Recent fluctuations in the KOSPI index have exceeded the volatility levels observed during the COVID-19 pandemic and the global financial crisis. Analysts suggest that this is not merely a correction but a typical high-volatility phase that occurs in the latter part of a bull market.

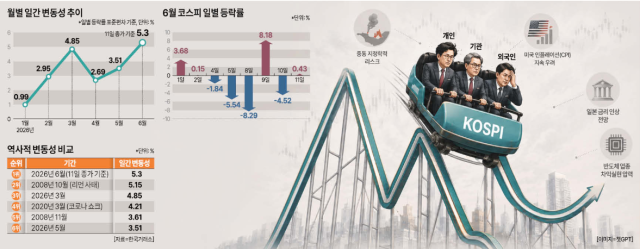

According to the Korea Exchange, the KOSPI dropped 8.29% on June 8, surged 8.18% on June 9, fell 4.52% on June 10, and closed up 0.43% on June 11. This rapid sequence of declines and gains over just four days has heightened investor anxiety.

An analysis of daily KOSPI fluctuations shows that the index's daily volatility for June has averaged 5.30%. This figure, calculated as the standard deviation of daily changes, indicates how much the index has fluctuated. A higher number signifies a more turbulent and uncertain market.

This level of volatility surpasses the 4.21% recorded during the initial shock of the COVID-19 pandemic in March 2020 and is higher than the 5.15% seen in October 2008, when the global financial crisis intensified.

Monthly daily volatility figures for this year are as follows: January 0.99%, February 2.95%, March 4.85%, April 2.69%, May 3.51%, and June 5.30%. The volatility, which remained around 1% at the beginning of the year, has more than quintupled recently.

The recent increase in volatility is attributed to a combination of geopolitical risks in the Middle East, caution ahead of U.S. inflation data releases, expectations of interest rate hikes in Japan, and profit-taking pressures in the semiconductor sector.

Some analysts argue that the current high volatility is not just a simple correction but a typical phenomenon seen in the latter stages of a bull market. Historical trends during the dot-com bubble and the post-pandemic rally of big tech companies show that in the later stages of a bull market, stock prices tend to rise faster while volatility and the frequency of corrections increase. Indeed, KOSPI's daily volatility has surged to 5.30% in June, exceeding the 4.21% recorded during the pandemic shock in March 2020.

Kim Sung-hwan, a researcher at Shinhan Investment Corp, stated, "This bull market can be compared to the roaring 1920s, the dot-com bubble, and the post-pandemic FANG cycle. It is difficult to argue that the market is still in the early to mid-stages of a bull market."

He added, "The latter part of a bull market often brings significant fatigue for investors due to volatility, but until the market peak is confirmed, risk-adjusted returns are often not severely compromised."

Looking ahead, he believes there is still potential for a bullish market for over a year, suggesting that while volatility may increase, adequate compensation for that risk is likely to be provided.

Market observers note that analyzing the current volatility phase using realized volatility based on actual daily fluctuations is beneficial. An industry source explained, "The KOSPI200 volatility index (VKOSPI), known as the fear index, reflects expected volatility based on option prices, while the standard deviation of daily fluctuations reflects actual market movements. The latter may provide a more intuitive understanding of the volatility experienced by investors."

* This article has been translated by AI.

Copyright ⓒ Aju Press All rights reserved.