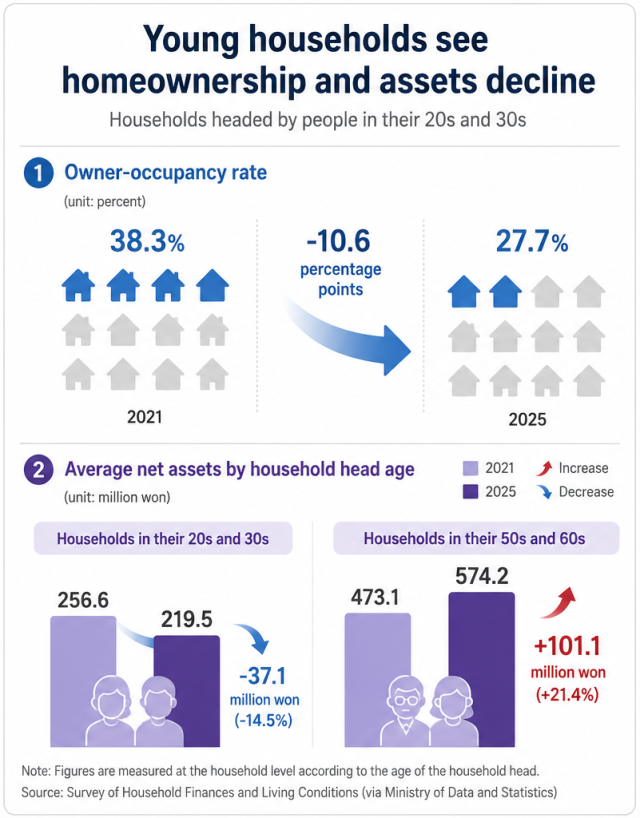

An analysis of anonymized household microdata from the Survey of Household Finances and Living Conditions, reported by Munhwa Ilbo on July 13, showed that the owner-occupancy rate among households headed by people in their 20s and 30s fell to 27.7 percent in 2025 from 38.3 percent in 2021.

The decline coincided with a widening wealth gap between generations. Average net assets of younger households dropped to 219.5 million won ($159,000) from 256.6 million won over the same period, while households headed by people in their 50s and 60s saw average net assets rise to 574.2 million won from 473.1 million won.

The owner-occupancy and net asset figures are measured at the household level according to the age of the household head.

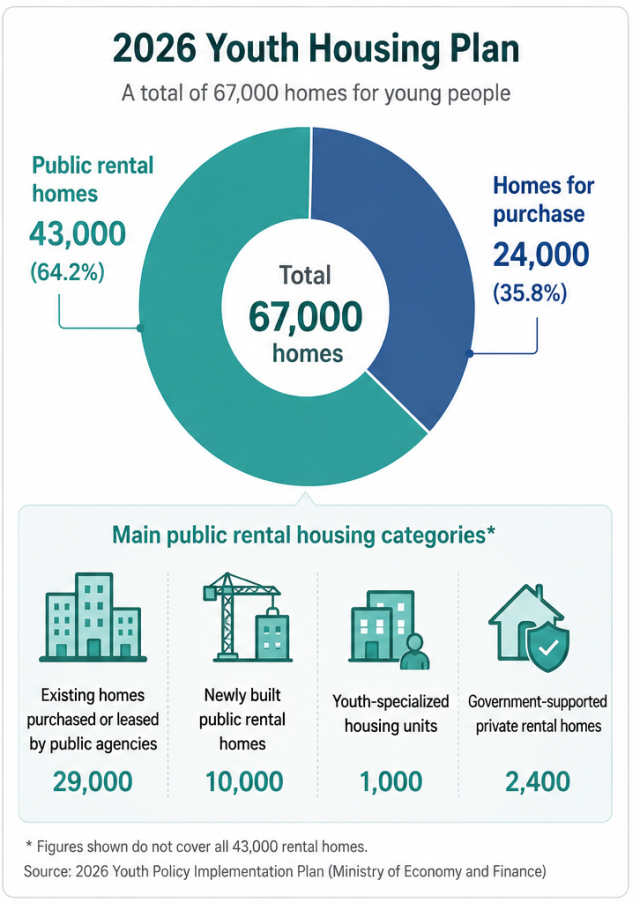

The deterioration comes as the government's latest youth housing policy increasingly relies on expanding rental housing rather than ownership opportunities.

The rental program consists mainly of 29,000 existing homes purchased or leased by public agencies and rented to young tenants, along with 10,000 newly built public rental homes, 1,000 youth-specialized housing units and 2,400 privately supplied rental homes supported and regulated by the government.

While public rental housing offers lower rents and longer tenancy security, it does not allow occupants to build housing wealth in the way homeownership does. Publicly supplied homes transfer ownership to buyers, although the eventual financial gains depend on purchase prices, location and future market conditions.

The emphasis on rental housing reflects a broader trend in government policy over the past decade.

According to the government's second Basic Plan for Youth Policy, about 460,000 public homes for young people were approved between 2021 and 2025, including 295,000 rental units and 164,000 homes for sale. The government said most of those figures represented project approvals, meaning a considerable time lag remained before construction, completion and actual occupancy.

An earlier youth housing initiative announced by the Moon Jae-in administration in 2018 likewise focused heavily on rental support, comprising 140,000 public rental homes and 130,000 government-supported private rental units through 2022.

Separate administrative statistics also point to a persistent gap between generations.

The Ministry of Data and Statistics' "Administrative Statistics by Life Cycle in 2024," released on Dec. 23, showed that only 11.5 percent of individuals aged 15 to 39 owned a home, unchanged from a year earlier. That compared with 45.5 percent among those aged 40 to 64 and 46.3 percent among people aged 65 and older.

The ministry noted that younger homeowners earned nearly twice as much income from wages and business as non-homeowners but also carried significantly heavier debt, with median loan balances 6.5 times larger than those without homes.

The administrative homeownership figures are calculated for individuals, while the owner-occupancy and net asset figures from the household finance survey are measured at the household level and therefore are not directly comparable.

Economists have increasingly argued that rising housing costs are becoming a structural drag on Korea's economy rather than simply a housing affordability issue.

In an issue note published on Jan. 19, the Bank of Korea estimated that every 1 percent increase in housing costs reduced the total assets of young people by 0.04 percent. The central bank said rising housing expenses constrain consumption as well as spending on education, skills and career development, describing youth employment and housing as "structural problems constraining Korea's growth."

A separate BOK study released on Feb. 12 found that a 5 percent increase in housing prices reduced the economic well-being of households headed by people younger than 50 by 0.23 percent while increasing that of older households by 0.26 percent.

According to the central bank, younger households typically respond to higher home prices by saving more aggressively or taking on larger mortgages to purchase their first home or move into better housing, reducing current consumption. Older households, already holding substantial housing assets, benefit from rising property values without facing the same financial burden.

Kang Min-joo, ING's senior economist for South Korea and Japan, said in Asia 2026: 6 Questions for Korea's Recovery, published on Dec. 3, that persistently strong demand and chronically limited housing supply in Seoul continued to push prices higher.

Kang noted that Korean households hold roughly 46 percent of their total assets in real estate. However, because property is difficult to convert into cash and mortgage repayments consume a growing share of income, rising home values have provided only limited support for private consumption.

The housing market has also complicated monetary policy.

When the Bank of Korea kept its benchmark interest rate unchanged at 2.50 percent on May 28, it warned that housing prices in the Seoul metropolitan area and expectations of further gains had strengthened while housing-related lending continued to accelerate.

Korea's household debt stood at nearly 89 percent of nominal gross domestic product at the end of last year, among the highest levels in the developed world.

Kang said the growing divergence between the overheated Seoul housing market and weaker regional markets could constrain the central bank's policy flexibility in either direction, making it more difficult to balance inflation, financial stability and economic growth.

The property market is also intersecting with broader capital flows.

According to the BOK, Korean residents' investment in overseas stocks and bonds more than doubled to $140.3 billion last year from $67 billion in 2024, increasing its share of gross domestic product to 7.5 percent from 3.6 percent.

The central bank said overseas investment strengthens Korea's external asset position and future investment income but can temporarily weaken the won by increasing demand for foreign currencies.

Kang also said whether Korean investors increasingly favor overseas assets over domestic investments could become an important factor influencing the won. No official study, however, has established a direct causal relationship between declining youth homeownership and rising overseas investment.

For now, the government's latest housing plan leaves several critical questions unanswered. While it specifies the number of homes to be supplied, it provides few details on regional allocation or when projects will move from approval to construction, completion and actual occupancy.

For many younger Koreans, those timelines may prove just as important as the number of homes promised, as each year spent waiting for new supply risks placing homeownership even further beyond reach.

Copyright ⓒ Aju Press All rights reserved.