SEOUL, April 23 (AJP) -Regardless of the headline figures, SK hynix reigns as the most profitable chipmaker in the world and will likely stay so through the year as it consolidates leadership in high-bandwidth memory (HBM) critical to the AI transition through aggressive spending from its enhanced firepower.

The Korean pure-play memory maker will test upgraded HBM4E prototypes in the second half for potential rollout next year depending on client demand, according to executives during a conference call Thursday.

“The base die for HBM4E is progressing smoothly, using optimal technology to meet customer performance requirements,” the company said.

“The core die is being designed on a sixth-generation 10-nanometer-class (1c) process to address increasingly demanding performance needs.”

The company added that its 1c process has already reached mature yield levels ahead of mass production starting later this year, enabling it to deliver HBM4E with “stable performance and supply capacity.”

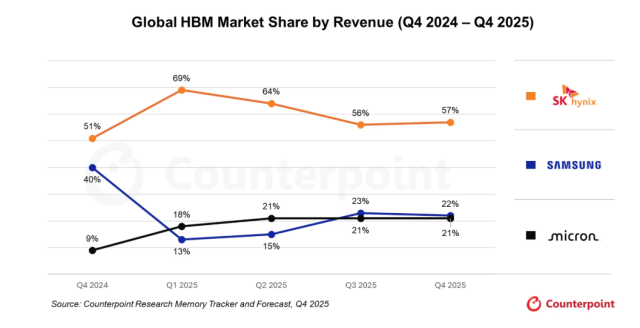

SK hynix, which pioneered HBM critical to Nvidia’s breakout AI chips, remains unrivaled in the premium segment, supported by overwhelming demand and long-term supply arrangements with hyperscale customers.

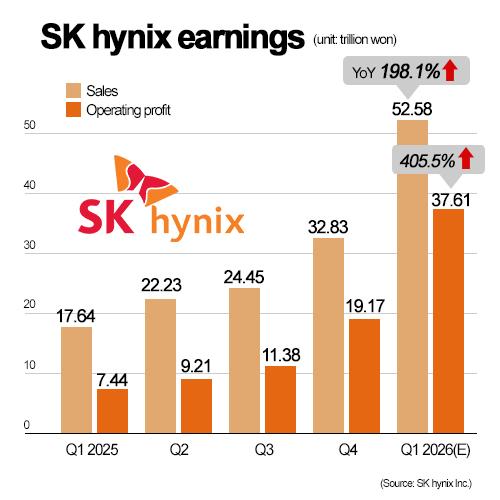

Its record first-quarter results underscore its edge from a high concentration of HBM products.

The company posted an operating margin of 72 percent, surpassing its previous high of 58 percent and outpacing TSMC’s roughly 58 percent and Samsung Electronics’ estimated 43 percent over the same period.

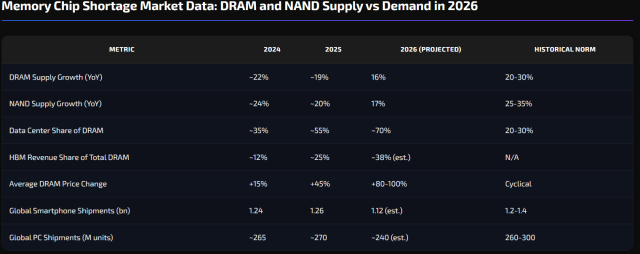

The earnings surge reflects a structural shift in the memory market. DRAM supply growth is projected to slow to the mid-teens in 2026, well below the historical norm of 20–30 percent, while NAND supply growth is also moderating.

At the same time, data center demand is rapidly absorbing supply, with its share of DRAM consumption expected to approach 70 percent this year, up sharply from about 35 percent in 2024.

HBM’s revenue share is also expanding quickly, estimated to reach nearly 40 percent of total DRAM this year, underscoring its central role in profitability.

The strong earnings were driven by surging demand for HBM — a key component in AI accelerators — alongside sharp price increases in conventional DRAM and NAND amid tight supply.

Industry data show DRAM contract prices jumped more than 90 percent on quarter in the first three months of the year, reflecting a supplier-driven market that has significantly boosted profitability.

The extraordinary dynamics in favor of the supply side will likely continue for some time, according to SK hynix.

“This increase in memory prices is not the result of a temporary supply-demand imbalance, but rather a structural shift in the market,” the company said, noting that AI demand is fundamentally reshaping pricing dynamics.

HBM accounted for around 30 percent of SK hynix’s DRAM shipments, with the remainder coming from conventional products such as DDR5 and LPDDR5X, which also benefited from the pricing upcycle.

Samsung Electronics is also seeing strong gains from memory, with analysts estimating its memory division posted operating margins of 60 to 70 percent.

However, its overall profitability remains lower due to weaker performance in other business segments, including foundry and consumer electronics.

The shift is being reinforced by a rapid reallocation of manufacturing capacity toward AI infrastructure. Hyperscale cloud providers such as Meta, Google, Microsoft and Amazon have secured long-term supply agreements, effectively locking in production at premium prices.

“Customers are prioritizing securing supply over price, and the growing importance of memory in AI computing is increasingly reflected in pricing,” the company said.

As a result, even as overall memory output grows, supply available for consumer devices continues to shrink, contributing to a tightening cycle that is expected to persist.

The scale of AI demand is further amplifying the imbalance. Nvidia’s latest AI systems consume hundreds of DRAM dies per unit, with a single rack requiring memory equivalent to that used in roughly 1,000 high-end smartphones.

SK hynix said it is accelerating investment to meet demand but warned that supply expansion will take time.

“Even under current strong demand conditions, there are clear limits to how quickly production capacity can be meaningfully expanded,” the company said, citing constraints from prior investment cuts and limited cleanroom availability.

The company plans to expand capital expenditure this year, including ramping up its Cheongju M15X facility and advancing the Yongin semiconductor cluster, while securing critical equipment to support long-term capacity to maintain its comfortable lead in the premium HBM market.

The red-hot earnings streak has bolstered its cashable assets by 19.4 trillion won from December to 54.3 trillion won as of March while debt was reduced to 19.3 trillion, translating into a net cash reserve of 35 trillion won.

Despite geopolitical risks from the Gulf crisis, SK hynix said its production outlook remains largely unaffected.

“We have already secured countermeasures against raw material and energy supply risks, and the impact on production is expected to be very limited,” the company said, citing diversified sourcing and long-term LNG contracts.

Shares of SK hynix fell 1.27 percent to 1,207,000 won on profit-taking from recent rally as of 1:40 p.m.

Copyright ⓒ Aju Press All rights reserved.