A market slump in derivative-linked products has begun to ease on the back of a rebound in global stocks and steadier interest rates, with issuance rising sharply in principal-protected derivative-linked bonds. Still, regulators said investor caution tied to past losses has not fully faded, underscoring the need to understand product structures before investing.

According to the Financial Supervisory Service on Tuesday, issuance of derivative-linked securities and bonds in 2025 totaled 94.9 trillion won, up 21.3 trillion won from a year earlier. Redemptions over the same period came to 81.2 trillion won, down 5.1 trillion won.

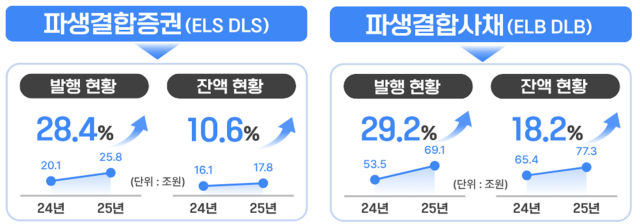

With issuance exceeding redemptions, the outstanding balance at year-end was tallied at 95.1 trillion won, recovering to the level seen at the end of 2023. The balance had fallen to 81.6 trillion won in 2024, the lowest since 2014 (84.1 trillion won), as demand slumped amid concerns over ELS losses following a sharp drop in Hong Kong’s H index and sales suspensions by major banks.

By product, both derivative-linked securities and derivative-linked bonds posted growth of about 30%. Issuance of derivative-linked securities rose 5.7 trillion won, or 28.6%, to 25.8 trillion won, led by index-linked ELS. Derivative-linked bond issuance increased 15.6 trillion won, or 29.2%, to 69.1 trillion won, largely reflecting stronger demand for principal-protected products in the retirement pension market.

The FSS data also showed shifts in product structure. Among derivative-linked securities, no-knock-in products still accounted for the majority at 60.0%, but that was down 7.3 percentage points from 67.3% a year earlier. For knock-in products, low knock-in structures made up 95.8%. All derivative-linked bonds were issued with no-knock-in structures.

Returns improved overall. In 2025, the annualized return on products redeemed early or at maturity was 6.4% for derivative-linked securities and 3.7% for derivative-linked bonds. A year earlier, the figures were -4.7% and 4.0%, respectively. By type, annualized returns were 7.8% for ELS, 2.1% for DLS, 4.0% for ELB and 3.3% for DLB, with equity-based products performing relatively better.

“Risk can increase as the number of underlying assets rises or as the offered yield gets higher, so investors should decide only after fully understanding the product structure,” an FSS official said. The official said the agency will closely monitor risk factors, including issuance trends, and guide financial firms to ensure investors receive adequate risk disclosures.

* This article has been translated by AI.

Copyright ⓒ Aju Press All rights reserved.