This sharp drop signifies more than just profit-taking; it indicates that the market is beginning to reassess fundamentals and macroeconomic realities.

As of May 14, the KOSPI's 50-day deviation had surged to 131%. Analysts noted, "During the dot-com bubble, the 50-day deviation reached 130%, followed by a short-term correction within 1 to 3 weeks," highlighting the clear signs of overheating. The recent AI and semiconductor boom had overshadowed interest rates, oil prices, and geopolitical risks, making the South Korean stock market one of the most overheated globally. However, financial markets ultimately revert to fundamentals such as earnings, interest rates, inflation, and exchange rates.

The core of this correction lies in inflation and the global bond market. The yield on the U.S. 10-year Treasury bond soared to 4.59%, reaching its highest level in nearly a year, while the 30-year yield exceeded 5.12%, the highest since 2007. Japan's 30-year bond yield surpassed 4% for the first time, and the UK's 30-year yield climbed to 5.85%, the highest since 1998.

The Wall Street Journal reported, "A sharp sell-off in Japanese and British bonds has spilled over into the U.S. market," marking a rare simultaneous disturbance in the global bond market. On the same day, South Korea's 10-year government bond yield jumped by 13.2 basis points to 4.217%, creating a typical risk-averse environment where stocks, bonds, and exchange rates all fluctuated simultaneously.

The turmoil in the bond market is clear. With the prolonged war in Iran pushing international oil prices back above $100 per barrel, the market has begun to recognize the reality of prolonged high interest rates. According to the Financial Supervisory Service, Brent crude has surged by 73.74% and WTI by 76.19% compared to the end of last year.

With approximately 20% of the world's oil maritime traffic passing through the Strait of Hormuz, the unresolved risks in the region could lead to rising logistics costs and energy prices, further fueling global inflation pressures. The CME FedWatch indicates that the likelihood of a 0.25 percentage point rate hike in December has jumped from 13.6% to 50% in just a week, reversing expectations for a rate cut by the Federal Reserve.

Additionally, a change in the Federal Reserve's leadership adds another variable. May 15 marked the last day of Jerome Powell's term, with Kevin Warsh taking over as the new chair. Société Générale stated, "The instability in the bond market will be the first test for Warsh's administration." The market is closely watching how the new chair manages expectations amid a potential resurgence of inflation.

These warning signals from the market have been ignored for too long. The recent U.S.-China summit failed to deliver a substantial breakthrough beyond restoring relations. Geopolitical risks surrounding Taiwan remain unchanged. Nevertheless, global markets have continued their overheated rally, relying solely on optimism surrounding AI.

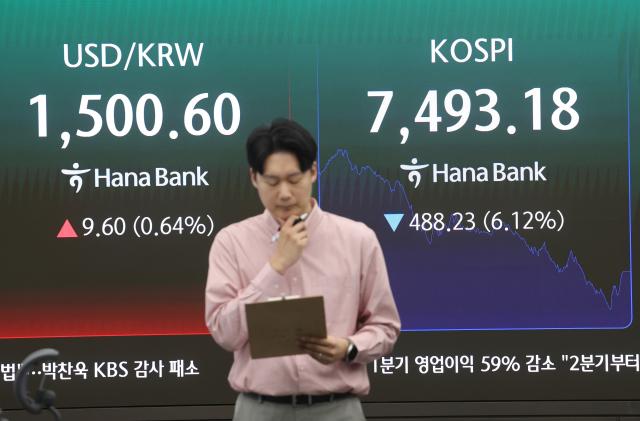

The shock to the South Korean market has been particularly severe. On the same day, Japan's Nikkei fell by 1.99% and Taiwan's market by 1.39%, while the KOSPI plummeted by over 6%. The won-dollar exchange rate surged to 1,500.8 won. Strengthening U.S.-China cooperation has diminished expectations for domestic semiconductor, power equipment, and solar sectors. Major semiconductor stocks that had previously boosted the index, such as Samsung Electronics (-8.61%) and SK Hynix (-7.66%), contributed to the decline.

Foreign capital outflows are also concerning. On May 15, foreign investors sold a net 6.3173 trillion won in the stock market, bringing the total net sales for the year to 98.2 trillion won. Foreign selling has continued for seven consecutive trading days. While AI and semiconductors had driven the market up, the resurgence of global interest rates and the dollar prompted foreign funds to exit first.

However, this correction should not be immediately interpreted as a collapse. The semiconductor industry and the AI investment cycle remain intact. Customer deposits still exceed 130 trillion won, indicating a favorable liquidity environment, and the KOSPI valuation is considered undervalued compared to major global markets.

Yet, the market is now factoring in not just growth stories but also interest rates and liquidity costs. In an environment of rising long-term rates, it becomes challenging to justify high valuations based solely on future expectations.

What is needed now is a return to fundamentals. The government and financial authorities should focus on stabilizing exchange rates and the bond market, managing excessive leverage and credit concentration, rather than merely defending short-term indices. Investors must also break free from the crowd mentality of "it will always go up" and critically assess corporate earnings, cash flow, debt, and interest rate sensitivity.

This recent Black Friday may not just be a panic reaction but part of the market's return to normalcy. The end of an abnormal hyper-rally has brought inflation and interest rates back to the forefront of market considerations. Ultimately, the market cannot outpace fundamentals. What is needed now is neither fear nor frenzy, but a calm return to basics and common sense.

* This article has been translated by AI.

Copyright ⓒ Aju Press All rights reserved.