Another painful correction hit the Seoul stock market, which until just a week ago had appeared almost invincible after an extraordinary 18-month rally.

The KOSPI tumbled nearly 8 percent on Thursday, while the KOSDAQ fell almost 7 percent, a brutal hangover for the junior market just a day after its subdued 30th anniversary. The KOSPI closed at 7,648.09, down about 16 percent from its June 22 peak of 9,114.55. Even so, it remains roughly 90 percent higher than at the start of the year and more than double its level of 3,075.05 a year earlier.

Such spectacular gains naturally attracted profit-taking from foreign investors and savvy short sellers.

Those left nursing the biggest losses, however, are often the latecomers gripped by fear of missing out, many of whom entered the rally with borrowed money.

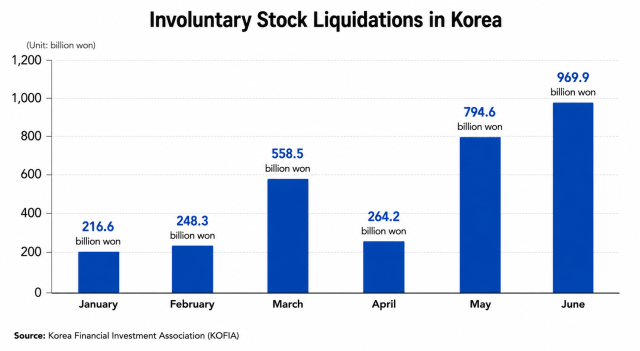

According to the Korea Financial Investment Association (KOFIA), involuntary stock liquidations triggered by margin calls totaled 969.9 billion won ($623 million) in June, the largest monthly amount this year. That brought forced selloffs during the first half to 3.15 trillion won ($2.03 billion).

The monthly figures illustrate how leverage accelerated as the rally gathered pace. Forced liquidations totaled 216.6 billion won in January and 248.3 billion won in February before jumping to 558.5 billion won in March, when Middle East tensions rattled global markets. They eased to 264.2 billion won in April, then surged again to 794.6 billion won in May before reaching June's record.

Yang Jun-sok, an economics professor at the Catholic University of Korea, said the latest wave of forced liquidations should be viewed partly as a "learning process" for investors rather than simply a problem requiring government intervention.

"The problem is moral hazard," Yang said. "If people are protected from losses every time, they will take even greater risks in the future."

The spike in margin calls followed one of the most volatile months in the market's recent history. During June, the KOSPI swung 1,991 points between an intraday low of 7,394.46 and a high of 9,385.59. Just one trading day after closing above 9,000 for the first time, the benchmark plunged 9.99 percent, repeatedly triggering market stabilization measures, including sidecars and circuit breakers.

The Korea Exchange activated 10 sidecars — five on buy orders and five on sell orders — while three circuit breakers were triggered during the month. The VKOSPI volatility index climbed to 97.78 on June 24, its highest level since the 2008 global financial crisis.

The turmoil has also renewed scrutiny of investor safeguards.

A recent review of the country's 10 largest brokerage mobile trading platforms found that nine allow investors to place stock orders exceeding their available cash balance without requiring them to explicitly opt into unpaid settlement trading. Toss Securities, one of the country's newer online brokerages, was the only firm that blocks such orders by default.

Under South Korea's unpaid settlement system, investors can buy stocks by paying only part of the purchase price upfront and settling the remaining balance two business days later. If they fail to make the payment on time, brokerages automatically liquidate the shares to recover the outstanding balance.

Brokerages argue that the system allows experienced investors to trade more efficiently. Critics, however, say the default setting lowers the psychological barrier to leveraged investing by enabling investors to place larger orders without fully appreciating that they are effectively borrowing money.

Yang said brokerages ultimately transfer the risks of leveraged trading to investors, making financial literacy all the more important. He added that investors in more mature markets, such as the United States, generally have a better understanding of investment risks, while South Korea still has room to improve.

"It's like saying too many students received D's, so let's give them more A's, B's and C's instead," he said. "Then no one has an incentive to study."

Government intervention, Yang argued, should be reserved for situations where market losses threaten the broader financial system. Otherwise, allowing investors to bear the consequences of their own decisions, painful as that may be, ultimately creates healthier markets over the long run.

Copyright ⓒ Aju Press All rights reserved.