The Bank of Korea reported on June 24 that households with multiple properties possess significantly more assets than those without homes, yet their income-based debt repayment capacity is comparatively weaker.

According to the Financial Stability Report released by the Bank of Korea, as of March last year, the net assets of multiple property households stood at 1.07 billion won, seven times that of non-homeowners, who had 145 million won. This disparity is attributed to the greater increase in the value of real estate assets compared to liabilities as the number of properties increases.

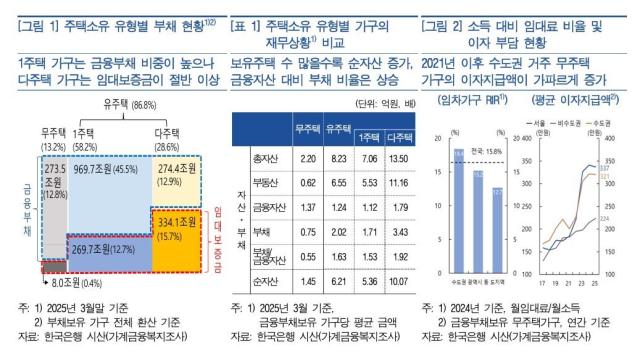

However, the liquidity situation presents a different picture. The debt-to-financial asset ratio for homeowners is 1.63, significantly higher than the 0.55 ratio for non-homeowners. This indicates that while they hold substantial assets, their ability to manage debt with financial assets alone is relatively limited.

The structure of debt also varies. Single-property homeowners tend to have a higher proportion of financial liabilities related to mortgage loans for home purchases, while multiple property owners rely more on rental deposits than on loans from financial institutions. Non-homeowners, on the other hand, have a larger share of loans for securing rental deposits and living expenses.

Debt repayment capacity also differs based on property ownership. Multiple property households have a relatively favorable debt-to-asset ratio (DTA), but their debt service ratio (DSR) is higher than that of non-homeowners and single-property households. This suggests that despite their larger asset base, their ability to repay debt based on income is weaker.

The vulnerability of low-income multiple property households is particularly concerning. As of March this year, the DSR for low-income multiple property households was 72.9%, more than double that of high-income multiple property households at 31.4%, and significantly above the financial authorities' management threshold of 40%.

Delinquency rates also tend to rise with the number of properties owned. As of the end of the first quarter of this year, the average delinquency rate for multiple property owners was slightly higher than that of single-property owners, with borrowers owning three or more properties recording a delinquency rate of 1.35%, a relatively high level.

In contrast, non-homeowners generally face lower overall debt repayment burdens, but the cost of living, particularly in the metropolitan area, is increasing. Recent rises in rental prices in the metropolitan area have led to a higher rental income ratio (RIR) for renting households compared to those in non-metropolitan areas, and the average interest payment amount is also rising rapidly.

The Bank of Korea emphasized the need for policy responses that consider the characteristics of borrowers, as financial soundness varies based on housing ownership. It suggested that support should continue for vulnerable groups among non-homeowners, while maintaining loan accessibility for single-property households within their repayment capacity. Furthermore, it noted that multiple property households are significantly affected by fluctuations in market interest rates and housing prices, highlighting the need for proactive soundness management and orderly housing sales.

* This article has been translated by AI.

Copyright ⓒ Aju Press All rights reserved.