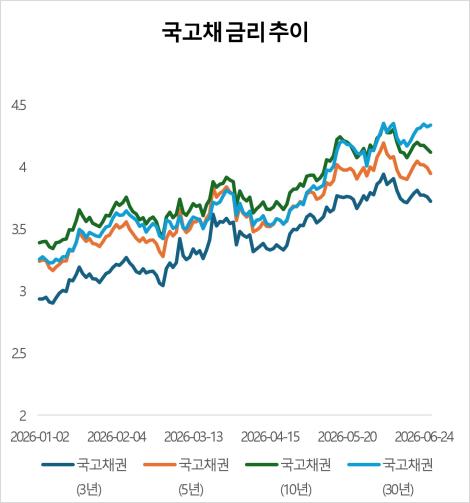

This year, domestic bond yields have experienced significant volatility, resembling a rollercoaster ride. The yields on all maturities of government bonds fluctuated by over 100 basis points (1 basis point = 0.01 percentage points), reaching new highs in June. Increased inflation concerns stemming from geopolitical risks in the Middle East, coupled with tightening signals from the central banks of South Korea and the United States, have contributed to the turbulence in the bond market throughout the first half of the year. While volatility is expected to continue in the second half, forecasts suggest that the peak interest rates will be limited.

According to the Korea Financial Investment Association's Bond Information Center, the yield on three-year government bonds rose from 2.902% to 3.940%, recording a fluctuation of 103.8 basis points. The five-year bonds saw yields range from 3.163% to 4.190%, with a fluctuation of 102.7 basis points, while the ten-year bonds fluctuated between 3.341% and 4.348%, marking a change of 100.7 basis points. The 30-year bonds, classified as ultra-long-term, recorded the largest fluctuation at 112.5 basis points, with yields ranging from 3.224% to 4.349%.

The trend of rising yields accelerated in the latter half of the first half of the year. The three-, five-, and ten-year bonds reached their peak yields on June 8, while the 30-year bonds hit their high on June 11. Market analysts attribute the increased selling pressure on long-term bonds in June to the combined effects of inflation concerns from the Middle East and tightening signals from the central banks.

Several factors have driven the rise in yields, including inflation, fiscal policy, and monetary policy. The ongoing conflict in the Middle East has led to a surge in international oil prices, raising concerns about supply-side inflation pressures. Additionally, the government's expansionary fiscal policy has increased the supply burden of government bonds, further pushing yields higher. The government plans to issue a net total of 109 trillion won in government bonds this year, exceeding 100 trillion won for the second time since the COVID-19 pandemic in 2021. Analysts suggest that expectations of significant government bond issuance early in the year have contributed to upward pressure on long-term yields.

As the first half progressed, signals of tightening from both the Bank of Korea and the U.S. Federal Reserve added to market pressures. The Bank of Korea has strongly hinted at the possibility of raising its benchmark interest rate in the second half, while the Fed has also indicated potential rate hikes within the year. The market has responded by raising long-term yields, reflecting expectations that monetary tightening may last longer than previously anticipated. Long-term bonds tend to exhibit greater volatility than short-term bonds as they incorporate uncertainties related to future interest rates, growth rates, inflation, and fiscal conditions.

At the beginning of the year, there were still some expectations for interest rate cuts. However, the inflation shock from the Middle East, combined with tightening trends from domestic and international central banks, quickly turned the bond market bearish. Particularly, long-term yields have risen significantly as they preemptively reflect concerns about future inflation and fiscal conditions.

Nevertheless, experts believe that while market volatility is likely to persist in the second half, the chances of a repeat of the rapid rise in interest rates seen in the first half are low. Samsung Securities anticipates an improvement in bond supply conditions. The surge in corporate profits from major companies like Samsung Electronics and SK Hynix is expected to significantly increase corporate tax revenues, leading to a substantial decrease in net government bond issuance in 2027.

Experts also note that the anticipated interest rate hikes have already been largely factored into market rates, and the current level of interest rates is relatively high, limiting further upward potential. Kim Ji-man, a researcher at Samsung Securities, stated, "Considering the peaks and duration of the interest rate surges in 2022-2023, we expect significant volatility in the bond market in the second half of this year, but the potential for higher peaks in interest rates is low. The government budget proposal to be announced at the end of August will be a key variable in confirming this."

* This article has been translated by AI.

Copyright ⓒ Aju Press All rights reserved.