South Korea is behaving, more by momentum than by design, as if becoming Taiwan is the goal.

Chips already make up 40 percent of the country's exports. Two companies sit behind eight of every ten core memory chips feeding the world's AI accelerators. KOSPI has been the best-performing major index for two straight years running on the back of that concentration.

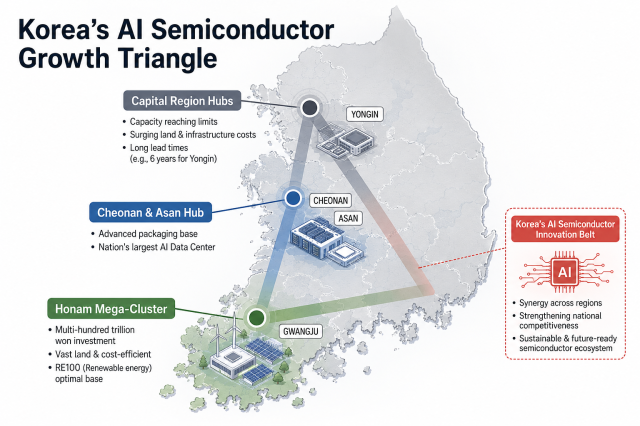

And the government is encouraging Samsung Electronics and SK hynix to expand their footprint beyond the capital region and build up to five new fabs across Honam and Chungcheong.

The argument for deliberately mimicking Taiwan starts with the "silicon shield" logic itself, and it has real force.

Taiwan's indispensability to the global chip supply — TSMC alone stands behind roughly 90 percent of all chips manufactured below the 5-nanometer node, making up about half the Taipei market and singularly responsible for double-digit GDP growth — gives it a form of geopolitical insurance against China that no amount of military spending could buy as efficiently.

A country the world cannot afford to lose access to is a country the world has strong incentives to defend. Korea, bordering a hostile North Korea while watching China lean on Taiwan, has obvious reasons to want that same insurance for itself.

And unlike a reckless bet, this one is backed by demand that looks durable rather than cyclical. Micron's fiscal third-quarter results — revenue of $41.46 billion, up 74 percent in a single quarter, with shares jumping nearly 16 percent on the news — were read across the industry as proof the AI memory cycle won't fizzle out in year two or three the way past cycles did.

CEO Sanjay Mehrotra expects tight DRAM and NAND supply to persist beyond calendar 2027, with no meaningful easing until 2028, because the new capacity coming from Micron's Idaho and New York fabs, SK hynix's M15X line, and Samsung's P5 line won't be fully online until 2027 to 2030.

More tellingly, Micron disclosed 16 long-term Strategic Customer Agreements worth roughly $22 billion in commitments — take-or-pay contracts that lock in demand visibility through 2030 and mark a real structural break from memory's traditionally spot-priced, boom-bust business model.

Samsung and SK hynix are expected to sign similar long-term deals as they finance their own HBM and DRAM expansions. If the demand really is locked in for the rest of the decade, doubling down isn't a gamble — it's just following where the money and the geopolitics both point, which is exactly what Taiwan did with TSMC.

The Honam and Chungcheong expansion is what doubling down looks like in practice, and the country is moving on it with real urgency.

Presidential policy chief Kim Yong-beom has framed the timeline almost as a national emergency: the Yongin-area cluster, originally slated for completion between 2044 and 2048, now needs to be finished by 2034 to 2035, with Korea already needing to scout a "second cluster" for the decade after that, because the capital region has run out of land, power, and water to support more.

SK hynix is reportedly building front- and back-end plants in Gwangju plus a new NAND fab in Cheongju, while Samsung weighs its own packaging and fab investment in Gwangju — hundreds of trillions of won committed to becoming more indispensable, not less.

The problem is that Taiwan's silicon shield rests on something Korea's memory business doesn't have: a monopoly on a capability the rest of the world cannot currently replicate at scale.

Korea's memory dominance does not work that way, and the most recent data makes that plain.

Counterpoint Research's first-quarter figures show Samsung widening its DRAM lead over SK hynix — 38 percent revenue share to SK hynix's 29 percent, Micron at 22 percent — but that's a reversal from a year earlier, when SK hynix led and Samsung trailed for two straight quarters before they drew even and Samsung pulled ahead.

The leaders inside Korea's own duopoly keep trading places quarter to quarter. More pointedly, China's CXMT used the same boom that lifted Samsung and SK hynix to climb from 3 percent to 8 percent share in a single year.

In HBM, SK hynix's commanding 58 percent share is down from 69 percent a year ago, with Samsung and Micron now tied at 21 percent each, and Counterpoint expects Samsung to keep gaining as it starts shipping HBM4 to Nvidia later this year.

In NAND, China's YMTC more than tripled its share in a year, from 8 to 13 percent. Every category Korea leads is a category where the lead is being actively contested in real time — by an American competitor signing the same kind of long-term contracts, and by Chinese entrants using the identical memory shortage to climb the ladder.

Korea isn't holding an irreplicable monopoly; it's winning a capital-intensive arms race that has to be re-won every year, against rivals who are gaining ground precisely because the same favorable cycle that's lifting Korea is lifting them too.

That distinction matters because of what the Honam expansion's own backers admit about it.

The reporting around the southward fab expansion is candid that this is a bet carrying real risk, talent shortages since semiconductor engineers and graduate researchers have historically resisted relocating outside the capital region; power reliability since the renewable energy that makes Honam attractive is weather-dependent in a way 24-hour fabs cannot tolerate; and oversupply timing since every major producer is expanding capacity at once, and if the global cycle turns down before these fabs are fully operational around 2028 to 2029.

Taiwan's concentration in chips — ICT including semiconductors now accounts for 78.5 percent of its total exports — isn't really a choice Taiwan made so much as a structural reality it built around, having never had a comparably large alternative industrial base to protect.

Korea has a more diversified industrial base than Taiwan ever did, and non-chip sectors of its economy are sitting comparatively muted right through the current boom rather than growing alongside it.

Becoming more like Taiwan doesn't cost Korea nothing, because Korea has something to lose that Taiwan didn't have in the first place.

That's also visible in how the windfall itself is being handled. The government is still debating, rather than deciding, how to spend and redistribute the extra tax revenue the chip boom is generating, even as Samsung and SK hynix are projected to clear a combined 640 trillion won or so in operating profit this year.

Though both chipmaking powerhouse, the two countries aren't actually playing the same game.

Taiwan's shield works because TSMC holds a position nobody can contest on any near-term timeline. Korea's memory business is the opposite: a lead that has to be defended every quarter. Korea has an asset Taiwan never had to weigh against that indispensability — a broader industrial base and a genuine choice about where the chip windfall goes.

The question, therefore, is not whether Korea should build more fabs. It almost certainly should.

The more important question is what Korea builds with the wealth those fabs generate.

If semiconductor windfalls finance robotics, AI software, advanced manufacturing, defense technologies, healthcare and the next generation of globally competitive industries, chips become the foundation of a broader economy.

If they merely finance ever more semiconductor capacity, Korea risks becoming wealthier but narrower.

*The author is the managing editor of AJP.

Copyright ⓒ Aju Press All rights reserved.