Journalist

Ahn Seon Young

asy728@ajunews.com

-

Woori Bank and Samsung Wallet Money Surpass 2 Million Users in Six Months Woori Bank, in partnership with Samsung Electronics, announced that its Samsung Wallet Money service has exceeded 2 million new users within six months of its launch. The service differentiates itself from existing payment options by allowing users to make online and offline transactions using only their smartphones, as well as offering ATM withdrawals and money transfer capabilities. Samsung Wallet Money is automatically registered in the Samsung Wallet, enabling payments with just a smartphone tap without needing to open a separate app. Unlike some payment services that only work at QR code merchants, it can be used at regular card merchant locations, utilizing existing card payment infrastructure without requiring additional devices. The registration process has also been simplified. Users can sign up with just a mobile phone verification, and those aged 14 and older can directly recharge and make payments. The integration with Samsung Wallet, a standard service on Samsung smartphones, enhances accessibility by eliminating the need for a separate app installation. Recently, the service introduced a mobile transit card top-up feature to improve convenience. Users of Samsung Wallet Money can recharge their T-money mobile transit card balance without fees through an update to the Samsung Wallet app. Additionally, a top-up service for the Izle (formerly Cashbee) mobile transit card is in development, aiming for a launch in early the third quarter of this year. "Beyond simply expanding payment methods, the significance of Samsung Wallet Money lies in enhancing financial convenience in daily life," said Heo Min-woo, a manager in Woori Bank's platform business division. "We will continue to provide a broad financial experience for all customer segments."* This article has been translated by AI. 2026-05-13 17:11:14

Woori Bank and Samsung Wallet Money Surpass 2 Million Users in Six Months Woori Bank, in partnership with Samsung Electronics, announced that its Samsung Wallet Money service has exceeded 2 million new users within six months of its launch. The service differentiates itself from existing payment options by allowing users to make online and offline transactions using only their smartphones, as well as offering ATM withdrawals and money transfer capabilities. Samsung Wallet Money is automatically registered in the Samsung Wallet, enabling payments with just a smartphone tap without needing to open a separate app. Unlike some payment services that only work at QR code merchants, it can be used at regular card merchant locations, utilizing existing card payment infrastructure without requiring additional devices. The registration process has also been simplified. Users can sign up with just a mobile phone verification, and those aged 14 and older can directly recharge and make payments. The integration with Samsung Wallet, a standard service on Samsung smartphones, enhances accessibility by eliminating the need for a separate app installation. Recently, the service introduced a mobile transit card top-up feature to improve convenience. Users of Samsung Wallet Money can recharge their T-money mobile transit card balance without fees through an update to the Samsung Wallet app. Additionally, a top-up service for the Izle (formerly Cashbee) mobile transit card is in development, aiming for a launch in early the third quarter of this year. "Beyond simply expanding payment methods, the significance of Samsung Wallet Money lies in enhancing financial convenience in daily life," said Heo Min-woo, a manager in Woori Bank's platform business division. "We will continue to provide a broad financial experience for all customer segments."* This article has been translated by AI. 2026-05-13 17:11:14 -

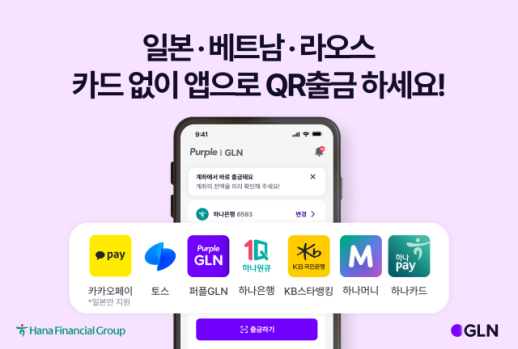

Hana Bank's GLN Expands Overseas QR Withdrawal Partnerships, Enabling Cash Withdrawals via KakaoPay in Japan Hana Bank's subsidiary, GLN International, is expanding its overseas QR withdrawal service in Japan, Vietnam, and Laos. This enhancement allows users of major domestic financial and platform apps to withdraw local currency without the need for currency exchange. The expansion focuses on the Japanese market, increasing the number of partner app channels from three to seven. Notably, KakaoPay, which enjoys high usage rates in Japan's mobile payment sector, has been added to the list of domestic partner apps. As a result, travelers to Japan can now access QR withdrawal services through not only Hana OneQ, Hana Money, and Toss apps but also Hana Pay, KakaoPay, Purple GLN, and KB Star Banking apps. Withdrawals can be made at Seven-Eleven convenience store ATMs and Seven Bank ATMs located in airports throughout Japan. QR payments are also accepted at various merchants, including convenience stores, clothing shops, and health and beauty stores. In Vietnam and Laos, users can access QR withdrawal services through six apps: Hana OneQ, Hana Money, Hana Pay, Toss, Purple GLN, and KB Star Banking. In Vietnam, local currency can be withdrawn at BIDV Bank ATMs, while in Laos, withdrawals can be made at BCEL Bank ATMs. Lee Seok, CEO of GLN, stated, "With the expansion of the QR withdrawal service in Japan, Vietnam, and Laos, more customers can enjoy cash withdrawal services abroad using familiar domestic apps without inconvenience. We will continue to lead the way in providing a simple withdrawal experience for travelers without the need for currency exchange or physical cards."* This article has been translated by AI. 2026-05-13 17:11:01

Hana Bank's GLN Expands Overseas QR Withdrawal Partnerships, Enabling Cash Withdrawals via KakaoPay in Japan Hana Bank's subsidiary, GLN International, is expanding its overseas QR withdrawal service in Japan, Vietnam, and Laos. This enhancement allows users of major domestic financial and platform apps to withdraw local currency without the need for currency exchange. The expansion focuses on the Japanese market, increasing the number of partner app channels from three to seven. Notably, KakaoPay, which enjoys high usage rates in Japan's mobile payment sector, has been added to the list of domestic partner apps. As a result, travelers to Japan can now access QR withdrawal services through not only Hana OneQ, Hana Money, and Toss apps but also Hana Pay, KakaoPay, Purple GLN, and KB Star Banking apps. Withdrawals can be made at Seven-Eleven convenience store ATMs and Seven Bank ATMs located in airports throughout Japan. QR payments are also accepted at various merchants, including convenience stores, clothing shops, and health and beauty stores. In Vietnam and Laos, users can access QR withdrawal services through six apps: Hana OneQ, Hana Money, Hana Pay, Toss, Purple GLN, and KB Star Banking. In Vietnam, local currency can be withdrawn at BIDV Bank ATMs, while in Laos, withdrawals can be made at BCEL Bank ATMs. Lee Seok, CEO of GLN, stated, "With the expansion of the QR withdrawal service in Japan, Vietnam, and Laos, more customers can enjoy cash withdrawal services abroad using familiar domestic apps without inconvenience. We will continue to lead the way in providing a simple withdrawal experience for travelers without the need for currency exchange or physical cards."* This article has been translated by AI. 2026-05-13 17:11:01 -

Increased Inclusion, Greater Burden: Rising Costs of Expanded Financial Support As the banking sector expands its inclusive finance initiatives to support vulnerable borrowers, concerns are growing about the financial burden on institutions. While there is consensus within the financial community on the need to assist disadvantaged groups, there are fears that performance metrics for inclusive finance could become a new standard for oversight and evaluation. On May 6, President Lee Jae-myung raised this issue during a Cabinet meeting, asking Financial Services Commission Chairman Lee Ok-keun if there was a way to evaluate how well financial institutions are implementing inclusive finance and to provide incentives or penalties based on that performance. He expressed concern that the current system relies too heavily on the goodwill of financial companies. This comment suggests a potential shift toward incorporating the performance of inclusive finance for low- and medium-credit borrowers into the evaluation and management guidelines for financial institutions. The atmosphere in the financial sector indicates that this could signal a move beyond mere recommendations to a more structured oversight and evaluation system. Banks have already invested significant resources into expanding support for vulnerable borrowers. The trend of increasing the scale of long-term delinquent loan write-offs and policy-based financial support is evident. This year, the total amount of special bonds scheduled for write-off is estimated at 335.1 billion won, with Shinhan Bank accounting for the largest share at 269.4 billion won, followed by KB Kookmin Bank at 33.5 billion won and Woori Bank at 32.2 billion won. There is also a surge in demand for policy financing targeting young people, who often lack sufficient credit history to access traditional financial systems. The 'Youth Future Connection Loan,' a notable public-private partnership in inclusive finance, has seen 4.75 billion won disbursed within a month of its launch in March, achieving 134% of its initial target. The average daily application rate reached about 1,700. The funding for this initiative comes from contributions of 100 billion won each from KB, Shinhan, and Woori Financial. In addition, banks are strengthening their support measures for vulnerable groups. KB Kookmin Bank plans to introduce a program this month that allows low-credit individual business owners to use interest payments on loans exceeding 5% to reduce their principal repayment burden. It is expected that over 10,000 individuals will benefit from this financial relief. Shinhan Bank has also been implementing a program since January 30 that refunds interest exceeding 5% for individual business customers. Additionally, a 'refinancing loan' aimed at helping customers switch from high-interest loans at savings banks to bank loans is set to launch in the first half of the year. However, the expansion of inclusive finance is increasing the financial burden on banks. In addition to their own programs, banks are participating in various public funding initiatives. Contributions to the Korea Inclusive Finance Agency have risen from 434.8 billion won last year to 632.1 billion won this year. The scale of policy-based low-income financial support is also expected to grow from 5.6 trillion won in 2024 to 7.2 trillion won this year, marking a 28.5% increase. The amount supplied in just the first two months of this year reached 2 trillion won. While these measures aim to alleviate the debt burden of vulnerable groups and support credit recovery, some critics argue that the policy burden is becoming excessively concentrated on private financial institutions. There are concerns that inclusive finance could devolve into a mere competition for supply metrics rather than providing genuine support for self-sufficiency. Evaluating success solely based on the scale of supply or debt relief could lead to superficial assistance and increased defaults. A financial sector representative stated, "There is a need for a system that evaluates inclusive finance based on actual self-sufficiency outcomes, such as normal repayment rates, the rate of return to economic activity after credit recovery, and re-delinquency rates. If the expansion of support continues, the burden on financial institutions will accumulate, ultimately passing those costs onto consumers."* This article has been translated by AI. 2026-05-12 03:57:45

Increased Inclusion, Greater Burden: Rising Costs of Expanded Financial Support As the banking sector expands its inclusive finance initiatives to support vulnerable borrowers, concerns are growing about the financial burden on institutions. While there is consensus within the financial community on the need to assist disadvantaged groups, there are fears that performance metrics for inclusive finance could become a new standard for oversight and evaluation. On May 6, President Lee Jae-myung raised this issue during a Cabinet meeting, asking Financial Services Commission Chairman Lee Ok-keun if there was a way to evaluate how well financial institutions are implementing inclusive finance and to provide incentives or penalties based on that performance. He expressed concern that the current system relies too heavily on the goodwill of financial companies. This comment suggests a potential shift toward incorporating the performance of inclusive finance for low- and medium-credit borrowers into the evaluation and management guidelines for financial institutions. The atmosphere in the financial sector indicates that this could signal a move beyond mere recommendations to a more structured oversight and evaluation system. Banks have already invested significant resources into expanding support for vulnerable borrowers. The trend of increasing the scale of long-term delinquent loan write-offs and policy-based financial support is evident. This year, the total amount of special bonds scheduled for write-off is estimated at 335.1 billion won, with Shinhan Bank accounting for the largest share at 269.4 billion won, followed by KB Kookmin Bank at 33.5 billion won and Woori Bank at 32.2 billion won. There is also a surge in demand for policy financing targeting young people, who often lack sufficient credit history to access traditional financial systems. The 'Youth Future Connection Loan,' a notable public-private partnership in inclusive finance, has seen 4.75 billion won disbursed within a month of its launch in March, achieving 134% of its initial target. The average daily application rate reached about 1,700. The funding for this initiative comes from contributions of 100 billion won each from KB, Shinhan, and Woori Financial. In addition, banks are strengthening their support measures for vulnerable groups. KB Kookmin Bank plans to introduce a program this month that allows low-credit individual business owners to use interest payments on loans exceeding 5% to reduce their principal repayment burden. It is expected that over 10,000 individuals will benefit from this financial relief. Shinhan Bank has also been implementing a program since January 30 that refunds interest exceeding 5% for individual business customers. Additionally, a 'refinancing loan' aimed at helping customers switch from high-interest loans at savings banks to bank loans is set to launch in the first half of the year. However, the expansion of inclusive finance is increasing the financial burden on banks. In addition to their own programs, banks are participating in various public funding initiatives. Contributions to the Korea Inclusive Finance Agency have risen from 434.8 billion won last year to 632.1 billion won this year. The scale of policy-based low-income financial support is also expected to grow from 5.6 trillion won in 2024 to 7.2 trillion won this year, marking a 28.5% increase. The amount supplied in just the first two months of this year reached 2 trillion won. While these measures aim to alleviate the debt burden of vulnerable groups and support credit recovery, some critics argue that the policy burden is becoming excessively concentrated on private financial institutions. There are concerns that inclusive finance could devolve into a mere competition for supply metrics rather than providing genuine support for self-sufficiency. Evaluating success solely based on the scale of supply or debt relief could lead to superficial assistance and increased defaults. A financial sector representative stated, "There is a need for a system that evaluates inclusive finance based on actual self-sufficiency outcomes, such as normal repayment rates, the rate of return to economic activity after credit recovery, and re-delinquency rates. If the expansion of support continues, the burden on financial institutions will accumulate, ultimately passing those costs onto consumers."* This article has been translated by AI. 2026-05-12 03:57:45 -

Household Loans Decline as Major Banks Tighten Lending Practices Household loans from major banks have seen an unprecedented decline as financial authorities tighten their management policies. While the growth rate of loans has slowed, concerns are rising that access to funds for genuine borrowers and those with lower credit ratings may be restricted. On May 11, data received by Lee In-young, a member of the National Assembly from the Democratic Party, from the Financial Supervisory Service revealed that KB Kookmin Bank's loan performance at the end of the first quarter was recorded at -178.0% compared to its annual loan growth target (excluding policy-based products). KB Kookmin Bank had set a household loan growth target of 909.2 billion won for this year, but instead saw a decrease of 1.6143 trillion won. The bank exceeded its loan target last year, resulting in penalties this year. Other banks are experiencing similar situations. NH Nonghyup Bank had a growth target of 870 billion won but reported a decrease of 1.3551 trillion won (-156.0%) by the end of the first quarter. Shinhan Bank, aiming for a target of 850 billion won, saw a reduction of 1.5896 trillion won (-187.0%). Hana Bank and Woori Bank reported decreases of 1.5402 trillion won and 344.7 billion won, respectively, marking -175.0% and -41.7% against their targets. Banks appear to have adopted a conservative approach to lending until the total household loan management targets were finalized in April. The overall household loan growth target for this year is set at 1.5%, lower than last year's 1.7%. The five major banks are required to adhere to stricter management, limiting their growth rate to around 1%. Additionally, authorities have established separate management targets for mortgage loans this year, setting ratios based on each bank's past performance in this area. With the introduction of monthly and quarterly management systems, banks are now required to adjust their lending speeds regularly. Ongoing real estate loan regulations have also contributed to the overall reduction in loan amounts. Internet-only banks have generally followed a conservative trend as well. K-Bank has a target of 667.3 billion won but reported a decrease of 223.7 billion won (-33.5%) in the first quarter, while Toss Bank executed only 370 million won out of its 550.2 billion won target (7.0%). However, the ongoing conservative lending stance in the financial sector raises concerns that genuine borrowers, particularly those with lower credit ratings, may face diminished opportunities for loans. Lee In-young cautioned, "If banks focus solely on total management targets and raise their thresholds uniformly, the burden will inevitably fall on lower-credit borrowers and those in need of loans for living expenses." 2026-05-11 15:57:09

Household Loans Decline as Major Banks Tighten Lending Practices Household loans from major banks have seen an unprecedented decline as financial authorities tighten their management policies. While the growth rate of loans has slowed, concerns are rising that access to funds for genuine borrowers and those with lower credit ratings may be restricted. On May 11, data received by Lee In-young, a member of the National Assembly from the Democratic Party, from the Financial Supervisory Service revealed that KB Kookmin Bank's loan performance at the end of the first quarter was recorded at -178.0% compared to its annual loan growth target (excluding policy-based products). KB Kookmin Bank had set a household loan growth target of 909.2 billion won for this year, but instead saw a decrease of 1.6143 trillion won. The bank exceeded its loan target last year, resulting in penalties this year. Other banks are experiencing similar situations. NH Nonghyup Bank had a growth target of 870 billion won but reported a decrease of 1.3551 trillion won (-156.0%) by the end of the first quarter. Shinhan Bank, aiming for a target of 850 billion won, saw a reduction of 1.5896 trillion won (-187.0%). Hana Bank and Woori Bank reported decreases of 1.5402 trillion won and 344.7 billion won, respectively, marking -175.0% and -41.7% against their targets. Banks appear to have adopted a conservative approach to lending until the total household loan management targets were finalized in April. The overall household loan growth target for this year is set at 1.5%, lower than last year's 1.7%. The five major banks are required to adhere to stricter management, limiting their growth rate to around 1%. Additionally, authorities have established separate management targets for mortgage loans this year, setting ratios based on each bank's past performance in this area. With the introduction of monthly and quarterly management systems, banks are now required to adjust their lending speeds regularly. Ongoing real estate loan regulations have also contributed to the overall reduction in loan amounts. Internet-only banks have generally followed a conservative trend as well. K-Bank has a target of 667.3 billion won but reported a decrease of 223.7 billion won (-33.5%) in the first quarter, while Toss Bank executed only 370 million won out of its 550.2 billion won target (7.0%). However, the ongoing conservative lending stance in the financial sector raises concerns that genuine borrowers, particularly those with lower credit ratings, may face diminished opportunities for loans. Lee In-young cautioned, "If banks focus solely on total management targets and raise their thresholds uniformly, the burden will inevitably fall on lower-credit borrowers and those in need of loans for living expenses." 2026-05-11 15:57:09 -

Woori Bank Issues 300 Billion Won Green Bonds, Leading the Banking Sector Woori Bank has become the first commercial bank this year to issue Korean-style green bonds, accelerating its efforts in ESG finance. The bank raised a record 300 billion won, reinforcing its position as a leader in the green finance market. On May 11, Woori Bank announced that it issued a total of 300 billion won in Korean-style green bonds through the "Korean-style Green Bond Issuance Interest Support Program" organized by the Ministry of Climate, Energy, and Environment and the Korea Environmental Industry and Technology Institute. The issuance consists of 150 billion won with a three-year maturity and 150 billion won with a one-year maturity. This marks the first instance among commercial banks this year and is the largest single issuance to date. Following the issuance of 150 billion won in Korean-style green bonds in both 2024 and 2025, this latest 300 billion won issuance brings the bank's total to 600 billion won. This amount positions Woori Bank as the leader in cumulative issuance of Korean-style green bonds among banks since 2022. The funds raised will be fully allocated to support eco-friendly projects, including solar and wind energy production and waste-to-energy recovery projects. Woori Bank plans to solidify its leading position in the green finance market and accelerate its expansion in ESG finance. Kang Han-na, head of Woori Bank's funding department, stated, "This issuance of Korean-style green bonds is an opportunity to reaffirm Woori Bank's commitment to ESG management in the market. As the role of finance in the transition to eco-friendliness becomes increasingly important, we will continue our responsible ESG initiatives."* This article has been translated by AI. 2026-05-11 14:16:16

Woori Bank Issues 300 Billion Won Green Bonds, Leading the Banking Sector Woori Bank has become the first commercial bank this year to issue Korean-style green bonds, accelerating its efforts in ESG finance. The bank raised a record 300 billion won, reinforcing its position as a leader in the green finance market. On May 11, Woori Bank announced that it issued a total of 300 billion won in Korean-style green bonds through the "Korean-style Green Bond Issuance Interest Support Program" organized by the Ministry of Climate, Energy, and Environment and the Korea Environmental Industry and Technology Institute. The issuance consists of 150 billion won with a three-year maturity and 150 billion won with a one-year maturity. This marks the first instance among commercial banks this year and is the largest single issuance to date. Following the issuance of 150 billion won in Korean-style green bonds in both 2024 and 2025, this latest 300 billion won issuance brings the bank's total to 600 billion won. This amount positions Woori Bank as the leader in cumulative issuance of Korean-style green bonds among banks since 2022. The funds raised will be fully allocated to support eco-friendly projects, including solar and wind energy production and waste-to-energy recovery projects. Woori Bank plans to solidify its leading position in the green finance market and accelerate its expansion in ESG finance. Kang Han-na, head of Woori Bank's funding department, stated, "This issuance of Korean-style green bonds is an opportunity to reaffirm Woori Bank's commitment to ESG management in the market. As the role of finance in the transition to eco-friendliness becomes increasingly important, we will continue our responsible ESG initiatives."* This article has been translated by AI. 2026-05-11 14:16:16 -

Banks Embrace Inclusive Finance Amid Caution as Authorities Push for Public Finance The financial authorities are set to launch an 'Inclusive Finance Task Force' soon, marking a significant step toward publicizing the financial sector's role as emphasized by President Lee Jae-myung. While the heads of major commercial banks express support for the government's initiative to expand inclusive finance, they also voice concerns about uniform target setting and evaluations focused on short-term results. According to the financial sector on May 10, the Financial Services Commission plans to hold a kickoff meeting for the Inclusive Finance Task Force (tentative name) this month. Specific preparations, including the formation of subcommittees and agenda discussions, are currently underway. The establishment of the task force follows recent strong expressions from the Blue House regarding the public functions of finance. President Lee pointed out during a Cabinet meeting on May 6 that he feels “the public nature of financial institutions is too weak.” Kim Yong-beom, head of the Blue House Policy Office, also criticized the issue of financial exclusion for low- and medium-credit individuals as a “structural contradiction that has been meticulously neglected.” The task force is expected to discuss a wide range of topics, primarily focusing on reforming the credit evaluation system. Changes are anticipated in the current credit assessment methods, which fail to adequately reflect the future potential of individual borrowers. Additionally, the task force will address issues related to the existing lending system, which primarily serves high-credit borrowers while imposing barriers for those with medium to low credit scores. In response to the government's direction, the heads of major commercial banks generally expressed agreement. A survey conducted by Yonhap News among five major bank leaders, including Lee Hwan-joo of KB Kookmin Bank, Jung Sang-hyuk of Shinhan Bank, Lee Ho-sung of Hana Bank, Jeong Jin-wan of Woori Bank, and Kang Tae-young of NH Nonghyup Bank, revealed that none of the bank heads denied the public nature of banks. All bank leaders acknowledged that “banks have a quasi-public institution nature,” stating, “While banks operate as businesses based on market principles, they conduct operations on a public foundation that includes state authorization, trust, depositor protection, and financial stability, which imposes a much higher level of public nature and social responsibility than ordinary companies.” Regarding the criticism that vulnerable borrowers are excluded from the existing credit evaluation system, they noted, “It is time to evolve from a simple selective finance model to a data and technology-based 'discovery finance.' We are enhancing financial accessibility through the advancement of credit evaluation by combining existing financial data with non-financial alternative data.” However, there were overall concerns about evaluating how much inclusive finance has been implemented and the potential for profit or loss based on that evaluation. One bank leader pointed out, “If the expansion of uniform inclusive finance is evaluated solely based on loan volume or interest rates, it could ultimately burden the real economy and increase risks across the market in the long run.” Other bank leaders also expressed worries that “excessive interest rate reductions or debt relief could create a sense of relative deprivation and moral hazard for diligent repayers,” and that “a focus on short-term results could distort market functions and worsen soundness,” potentially burdening the autonomy and stability of financial institutions.* This article has been translated by AI. 2026-05-11 02:55:10

Banks Embrace Inclusive Finance Amid Caution as Authorities Push for Public Finance The financial authorities are set to launch an 'Inclusive Finance Task Force' soon, marking a significant step toward publicizing the financial sector's role as emphasized by President Lee Jae-myung. While the heads of major commercial banks express support for the government's initiative to expand inclusive finance, they also voice concerns about uniform target setting and evaluations focused on short-term results. According to the financial sector on May 10, the Financial Services Commission plans to hold a kickoff meeting for the Inclusive Finance Task Force (tentative name) this month. Specific preparations, including the formation of subcommittees and agenda discussions, are currently underway. The establishment of the task force follows recent strong expressions from the Blue House regarding the public functions of finance. President Lee pointed out during a Cabinet meeting on May 6 that he feels “the public nature of financial institutions is too weak.” Kim Yong-beom, head of the Blue House Policy Office, also criticized the issue of financial exclusion for low- and medium-credit individuals as a “structural contradiction that has been meticulously neglected.” The task force is expected to discuss a wide range of topics, primarily focusing on reforming the credit evaluation system. Changes are anticipated in the current credit assessment methods, which fail to adequately reflect the future potential of individual borrowers. Additionally, the task force will address issues related to the existing lending system, which primarily serves high-credit borrowers while imposing barriers for those with medium to low credit scores. In response to the government's direction, the heads of major commercial banks generally expressed agreement. A survey conducted by Yonhap News among five major bank leaders, including Lee Hwan-joo of KB Kookmin Bank, Jung Sang-hyuk of Shinhan Bank, Lee Ho-sung of Hana Bank, Jeong Jin-wan of Woori Bank, and Kang Tae-young of NH Nonghyup Bank, revealed that none of the bank heads denied the public nature of banks. All bank leaders acknowledged that “banks have a quasi-public institution nature,” stating, “While banks operate as businesses based on market principles, they conduct operations on a public foundation that includes state authorization, trust, depositor protection, and financial stability, which imposes a much higher level of public nature and social responsibility than ordinary companies.” Regarding the criticism that vulnerable borrowers are excluded from the existing credit evaluation system, they noted, “It is time to evolve from a simple selective finance model to a data and technology-based 'discovery finance.' We are enhancing financial accessibility through the advancement of credit evaluation by combining existing financial data with non-financial alternative data.” However, there were overall concerns about evaluating how much inclusive finance has been implemented and the potential for profit or loss based on that evaluation. One bank leader pointed out, “If the expansion of uniform inclusive finance is evaluated solely based on loan volume or interest rates, it could ultimately burden the real economy and increase risks across the market in the long run.” Other bank leaders also expressed worries that “excessive interest rate reductions or debt relief could create a sense of relative deprivation and moral hazard for diligent repayers,” and that “a focus on short-term results could distort market functions and worsen soundness,” potentially burdening the autonomy and stability of financial institutions.* This article has been translated by AI. 2026-05-11 02:55:10 -

KB Kookmin Bank to Automatically Apply Interest Over 5% to Principal Repayment KB Kookmin Bank is launching a financial support program aimed at alleviating the interest burden for individual business owners. The initiative will automatically apply a portion of the interest exceeding 5% on business loans toward principal repayment, thereby reducing both interest and principal repayment obligations. On May 10, KB Kookmin Bank announced that it will implement a program that utilizes the interest amount exceeding 5% on individual business loans to reduce debt burdens. This program is set to begin later this month as part of KB Financial Group's "KB Kookmin Happiness Hope Project." When individual business owners extend their existing loans and the interest rate exceeds 5%, the excess interest amount (up to 4 percentage points) will be automatically applied to the loan principal repayment. As a result, the loan balance will decrease, which is expected to lessen the future interest burden for individual business owners, helping to alleviate their financial costs. Additionally, there will be no prepayment fees for using the excess interest payment toward principal repayment. The program is targeted at individual business owners with low credit ratings who hold won-denominated loans with interest rates exceeding 5%. Certain sectors, such as real estate, and customers with overdue loans will be excluded from this initiative. A representative from KB Kookmin Bank stated, "We expect that more than 10,000 individual business owners will benefit from this program, and we will continue to fulfill our social responsibility through various inclusive finance practices for vulnerable groups." 2026-05-10 11:24:33

KB Kookmin Bank to Automatically Apply Interest Over 5% to Principal Repayment KB Kookmin Bank is launching a financial support program aimed at alleviating the interest burden for individual business owners. The initiative will automatically apply a portion of the interest exceeding 5% on business loans toward principal repayment, thereby reducing both interest and principal repayment obligations. On May 10, KB Kookmin Bank announced that it will implement a program that utilizes the interest amount exceeding 5% on individual business loans to reduce debt burdens. This program is set to begin later this month as part of KB Financial Group's "KB Kookmin Happiness Hope Project." When individual business owners extend their existing loans and the interest rate exceeds 5%, the excess interest amount (up to 4 percentage points) will be automatically applied to the loan principal repayment. As a result, the loan balance will decrease, which is expected to lessen the future interest burden for individual business owners, helping to alleviate their financial costs. Additionally, there will be no prepayment fees for using the excess interest payment toward principal repayment. The program is targeted at individual business owners with low credit ratings who hold won-denominated loans with interest rates exceeding 5%. Certain sectors, such as real estate, and customers with overdue loans will be excluded from this initiative. A representative from KB Kookmin Bank stated, "We expect that more than 10,000 individual business owners will benefit from this program, and we will continue to fulfill our social responsibility through various inclusive finance practices for vulnerable groups." 2026-05-10 11:24:33 -

Should You Switch to the New 5th Generation Health Insurance? The launch of the 5th generation health insurance is complicating decisions for current policyholders. While premiums have significantly decreased, changes in coverage structures mean that the extent of coverage can vary based on the treatments received. According to the Financial Services Commission on May 9, the key feature of the 5th generation health insurance is the enhancement of coverage for severe illnesses, while reducing coverage for non-severe, non-covered treatments. Premiums are expected to be about 30% lower than the 4th generation and over 50% lower than the 1st and 2nd generations. However, when choosing health insurance, it is essential to consider not only the premium levels but also past insurance payouts and future healthcare usage plans. For existing policyholders, if the expected insurance payouts exceed the annual premium, it is advantageous to maintain the current plan. Conversely, if anticipated payouts are lower than the premium, opting for reduced coverage to lower costs may be a sensible choice. For instance, a policyholder paying approximately 170,000 won per month for a 1st generation health insurance plan could see their monthly premium drop to around 20,000 won with a transition discount. Even after the three-year discount period, the premium would be about 40,000 won. By enrolling in a 'selective discount clause' that excludes low-usage items like physical therapy or non-covered injections, premiums could be reduced by 40% to around 100,000 won. However, switching to the 5th generation is most beneficial for those who rarely visit hospitals and find the high premiums of the 1st generation burdensome. If a policyholder with a 1st or 2nd generation plan anticipates treatment for a severe illness, it is advisable to maintain the existing coverage for broader protection, and consider switching to a selective discount clause after treatment when healthcare usage is expected to decrease. For those frequently visiting hospitals for treatments like physical therapy or extracorporeal shockwave therapy, it may be more advantageous to retain the existing health insurance. Particularly, the 1st generation plans often have lower out-of-pocket costs and favorable coverage conditions, so it is crucial to evaluate overall healthcare usage patterns and the extent of non-covered treatments before deciding to switch. Park Chang-sik, a senior official at Dongyang Life Insurance, stated, "For policyholders who do not have immediate plans for hospital visits and are not overly burdened by premiums, it is advisable to monitor future situations before hastily switching to the 5th generation. Conversely, those facing increased premium burdens due to aging should compare the cost-saving benefits and coverage structures before making a decision."* This article has been translated by AI. 2026-05-09 07:04:25

Should You Switch to the New 5th Generation Health Insurance? The launch of the 5th generation health insurance is complicating decisions for current policyholders. While premiums have significantly decreased, changes in coverage structures mean that the extent of coverage can vary based on the treatments received. According to the Financial Services Commission on May 9, the key feature of the 5th generation health insurance is the enhancement of coverage for severe illnesses, while reducing coverage for non-severe, non-covered treatments. Premiums are expected to be about 30% lower than the 4th generation and over 50% lower than the 1st and 2nd generations. However, when choosing health insurance, it is essential to consider not only the premium levels but also past insurance payouts and future healthcare usage plans. For existing policyholders, if the expected insurance payouts exceed the annual premium, it is advantageous to maintain the current plan. Conversely, if anticipated payouts are lower than the premium, opting for reduced coverage to lower costs may be a sensible choice. For instance, a policyholder paying approximately 170,000 won per month for a 1st generation health insurance plan could see their monthly premium drop to around 20,000 won with a transition discount. Even after the three-year discount period, the premium would be about 40,000 won. By enrolling in a 'selective discount clause' that excludes low-usage items like physical therapy or non-covered injections, premiums could be reduced by 40% to around 100,000 won. However, switching to the 5th generation is most beneficial for those who rarely visit hospitals and find the high premiums of the 1st generation burdensome. If a policyholder with a 1st or 2nd generation plan anticipates treatment for a severe illness, it is advisable to maintain the existing coverage for broader protection, and consider switching to a selective discount clause after treatment when healthcare usage is expected to decrease. For those frequently visiting hospitals for treatments like physical therapy or extracorporeal shockwave therapy, it may be more advantageous to retain the existing health insurance. Particularly, the 1st generation plans often have lower out-of-pocket costs and favorable coverage conditions, so it is crucial to evaluate overall healthcare usage patterns and the extent of non-covered treatments before deciding to switch. Park Chang-sik, a senior official at Dongyang Life Insurance, stated, "For policyholders who do not have immediate plans for hospital visits and are not overly burdened by premiums, it is advisable to monitor future situations before hastily switching to the 5th generation. Conversely, those facing increased premium burdens due to aging should compare the cost-saving benefits and coverage structures before making a decision."* This article has been translated by AI. 2026-05-09 07:04:25 -

SK Hynix Doubles in Four Months, But Bank Stocks Lag in KOSPI Rally The KOSPI index surged past 7500, driven by a spike in semiconductor stocks, but bank shares remain sidelined in the market rally. Analysts attribute the limited upward momentum to concerns over financial stability and policy uncertainties despite record earnings. On May 7, Samsung Electronics closed at 271,500 won, up 5,500 won (2.07%) from the previous day, marking a 111.2% increase since the start of the year. Similarly, SK Hynix rose from 677,000 won to 1,654,000 won, a 144.3% jump. The semiconductor sector is leading the KOSPI's overall rise, fueled by expectations of increased demand for artificial intelligence and foreign investment. In contrast, bank stocks have lagged behind. While the KOSPI has risen 73.7% this year, the KRX Bank Index has only increased by 25.1%. Major financial groups saw limited gains, with KB Financial rising 30.7% from 123,300 won to 161,200 won, and Shinhan Financial increasing 29.1% from 76,600 won to 98,900 won, falling short of the KOSPI's growth. Despite the recent strong performance of the four major financial groups (KB, Shinhan, Hana, and Woori), which reported a combined net profit of 5.33 trillion won in the first quarter—an 8.1% increase year-on-year—analysts note that the growth in stock prices has been muted. This is partly due to the market already pricing in the banks' shareholder return strategies, including stock buybacks and increased dividends, as investor interest shifts toward high-growth sectors like AI and semiconductors. Concerns over rising delinquency rates and increased loan loss provisions have also heightened worries about financial stability, while the management of household loans poses additional challenges to bank profitability. Recent comments from President Yoon Suk Yeol and Kim Yong-beom, head of the Presidential Policy Office, criticizing the current credit rating system and interest rate structure have further dampened investor sentiment. However, analysts maintain that the fundamentals of bank stocks remain solid. Given the trends in market interest rates and lending regulations, there is a strong likelihood of continued improvement in net interest margins (NIM) in the second quarter. While short-term underperformance may persist, a reduction in market concentration could highlight the undervalued appeal of bank stocks. Hana Securities analyst Choi Jeong-wook stated, "If concerns about interest rates grow, the defensive appeal of bank stocks may resurface, and we expect them to outperform the market this month."* This article has been translated by AI. 2026-05-07 16:20:19

SK Hynix Doubles in Four Months, But Bank Stocks Lag in KOSPI Rally The KOSPI index surged past 7500, driven by a spike in semiconductor stocks, but bank shares remain sidelined in the market rally. Analysts attribute the limited upward momentum to concerns over financial stability and policy uncertainties despite record earnings. On May 7, Samsung Electronics closed at 271,500 won, up 5,500 won (2.07%) from the previous day, marking a 111.2% increase since the start of the year. Similarly, SK Hynix rose from 677,000 won to 1,654,000 won, a 144.3% jump. The semiconductor sector is leading the KOSPI's overall rise, fueled by expectations of increased demand for artificial intelligence and foreign investment. In contrast, bank stocks have lagged behind. While the KOSPI has risen 73.7% this year, the KRX Bank Index has only increased by 25.1%. Major financial groups saw limited gains, with KB Financial rising 30.7% from 123,300 won to 161,200 won, and Shinhan Financial increasing 29.1% from 76,600 won to 98,900 won, falling short of the KOSPI's growth. Despite the recent strong performance of the four major financial groups (KB, Shinhan, Hana, and Woori), which reported a combined net profit of 5.33 trillion won in the first quarter—an 8.1% increase year-on-year—analysts note that the growth in stock prices has been muted. This is partly due to the market already pricing in the banks' shareholder return strategies, including stock buybacks and increased dividends, as investor interest shifts toward high-growth sectors like AI and semiconductors. Concerns over rising delinquency rates and increased loan loss provisions have also heightened worries about financial stability, while the management of household loans poses additional challenges to bank profitability. Recent comments from President Yoon Suk Yeol and Kim Yong-beom, head of the Presidential Policy Office, criticizing the current credit rating system and interest rate structure have further dampened investor sentiment. However, analysts maintain that the fundamentals of bank stocks remain solid. Given the trends in market interest rates and lending regulations, there is a strong likelihood of continued improvement in net interest margins (NIM) in the second quarter. While short-term underperformance may persist, a reduction in market concentration could highlight the undervalued appeal of bank stocks. Hana Securities analyst Choi Jeong-wook stated, "If concerns about interest rates grow, the defensive appeal of bank stocks may resurface, and we expect them to outperform the market this month."* This article has been translated by AI. 2026-05-07 16:20:19 -

Woori Bank to Lead Investment in Government Future City Fund for First-Generation New Town Redevelopment Woori Bank said Wednesday it will participate as the largest investor in the government-backed “Future City Fund,” aimed at supporting redevelopment projects in first-generation new towns. The policy fund was created to provide stable financing for aging apartment complexes in areas such as Bundang and Ilsan, where reconstruction is being pursued. It is designed to supply essential early-stage project costs from the planning stage, helping projects move forward more smoothly. Woori Bank will commit 480 billion won to the first master fund, which totals 600 billion won, as part of a broader 12 trillion won Future City Fund initiative. Linked to guarantees from the Korea Housing & Urban Guarantee Corp. (HUG), the funding will be provided at low interest rates, up to 20 billion won per project site, the bank said. Woori Asset Management will run the fund. The selection will allow the firm to expand beyond traditional asset management into alternative investments and large policy funds, it said. Major investors, including Woori Bank, have completed investment agreements to establish the fund. It will operate on a capital-call basis, with money drawn and deployed when needed. Actual disbursements will begin after the first borrower project is chosen among designated leading districts in the first-generation new towns and requests financial support. Lee Jin-kyung, a team leader in Woori Bank’s structured finance department, said the bank’s participation will help ease early funding shortages for aging new-town redevelopment and provide a more stable foundation for projects. He said the bank will continue expanding structured finance tied to policy financing. 2026-05-07 13:55:47

Woori Bank to Lead Investment in Government Future City Fund for First-Generation New Town Redevelopment Woori Bank said Wednesday it will participate as the largest investor in the government-backed “Future City Fund,” aimed at supporting redevelopment projects in first-generation new towns. The policy fund was created to provide stable financing for aging apartment complexes in areas such as Bundang and Ilsan, where reconstruction is being pursued. It is designed to supply essential early-stage project costs from the planning stage, helping projects move forward more smoothly. Woori Bank will commit 480 billion won to the first master fund, which totals 600 billion won, as part of a broader 12 trillion won Future City Fund initiative. Linked to guarantees from the Korea Housing & Urban Guarantee Corp. (HUG), the funding will be provided at low interest rates, up to 20 billion won per project site, the bank said. Woori Asset Management will run the fund. The selection will allow the firm to expand beyond traditional asset management into alternative investments and large policy funds, it said. Major investors, including Woori Bank, have completed investment agreements to establish the fund. It will operate on a capital-call basis, with money drawn and deployed when needed. Actual disbursements will begin after the first borrower project is chosen among designated leading districts in the first-generation new towns and requests financial support. Lee Jin-kyung, a team leader in Woori Bank’s structured finance department, said the bank’s participation will help ease early funding shortages for aging new-town redevelopment and provide a more stable foundation for projects. He said the bank will continue expanding structured finance tied to policy financing. 2026-05-07 13:55:47