Outstanding industrial loans by deposit-taking institutions stood at 2,061.8 trillion won (US$1.33 trillion) at the end of March, up 35.6 trillion won from the previous quarter. The increase widened sharply from an 8.5 trillion won gain in the fourth quarter.

The central bank cited seasonal factors, productive finance, and renewed credit-line borrowing all contributed to the increase, but the widespread rise suggested stronger demand for funds ahead of a potential interest rate hike by the BOK.

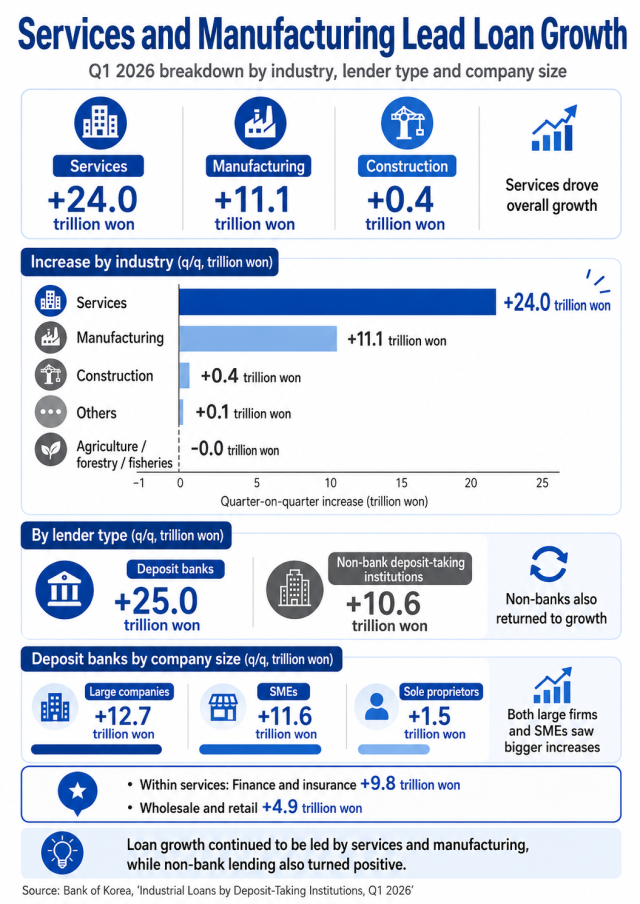

By industry, loans to manufacturers rose 11.1 trillion won, compared with a 1.2 trillion won increase in the previous quarter.

Loans to service companies increased by 24 trillion won, up from a 9.2 trillion won gain, while construction loans rose by 400 billion won, turning positive for the first time in seven quarters.

In particular, working-capital loans showed the sharpest increase as they jumped by 26.2 trillion won in the first quarter, far above the previous quarter's 1.9 trillion won increase. Facility loans also rose by 9.4 trillion won.

"Facility loans in both manufacturing and services also saw faster growth," she added.

Lee also said increased corporate lending by financial institutions under the government's productive finance drive contributed to the rise.

Since late last year, the government has promoted productive finance as a key policy goal, seeking to redirect capital away from real estate and household lending toward corporate investment and regional development.

By lender type, loans by deposit banks increased by 25 trillion won, compared with a 9.6 trillion won gain in the previous quarter. Loans by non-bank deposit-taking institutions rose by 10.6 trillion won, reversing a 1.1 trillion won decline.

Among deposit bank loans, lending to large companies increased by 12.7 trillion won, while loans to small and medium-sized enterprises rose by 11.6 trillion won.

Within the service sector, loans to financial and insurance companies increased by 9.8 trillion won, while loans to wholesale and retail businesses rose by 4.9 trillion won.

Faster loan growth could become a burden if it overlaps with monetary tightening. With companies already increasing debt, higher benchmark and market rates could quickly lift interest expenses. The pressure would be especially direct for working capital, or short-term funds used for wages, interest payments and raw material purchases.

Construction and non-bank lending also remain risk points. Higher rates could add refinancing pressure on weaker developers and prompt non-bank lenders to tighten standards if bad-loan risks rise.

The BOK said the latest loan increase remains manageable. "There have been much larger increases in the past, so in absolute terms, the current level does not appear excessively large," Lee said, asked whether it could raise credit risks.

Copyright ⓒ Aju Press All rights reserved.