profit-taking actions. Consequently, each time foreign selling increases, the exchange rate has also risen in tandem. Furthermore, even with a slight trade surplus each month, the demand for currency exchange from foreign stock sales (dollar purchases) has far exceeded the trade surplus, negating its benefits.

The pace of foreign capital outflow has accelerated since the outbreak of war in the Middle East. Compared to the global financial crisis in 2008 or the COVID-19 pandemic in 2020, the recent foreign stock sell-off has significantly heightened liquidity pressures, making it increasingly difficult to meet dollar exchange demands solely through trade surpluses.

Experts point to large-scale investment agreements with the U.S. as a factor pressuring the won's supply. Jeong Yong-taek, a researcher at IBK Investment & Securities, stated, "Given the substantial investments planned in local currency dollars, even if exports increase significantly, there is little incentive to convert funds into won for domestic use. Once these investments are executed, the resulting demand for dollars will exert psychological pressure on market participants."

* This article has been translated by AI.

Copyright ⓒ Aju Press All rights reserved.