The KONEX market serves as a funding avenue for early-stage small and venture companies. Established 13 years ago, it has now become a "ghost house." The flow of new listings has ceased, with an increasing number of companies exiting the market. Although over 100 companies are listed, the average daily trading volume is only between 1 billion and 1.5 billion won, with just 560,000 shares traded daily. The phrase "only the wind blows" aptly describes the current situation. The original purpose of serving as a "growth ladder" for small and venture companies has been lost.

◆ KONEX Market Faces Decline

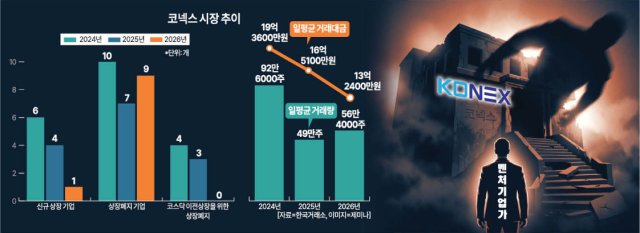

According to the Korea Exchange, only one new company, S-Tech M, was listed on the KONEX market this year, in April. Following the trend of just six new listings in 2024 and four in 2025, this year has seen a significant drop in new entries. In contrast, more companies are leaving the market, with 10 delistings in 2024 and seven in 2025. This year, nine companies, including AMSC, have been delisted.

The KONEX's role as a "growth ladder" has become ineffective. Originally designed as a stepping stone for companies to transition to the KOSDAQ, the need to use KONEX has diminished as direct pathways to KOSDAQ, such as technology-based and growth-based listings, have expanded. In fact, there have been no transitions from KONEX to KOSDAQ this year, following four in 2024 and three in 2025.

Market liquidity is also drying up. Over the past three years, the average daily trading volume in the KONEX market has steadily decreased from 1.936 trillion won to 1.651 trillion won, and then to 1.324 trillion won. Trading volume plummeted from an average of 926,000 shares in 2024 to 490,000 shares in 2025, and has stagnated at around 564,000 shares this year.

◆ Market Distortions Undermine Confidence

The absence of trading in the KONEX market has led to extreme market distortions. There are instances where stocks with zero trading volume have market capitalizations exceeding 1 trillion won. One such example is Bon Systems, which, as of June 22, had a closing price of 1,023,000 won and a market cap of 1.039 trillion won. With 1,015,973 shares listed, it accounts for about 30% of the total market capitalization of 3.4217 trillion won in KONEX.

Bon Systems, a company developing robotic components and motion control solutions, has not seen any actual trading since its listing in September last year, yet its stock price has surged from an initial public offering price of 16,300 won to 1,023,000 won, representing an increase of approximately 6,176%. Despite recording zero trading volume and value, its market capitalization has surpassed 1 trillion won.

This phenomenon stems from the KONEX's pricing mechanism. According to the Korea Exchange, if no trades occur, the closing price is determined based on the highest bid or lowest ask price at market close. Even without actual transactions, if bids are high, the reference price can rise. While the exchange describes this as a normal pricing mechanism under current regulations, it undeniably undermines market confidence.

◆ "Introduction of a Lift System? KONEX's Position May Worsen"

In light of the ongoing challenges, the exchange and industry stakeholders are seeking to revitalize the market through renewed support measures. A representative from the KONEX Association stated, "There are companies planning to list this year, and since KONEX serves as a bridge for transitioning to KOSDAQ, many cases typically enter the market in the second half of the year."

The association plans to resume support programs that were halted in 2023 to incentivize new listings. A total of 1 billion won will be allocated to cover some listing costs, including external auditor fees and advisory fees, from this month until the end of the year. The exchange is also working on regulatory improvements, including increasing the mandatory distribution ratio for KONEX-listed companies from the current 5% to a maximum of 15% and granting priority negotiation rights to designated advisors for facilitating transitions to KOSDAQ.

Despite these efforts, the future of KONEX remains uncertain. Concerns are growing that the government's plan to restructure the KOSDAQ market into a two-tier system in the second half of this year may further diminish KONEX's standing.

* This article has been translated by AI.

Copyright ⓒ Aju Press All rights reserved.