Major central banks are returning to a tightening mode, signaling a new phase for the global economy. Just last year, concerns over economic slowdown led to widespread expectations of interest rate cuts. However, rising inflation and strong economic momentum have changed the landscape. The U.S. Federal Reserve, the European Central Bank (ECB), and the Bank of Japan (BOJ) have all shifted towards tightening, and the Bank of Korea is also expected to raise its benchmark interest rate next month. As central banks tighten monetary policy, a reduction in liquidity, rising borrowing costs, and increased volatility in asset markets have become inevitable.

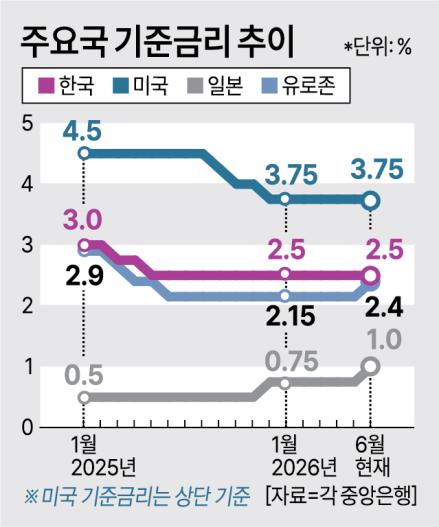

On June 17, the Federal Reserve held its benchmark interest rate steady at 3.50% to 3.75% during its Federal Open Market Committee (FOMC) meeting but indicated the possibility of future rate hikes. Wall Street had anticipated a more hawkish stance from the Fed, and the actual message was deemed even more aggressive. According to the FOMC dot plot, nine out of 18 committee members forecast at least one rate hike by the end of the year, a significant shift from March when no hikes were expected.

Additionally, the ECB recently raised its policy rate in response to inflation concerns stemming from the Middle East, while the BOJ increased its benchmark rate to 1% for the first time in 31 years, leaving the door open for further hikes. Market analysts predict that South Korea will begin raising its benchmark rate in July, with expectations of reaching 3.00% by the end of the year and 3.50% next year.

There are forecasts that this tightening cycle could last for an extended period, differing from the transition in 2022. At that time, expectations were high for a quick return to rate cuts following rapid increases and subsequent economic slowdown. In contrast, the current situation is characterized by rising energy prices, geopolitical risks, and sustained economic growth, suggesting that inflationary pressures may persist longer than anticipated. Both supply shocks and demand-side pressures are likely to prolong the high-interest-rate environment.

The Bank of Korea has noted the shift in monetary policy among major economies. Deputy Governor Yoo Sang-dae stated during a market situation assessment meeting, "As the Fed signals the possibility of rate hikes in response to inflation pressures following the ECB and BOJ, a visible shift in the monetary policy stance of major countries is becoming apparent. We expect the Fed's communication strategy to change, which may increase uncertainty regarding the future path of monetary policy."

The transition to tightening is expected to have significant impacts across the economy. First, corporate borrowing costs may rise, particularly for marginal firms that struggle to cover even interest expenses with their earnings. Last year, the proportion of marginal firms reached a record high of 39%. If high-interest rates persist, there are concerns that pressure for corporate restructuring may increase. Households will also face greater repayment burdens due to rising loan interest rates, which could act as a counterbalance to the recent optimism in the stock and real estate markets that has led to increased household borrowing.

Asset markets are likely to experience heightened volatility. A reduction in liquidity that has supported stock markets could lead to greater fluctuations in asset prices. As the likelihood of interest rate hikes increases, risk appetite may diminish, potentially cooling the domestic stock market, which recently achieved a significant milestone. Currency exchange rates are also expected to be affected. If the U.S. raises interest rates, the dollar may strengthen, leading to a depreciation of the won, a risk asset. However, this could have positive implications for export companies competing with Japan, as a stronger yen would enhance the price competitiveness of domestic firms.

Nomura Securities economist Park Jong-woo noted, "For every 0.25 percentage point increase in the benchmark rate, households and businesses will face an additional interest burden of approximately 7 trillion won. If rates rise three more times, the additional burden could exceed 20 trillion won. However, we believe that sufficient fiscal capacity this year and next will allow fiscal policy to partially offset these effects."

* This article has been translated by AI.

Copyright ⓒ Aju Press All rights reserved.