SEOUL, June 23 (AJP) - The race to build humanoid robots is no longer a contest over engineering prowess but a battle over who can manufacture them at scale and deploy them reliably. That gives automotive powerhouses such as South Korea a strategic advantage, according to Hong Kong-based Citic CLSA.

The transition is pulling automakers and auto suppliers — including Hyundai Motor Group and Hyundai Mobis — into what was once viewed primarily as a rivalry among robotics startups and artificial intelligence companies.

"Robotics momentum has largely been priced into Hyundai Motor shares, but not into the rest of the group," said Brian Lee, a research analyst covering humanoid robotics and autos at CLSA, during the brokerage's Northeast Asia Forum in Seoul on Tuesday.

He noted that Kia owns a 17 percent direct stake in Boston Dynamics, while Hyundai Mobis and Hyundai Glovis each hold 11 percent stakes. All three companies could benefit through ownership, component supply or logistics, yet none has received a similar market re-rating.

Global humanoid production totaled roughly 50,000 units last year. If current development roadmaps are met, annual output could rise to 400,000 units by 2028 and exceed 1 million by 2030, according to CLSA.

The first mass market for humanoids is unlikely to be households.

Homes remain messy, unpredictable environments where mistakes carry significant safety and legal risks.

Factories offer a more controlled setting. Workspaces are confined, tasks are repetitive and safety zones can be clearly defined.

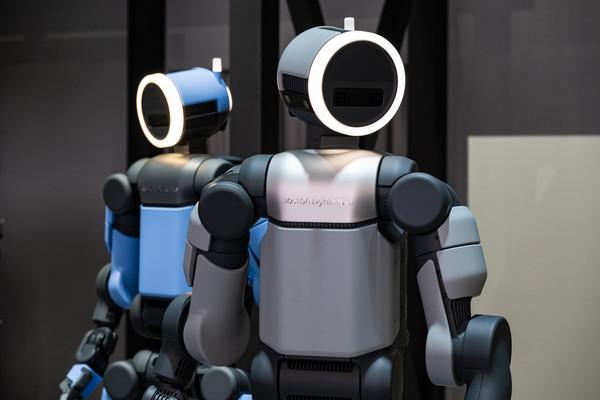

Boston Dynamics is already testing Atlas inside Hyundai Motor Group facilities. Tesla is deploying Optimus in its factories. Figure AI has worked with BMW at its Spartanburg plant, while Apptronik is testing Apollo with Mercedes-Benz.

These are no longer stage demonstrations. They are early industrial pilots tied directly to production lines, and the advantage increasingly belongs to companies that already operate giant factories.

Tesla possesses large-scale manufacturing expertise and global supply chains. Hyundai Motor Group, which acquired Boston Dynamics for about $1.1 billion in 2021, can leverage one of the world's largest automotive production networks.

Both companies also have built-in demand. Their own factories provide an immediate market that smaller robotics startups cannot easily replicate.

The economics are becoming difficult to ignore.

The annual cost of employing a U.S. factory worker is approaching $100,000. CLSA estimates the annual operating cost of an industrial humanoid could fall to around $30,000 by 2030 and to $10,000 by 2035, potentially reducing labor costs by 60 to 70 percent.

For manufacturers where labor accounts for roughly 10 percent of revenue, that could translate into nearly five percentage points of additional operating margin.

Robots also do not work eight-hour shifts.

Figure AI recently demonstrated a humanoid performing logistics tasks for 10 consecutive days at close to human productivity levels. On a 24-hour basis, that output could exceed what a single worker can deliver.

CLSA projects the global humanoid market will expand to $69 billion by 2030, $320 billion by 2035 and more than $1 trillion by 2045.

The next battleground is data.

Every robot deployed on a factory floor generates operational data that can train the next generation of machines, creating a feedback loop that increasingly rewards scale.

CLSA estimates that whichever company reaches annual production of 50,000 to 100,000 units first could lower manufacturing costs by 30 to 40 percent ahead of rivals while accumulating training data at a pace competitors would struggle to match.

In effect, humanoids could follow the same playbook that propelled electric vehicles: scale lowers costs, lower costs accelerate adoption, and adoption generates more data.

The dynamic could create an entirely new market for auto parts manufacturers.

Actuators — the systems that power a robot's joints — account for an estimated 80 to 85 percent of a humanoid's manufacturing cost, according to CLSA. Each robot requires 30 to 50 units.

Hyundai Mobis has secured an agreement to supply all actuator requirements for Boston Dynamics, CLSA said.

Other suppliers, including HL Mando, Schaeffler and Bosch, are also preparing for the market.

The opportunity is amplified by geopolitics.

Many non-Chinese robot developers currently depend on Chinese suppliers for actuators. Potential U.S. import restrictions could create an opening for Korean and European manufacturers.

That could turn the humanoid race into yet another industrial competition centered on supply chain resilience.

The outlook remains far from certain.

Current forecasts assume robot prices fall rapidly from $100,000-$150,000 today to $40,000-$50,000 by 2030. That may prove optimistic if production bottlenecks persist or key components remain expensive.

Safety presents another challenge. Humanoids operating alongside humans must function reliably almost all the time. Breakdowns and maintenance costs could slow adoption even when the economics appear favorable.

Labor regulations may also determine the pace of deployment.

The United States and Europe may move faster because of acute worker shortages. The United States alone faced a shortage of roughly 400,000 manufacturing workers last year.

South Korea and Japan, despite rapidly aging populations, could adopt humanoids more cautiously because of stricter labor protections.

China, meanwhile, already produces more than two-thirds of global humanoid output and retains supply-chain advantages that will not disappear quickly.

Major robot developers are expected to finalize supplier selections by the end of 2026 ahead of mass-production ramps targeted for 2028.

The race remains young, but its trajectory is becoming clearer.

The winners may not be the companies that build the smartest robots. They may be the automakers and suppliers that can manufacture them at scale, place them in real workplaces and improve them faster than everyone else.

Copyright ⓒ Aju Press All rights reserved.