Latest by

-

What Hyun-mi Kim Left Behind and What Yoon-deok Kim Must Prove The real estate market is difficult to navigate, and homeownership is challenging. In June 2017, the Moon Jae-in administration launched efforts to control housing prices. The government designated all of Seoul as a speculative zone under the 8·2 measures, imposed higher capital gains taxes on multiple homeowners, and announced plans for a reconstruction excess profit recovery system. It also significantly reduced loan limits to curb leverage, with the official rationale being to protect genuine demand and suppress short-term speculative demand. However, just four months later, the government offered incentives for multiple homeowners to register rental properties. This created a conflicting situation where homeowners were pressured to sell but were simultaneously given a legal avenue to avoid doing so. The design of the incentives was contradictory. Subsequent measures became more detailed under the label of “targeted prescriptions.” The 9·13 measures increased comprehensive real estate taxes, tightened loans for multiple homeowners, and imposed regulations on loans for rental businesses. The 12·16 measures prohibited mortgage loans for apartments priced over 150 million won and further lowered the loan-to-value ratio for amounts exceeding 90 million won. The regulatory landscape continued to expand, encompassing taxes, loans, subscriptions, reconstruction, resale, and rental business management. Despite these efforts, the median sale price of apartments in Seoul surged from 606 million won to 920 million won within three years of the Moon administration's inception. The cumulative increase in the actual transaction price index exceeded 45% over the same period. Throughout this time, the Minister of Land, Infrastructure and Transport remained unchanged, with Kim Hyun-mi serving as the longest-serving minister in the department's history. These records did not signify success but rather a chain of failures. The long tenure of Kim Hyun-mi as Minister of Land, Infrastructure and Transport. The reason for revisiting Kim Hyun-mi’s name is not to judge the past but to reflect on the failures of her administration as the new government embarks on a path of stringent real estate regulations. Is Kim Yoon-deok, the current Minister of Land, Infrastructure and Transport, free from the pitfalls that ensnared Kim Hyun-mi? Can he fulfill the tasks at hand until the end? The issue with Kim Hyun-mi’s administration was not a lack of measures; rather, there was an abundance of them. The problem lay in the inability to correct the diagnosis. The Ministry of Land, Infrastructure and Transport's assessment was relatively clear: chronic housing shortages had been largely resolved, housing supply rates had increased, and the number of housing units entering the market in Seoul and the metropolitan area was not below historical averages. They attributed rising housing prices to speculative demand, multiple homeownership, gap investments, liquidity, and expectations of capital gains rather than supply shortages. Based on this assessment, the policy direction became entrenched in regulation. The approach involved tightening taxes, restricting loans, raising barriers for reconstruction, and limiting transactions. While there were supply measures, such as plans for 300,000 units in the metropolitan area, new towns, utilizing idle land in Seoul, and repurposing public facilities, these were more about partial supply in outer public housing areas rather than large-scale urban supply to meet core demand in Seoul. Market signals indicated otherwise. Demand for core areas in Seoul did not diminish, and the scarcity of new apartments in preferred locations increased. As regulations increased, listings became scarce, and demand shifted toward safer assets. Nevertheless, the government did not acknowledge the supply shortage for some time. In July 2020, Kim Hyun-mi stated she did not believe there was a housing supply shortage, explaining that the issue was not the quantity itself but the system for properly supplying it to genuine demand. It was only in November of the same year that she made comments acknowledging a decrease in apartment supply. There had already been several opportunities for a change in leadership. Despite numerous measures, prices continued to rise, listings became scarce, and the debate over supply shortages gained prominence. Opportunities arose when her successor was nominated in 2019 but failed to take office, after the ruling party's landslide victory in the 2020 general elections, and when discussions about a supply shift emerged in the summer of 2020. However, Kim Hyun-mi remained in her position. Her retention was not a decision but a default; in a structure where doing nothing resulted in retention, changing leadership required justifications, candidates, and timing, all of which came with costs. If the diagnosis is incorrect, it must be corrected. However, to correct the diagnosis, one must first acknowledge that it is wrong. Acknowledgment implies dismissal, and dismissal signifies the formal recognition of failure. As long as this equation holds, a change in ministers becomes a means of policy modification rather than a declaration of governmental failure. The Moon administration became a prisoner of this equation. Ultimately, a change occurred only at the end of December 2020, with just over a year left in the administration's term. The new Minister, Byun Chang-heum, introduced a supply plan for 836,000 units just five weeks after taking office. While the numbers were significant, the timing was late. However, LH, the key executing agency for the supply plan, soon became embroiled in pre-speculation allegations regarding the Gwangmyeong and Siheung new towns. The administration lacked both time to recover and political capital. The delayed transition faltered not due to directional issues but due to timing. One cannot attribute Kim Hyun-mi’s failures to Byun Chang-heum. The Byun administration was more a result of the delayed transition. The Kim Hyun-mi administration should have recognized the diagnosis of supply shortages earlier and adjusted the regulatory framework more swiftly. A change in leadership could have been a method for that adjustment. However, the change was perceived as an acknowledgment of failure, and thus it was postponed. In the meantime, the market had moved further away. The new government's approach to real estate regulation and its implications. Five years have passed since then, and the Yoon Suk-yeol administration has begun. The starting point is eerily similar. The guiding principle is “eradication of real estate windfall profits and transition to a productive economic structure.” The 10·15 measures have designated all of Seoul and 12 areas in Gyeonggi Province as regulated zones and land transaction permission areas, and in May of this year, the government resumed higher capital gains taxes. This design aims to tighten the exit routes for multiple homeowners. However, the market is moving in unexpected directions. In a climate of reduced transactions, a few listings are being sold at high prices, a paradox that has become familiar since the introduction of regulations. In the year following the Yoon administration's launch, apartment prices in Seoul recorded double-digit increases according to real estate data, surpassing the initial year’s rise during the Moon administration. The rental market is also showing signs of strain. Regulations on multiple homeowners are reducing rental supply, leading to rental instability, which in turn drives demand for purchases. This chain of events is not unfamiliar, having been witnessed after the implementation of the two rental laws in 2020. The years 2026 and 2027 are expected to see a further decrease in housing supply due to a construction cliff. Pressure in the rental market is likely to continue building for the foreseeable future. Recently, speculation about a cabinet reshuffle has emerged. Following the defeat in the Seoul mayoral election, discussions about a comprehensive revision of real estate policy have coincided with rumors of a change in the Minister of Land, Infrastructure and Transport. Kim Yoon-deok has been in office for less than a year, which is typically considered too early for a change. However, it is difficult to avoid accountability regarding the scarcity of listings, overheating, and rental supply instability in the Seoul real estate market. President Yoon Suk-yeol did not rule out the possibility of a cabinet reshuffle during his press conference marking his first year in office. However, he did not specify which departments would be reviewed in detail. While he did not directly mention Kim Yoon-deok's retention, his comments did not strongly support immediate replacement either. Kim Yoon-deok appears to be aware of this accountability. On the night of June 4, the day after the local elections, he announced on Facebook that he had discussed housing supply plans with the Korea Housing Association, stating, “The government’s commitment to housing supply is resolute and firm.” He emphasized the importance of communicating with supply sites until the goals of the 9·7 housing supply measures are achieved, promising to address any obstacles swiftly. In a context where real estate is cited as a contributing factor to the defeat in the Seoul mayoral election, the Minister of Land, Infrastructure and Transport has reaffirmed his commitment to supply. The minister is inevitably accountable for housing and rental prices. Yoon-deok Kim's other test: balanced development. Moreover, the significance of Kim Yoon-deok as a minister extends beyond managing the real estate market. As the first Minister of Land, Infrastructure and Transport from Jeollabuk-do, he views balanced development and the reorganization of land use as issues of greater importance than mere departmental concerns. The second phase of the relocation of public institutions and the fifth national railway network construction plan are prime examples. Easing the concentration in the metropolitan area and reestablishing regional hubs are central to the new government's land policy. These tasks have already entered the national agenda, transcending personal interests. The importance of balanced development and the relocation of public institutions was publicly addressed in presidential briefings, and the Ministry of Land, Infrastructure and Transport has prioritized the second phase of public institution relocation as a key issue for balanced growth. Kim Yoon-deok has also indicated that he will outline a timeline by September, making it clear that these issues can no longer be postponed as long-term projects. Relocating public institutions is a matter where regional interests clash directly. It carries significant implications if proposed just before a general election, and delaying it too long makes subsequent procedures difficult. With the general election scheduled for April 2028, it is essential to establish a framework within this year. The fifth national railway network construction plan has also been delayed due to complaints from across the country. The moment one line is included or excluded, local political circles and local governments will react simultaneously. Here, the decisive differences between Kim Hyun-mi and Kim Yoon-deok become evident. Kim Hyun-mi was bound to the singular task of real estate. As that task failed, changing ministers became increasingly difficult. Changing the minister would mean acknowledging failure, while not changing would result in the accumulation of failures. In a structure where errors could not be corrected, transitions could not be executed, and failures could not be acknowledged, the more measures there were, the greater the failures became. Kim Yoon-deok, however, is in a different position. This does not mean his task is easier. His responsibilities are twofold. One is to manage the instability of housing and rental prices. If the tightening of regulations leads to increased rental instability and scarcity of listings, Kim Yoon-deok will also face accountability. The other is to transform balanced development and statutory plans into tangible outcomes. This task will inevitably be evaluated as a measure of Kim Yoon-deok’s success. Ultimately, the case of Kim Hyun-mi illustrates one key point: a minister's evaluation hinges not on how long they endure but on whether they fulfill their assigned responsibilities in a timely manner. Managing real estate instability while closing the timeline for balanced development is the challenge that Kim Yoon-deok must prove he can meet.* This article has been translated by AI. 2026-06-15 14:51:00

What Hyun-mi Kim Left Behind and What Yoon-deok Kim Must Prove The real estate market is difficult to navigate, and homeownership is challenging. In June 2017, the Moon Jae-in administration launched efforts to control housing prices. The government designated all of Seoul as a speculative zone under the 8·2 measures, imposed higher capital gains taxes on multiple homeowners, and announced plans for a reconstruction excess profit recovery system. It also significantly reduced loan limits to curb leverage, with the official rationale being to protect genuine demand and suppress short-term speculative demand. However, just four months later, the government offered incentives for multiple homeowners to register rental properties. This created a conflicting situation where homeowners were pressured to sell but were simultaneously given a legal avenue to avoid doing so. The design of the incentives was contradictory. Subsequent measures became more detailed under the label of “targeted prescriptions.” The 9·13 measures increased comprehensive real estate taxes, tightened loans for multiple homeowners, and imposed regulations on loans for rental businesses. The 12·16 measures prohibited mortgage loans for apartments priced over 150 million won and further lowered the loan-to-value ratio for amounts exceeding 90 million won. The regulatory landscape continued to expand, encompassing taxes, loans, subscriptions, reconstruction, resale, and rental business management. Despite these efforts, the median sale price of apartments in Seoul surged from 606 million won to 920 million won within three years of the Moon administration's inception. The cumulative increase in the actual transaction price index exceeded 45% over the same period. Throughout this time, the Minister of Land, Infrastructure and Transport remained unchanged, with Kim Hyun-mi serving as the longest-serving minister in the department's history. These records did not signify success but rather a chain of failures. The long tenure of Kim Hyun-mi as Minister of Land, Infrastructure and Transport. The reason for revisiting Kim Hyun-mi’s name is not to judge the past but to reflect on the failures of her administration as the new government embarks on a path of stringent real estate regulations. Is Kim Yoon-deok, the current Minister of Land, Infrastructure and Transport, free from the pitfalls that ensnared Kim Hyun-mi? Can he fulfill the tasks at hand until the end? The issue with Kim Hyun-mi’s administration was not a lack of measures; rather, there was an abundance of them. The problem lay in the inability to correct the diagnosis. The Ministry of Land, Infrastructure and Transport's assessment was relatively clear: chronic housing shortages had been largely resolved, housing supply rates had increased, and the number of housing units entering the market in Seoul and the metropolitan area was not below historical averages. They attributed rising housing prices to speculative demand, multiple homeownership, gap investments, liquidity, and expectations of capital gains rather than supply shortages. Based on this assessment, the policy direction became entrenched in regulation. The approach involved tightening taxes, restricting loans, raising barriers for reconstruction, and limiting transactions. While there were supply measures, such as plans for 300,000 units in the metropolitan area, new towns, utilizing idle land in Seoul, and repurposing public facilities, these were more about partial supply in outer public housing areas rather than large-scale urban supply to meet core demand in Seoul. Market signals indicated otherwise. Demand for core areas in Seoul did not diminish, and the scarcity of new apartments in preferred locations increased. As regulations increased, listings became scarce, and demand shifted toward safer assets. Nevertheless, the government did not acknowledge the supply shortage for some time. In July 2020, Kim Hyun-mi stated she did not believe there was a housing supply shortage, explaining that the issue was not the quantity itself but the system for properly supplying it to genuine demand. It was only in November of the same year that she made comments acknowledging a decrease in apartment supply. There had already been several opportunities for a change in leadership. Despite numerous measures, prices continued to rise, listings became scarce, and the debate over supply shortages gained prominence. Opportunities arose when her successor was nominated in 2019 but failed to take office, after the ruling party's landslide victory in the 2020 general elections, and when discussions about a supply shift emerged in the summer of 2020. However, Kim Hyun-mi remained in her position. Her retention was not a decision but a default; in a structure where doing nothing resulted in retention, changing leadership required justifications, candidates, and timing, all of which came with costs. If the diagnosis is incorrect, it must be corrected. However, to correct the diagnosis, one must first acknowledge that it is wrong. Acknowledgment implies dismissal, and dismissal signifies the formal recognition of failure. As long as this equation holds, a change in ministers becomes a means of policy modification rather than a declaration of governmental failure. The Moon administration became a prisoner of this equation. Ultimately, a change occurred only at the end of December 2020, with just over a year left in the administration's term. The new Minister, Byun Chang-heum, introduced a supply plan for 836,000 units just five weeks after taking office. While the numbers were significant, the timing was late. However, LH, the key executing agency for the supply plan, soon became embroiled in pre-speculation allegations regarding the Gwangmyeong and Siheung new towns. The administration lacked both time to recover and political capital. The delayed transition faltered not due to directional issues but due to timing. One cannot attribute Kim Hyun-mi’s failures to Byun Chang-heum. The Byun administration was more a result of the delayed transition. The Kim Hyun-mi administration should have recognized the diagnosis of supply shortages earlier and adjusted the regulatory framework more swiftly. A change in leadership could have been a method for that adjustment. However, the change was perceived as an acknowledgment of failure, and thus it was postponed. In the meantime, the market had moved further away. The new government's approach to real estate regulation and its implications. Five years have passed since then, and the Yoon Suk-yeol administration has begun. The starting point is eerily similar. The guiding principle is “eradication of real estate windfall profits and transition to a productive economic structure.” The 10·15 measures have designated all of Seoul and 12 areas in Gyeonggi Province as regulated zones and land transaction permission areas, and in May of this year, the government resumed higher capital gains taxes. This design aims to tighten the exit routes for multiple homeowners. However, the market is moving in unexpected directions. In a climate of reduced transactions, a few listings are being sold at high prices, a paradox that has become familiar since the introduction of regulations. In the year following the Yoon administration's launch, apartment prices in Seoul recorded double-digit increases according to real estate data, surpassing the initial year’s rise during the Moon administration. The rental market is also showing signs of strain. Regulations on multiple homeowners are reducing rental supply, leading to rental instability, which in turn drives demand for purchases. This chain of events is not unfamiliar, having been witnessed after the implementation of the two rental laws in 2020. The years 2026 and 2027 are expected to see a further decrease in housing supply due to a construction cliff. Pressure in the rental market is likely to continue building for the foreseeable future. Recently, speculation about a cabinet reshuffle has emerged. Following the defeat in the Seoul mayoral election, discussions about a comprehensive revision of real estate policy have coincided with rumors of a change in the Minister of Land, Infrastructure and Transport. Kim Yoon-deok has been in office for less than a year, which is typically considered too early for a change. However, it is difficult to avoid accountability regarding the scarcity of listings, overheating, and rental supply instability in the Seoul real estate market. President Yoon Suk-yeol did not rule out the possibility of a cabinet reshuffle during his press conference marking his first year in office. However, he did not specify which departments would be reviewed in detail. While he did not directly mention Kim Yoon-deok's retention, his comments did not strongly support immediate replacement either. Kim Yoon-deok appears to be aware of this accountability. On the night of June 4, the day after the local elections, he announced on Facebook that he had discussed housing supply plans with the Korea Housing Association, stating, “The government’s commitment to housing supply is resolute and firm.” He emphasized the importance of communicating with supply sites until the goals of the 9·7 housing supply measures are achieved, promising to address any obstacles swiftly. In a context where real estate is cited as a contributing factor to the defeat in the Seoul mayoral election, the Minister of Land, Infrastructure and Transport has reaffirmed his commitment to supply. The minister is inevitably accountable for housing and rental prices. Yoon-deok Kim's other test: balanced development. Moreover, the significance of Kim Yoon-deok as a minister extends beyond managing the real estate market. As the first Minister of Land, Infrastructure and Transport from Jeollabuk-do, he views balanced development and the reorganization of land use as issues of greater importance than mere departmental concerns. The second phase of the relocation of public institutions and the fifth national railway network construction plan are prime examples. Easing the concentration in the metropolitan area and reestablishing regional hubs are central to the new government's land policy. These tasks have already entered the national agenda, transcending personal interests. The importance of balanced development and the relocation of public institutions was publicly addressed in presidential briefings, and the Ministry of Land, Infrastructure and Transport has prioritized the second phase of public institution relocation as a key issue for balanced growth. Kim Yoon-deok has also indicated that he will outline a timeline by September, making it clear that these issues can no longer be postponed as long-term projects. Relocating public institutions is a matter where regional interests clash directly. It carries significant implications if proposed just before a general election, and delaying it too long makes subsequent procedures difficult. With the general election scheduled for April 2028, it is essential to establish a framework within this year. The fifth national railway network construction plan has also been delayed due to complaints from across the country. The moment one line is included or excluded, local political circles and local governments will react simultaneously. Here, the decisive differences between Kim Hyun-mi and Kim Yoon-deok become evident. Kim Hyun-mi was bound to the singular task of real estate. As that task failed, changing ministers became increasingly difficult. Changing the minister would mean acknowledging failure, while not changing would result in the accumulation of failures. In a structure where errors could not be corrected, transitions could not be executed, and failures could not be acknowledged, the more measures there were, the greater the failures became. Kim Yoon-deok, however, is in a different position. This does not mean his task is easier. His responsibilities are twofold. One is to manage the instability of housing and rental prices. If the tightening of regulations leads to increased rental instability and scarcity of listings, Kim Yoon-deok will also face accountability. The other is to transform balanced development and statutory plans into tangible outcomes. This task will inevitably be evaluated as a measure of Kim Yoon-deok’s success. Ultimately, the case of Kim Hyun-mi illustrates one key point: a minister's evaluation hinges not on how long they endure but on whether they fulfill their assigned responsibilities in a timely manner. Managing real estate instability while closing the timeline for balanced development is the challenge that Kim Yoon-deok must prove he can meet.* This article has been translated by AI. 2026-06-15 14:51:00 -

Retirement Pension Fees Can Significantly Impact Your Returns When selecting retirement pension products, subscribers typically focus on returns, but another crucial factor is fees. Even with similar returns, the fees can differ significantly, sometimes by dozens of times, making it essential to consider costs as well. An analysis of the Financial Supervisory Service's disclosure data on retirement pension providers revealed substantial disparities in fee burdens, even among similar types of plans. The fee burden refers to the costs incurred by subscribers for management and asset handling, which are deducted from assets annually and can significantly affect compounding over the long term. For instance, as of the fourth quarter of last year, Shin Young Securities reported a total fee burden rate of 0.126% for its defined benefit (DB) plans, while Mirae Asset Securities had a rate of 0.399% and iM Securities reported 0.386%. This indicates that even within the same sector, the fees borne by subscribers can vary by more than three times. The fee burden rate is calculated by adding management and asset handling fees, which are often lower for non-face-to-face products or promotional offerings. This month, Kiwoom Securities, a new entrant in the retirement pension market, announced a zero percent fee for the first year. However, a higher fee does not always correlate with higher returns. For example, based on a 10-year non-guaranteed principal and interest return, KB Insurance achieved a return of 4.56%, while DB Insurance reported 4.62%, with a performance difference of just 0.1 percentage points. The differences become more pronounced across different sectors. For instance, Woori Bank's Individual Retirement Pension (IRP) had a three-year return of 13.24%, while Fubon Hyundai Life Insurance reported 12.32%. However, the fees were drastically different, with Woori Bank at 0.007% and Fubon Hyundai Life at 0.347%. These figures reflect the cost levels at the time of disclosure, and individual returns may vary based on the specific products and asset allocations chosen by subscribers. Nevertheless, relying solely on return rankings when selecting a provider can obscure a complete assessment of actual investment performance. A financial industry official noted, "Given that retirement pensions are long-term assets managed over 20 to 30 years, even small differences in fees can accumulate over time." This means that even a 0.1 to 0.2 percentage point increase in annual fees can significantly impact the final payout when compounded over the long term.* This article has been translated by AI. 2026-06-15 14:51:00

Retirement Pension Fees Can Significantly Impact Your Returns When selecting retirement pension products, subscribers typically focus on returns, but another crucial factor is fees. Even with similar returns, the fees can differ significantly, sometimes by dozens of times, making it essential to consider costs as well. An analysis of the Financial Supervisory Service's disclosure data on retirement pension providers revealed substantial disparities in fee burdens, even among similar types of plans. The fee burden refers to the costs incurred by subscribers for management and asset handling, which are deducted from assets annually and can significantly affect compounding over the long term. For instance, as of the fourth quarter of last year, Shin Young Securities reported a total fee burden rate of 0.126% for its defined benefit (DB) plans, while Mirae Asset Securities had a rate of 0.399% and iM Securities reported 0.386%. This indicates that even within the same sector, the fees borne by subscribers can vary by more than three times. The fee burden rate is calculated by adding management and asset handling fees, which are often lower for non-face-to-face products or promotional offerings. This month, Kiwoom Securities, a new entrant in the retirement pension market, announced a zero percent fee for the first year. However, a higher fee does not always correlate with higher returns. For example, based on a 10-year non-guaranteed principal and interest return, KB Insurance achieved a return of 4.56%, while DB Insurance reported 4.62%, with a performance difference of just 0.1 percentage points. The differences become more pronounced across different sectors. For instance, Woori Bank's Individual Retirement Pension (IRP) had a three-year return of 13.24%, while Fubon Hyundai Life Insurance reported 12.32%. However, the fees were drastically different, with Woori Bank at 0.007% and Fubon Hyundai Life at 0.347%. These figures reflect the cost levels at the time of disclosure, and individual returns may vary based on the specific products and asset allocations chosen by subscribers. Nevertheless, relying solely on return rankings when selecting a provider can obscure a complete assessment of actual investment performance. A financial industry official noted, "Given that retirement pensions are long-term assets managed over 20 to 30 years, even small differences in fees can accumulate over time." This means that even a 0.1 to 0.2 percentage point increase in annual fees can significantly impact the final payout when compounded over the long term.* This article has been translated by AI. 2026-06-15 14:51:00 -

Mirae Asset faces investor fury and probe after SpaceX IPO allocation failure SEOUL, June 15 (AJP) — South Korea's second-largest brokerage house Mirae Asset Securities is under fire after failing to secure any shares in the blockbuster initial public offering of SpaceX, leaving Korean investors empty-handed in one of the world's most coveted listings. "Pathetic," one investor wrote on Mirae Asset's online forum. "Run before you get burned," another wrote Monday, referring to Mirae Asset Securities' own share price, which fell about 2 percent despite a 5.5 percent rally in the benchmark KOSPI. The backlash has quickly widened into a regulatory issue. The Financial Supervisory Service has launched an inspection into why Mirae Asset failed to receive shares that had been expected for Korean investors and whether the brokerage properly warned clients that final allocations could be reduced or canceled. According to investment banking sources, SpaceX had initially been expected to allocate 2,314,815 Class A common shares to Mirae Asset out of 555,555,555 shares sold in the offering. But Goldman Sachs, the lead underwriter, reportedly excluded Mirae Asset and some other syndicate members from the final distribution. The failure stunned Korean investors, who have become among the world's most aggressive retail buyers of U.S. stocks and had viewed SpaceX as a rare chance to enter a global AI, defense and space infrastructure play at the IPO stage. As of June 11, South Koreans owned $190.2 billion in U.S. equities, of which Tesla shares make up $24.1 billion worth. Mirae Asset has refunded subscription deposits in full, but investors may still have suffered losses from currency conversion, overseas remittance and refund procedures. Some deposits were converted into dollars when the won-dollar rate was around 1,530, while refunds were returned when the rate had moved closer to 1,510, raising the possibility of foreign-exchange losses. The FSS is also examining whether Mirae Asset sufficiently disclosed allocation risks, whether there was exaggerated marketing, and whether the brokerage had understood in advance that it might fail to receive any shares. A key issue is regulatory approval. Industry officials said Mirae Asset's failure to obtain clearance from Korean financial authorities may have made global underwriters reluctant to allocate shares to the brokerage. Korea requires securities registration documents to be submitted at least 15 business days before a public offering to general investors, but SpaceX followed U.S. IPO rules and filed roughly a week before listing. Mirae Asset later shifted the subscription from a public offering for general investors to a private placement for professional investors, but industry officials said the change may not have been fully coordinated with global advisers. In contrast, Mizuho Securities, which secured approval from Japanese regulators, reportedly received about $2.2 billion worth of SpaceX shares, or roughly 3 percent of the offering. The controversy has also spread to exchange-traded funds. Some asset managers had promoted plans to include SpaceX IPO shares secured through Mirae Asset in their ETFs. When the allocation failed, at least one fund reportedly bought SpaceX shares in the market on listing day, potentially at prices well above the $135 IPO price. Regulators are expected to examine whether ETF investors were disadvantaged as a result. The FSS is also expected to review possible conflict-of-interest issues after reports that Mirae Asset Group affiliates participated separately with proprietary capital and received SpaceX shares through a U.S.-based institutional channel. Those shares were separate from the failed client subscription, but the situation has raised questions over whether group interests and client interests were properly managed. Mirae Asset apologized to clients for failing to meet expectations. "We apologize for the inconvenience and for failing to meet the expectations of customers who waited a long time for the subscription results," the company said in a notice. The case is drawing heightened attention because it comes before a possible wave of U.S. mega-listings involving artificial intelligence companies such as Anthropic and OpenAI. Financial authorities see the SpaceX failure as a test case for how Korean brokerages should handle overseas IPO access for local investors. An FSS official said the regulator needs to thoroughly examine what happened because investor protection will become increasingly important as more Korean capital seeks access to global IPOs. 2026-06-15 14:49:58

Mirae Asset faces investor fury and probe after SpaceX IPO allocation failure SEOUL, June 15 (AJP) — South Korea's second-largest brokerage house Mirae Asset Securities is under fire after failing to secure any shares in the blockbuster initial public offering of SpaceX, leaving Korean investors empty-handed in one of the world's most coveted listings. "Pathetic," one investor wrote on Mirae Asset's online forum. "Run before you get burned," another wrote Monday, referring to Mirae Asset Securities' own share price, which fell about 2 percent despite a 5.5 percent rally in the benchmark KOSPI. The backlash has quickly widened into a regulatory issue. The Financial Supervisory Service has launched an inspection into why Mirae Asset failed to receive shares that had been expected for Korean investors and whether the brokerage properly warned clients that final allocations could be reduced or canceled. According to investment banking sources, SpaceX had initially been expected to allocate 2,314,815 Class A common shares to Mirae Asset out of 555,555,555 shares sold in the offering. But Goldman Sachs, the lead underwriter, reportedly excluded Mirae Asset and some other syndicate members from the final distribution. The failure stunned Korean investors, who have become among the world's most aggressive retail buyers of U.S. stocks and had viewed SpaceX as a rare chance to enter a global AI, defense and space infrastructure play at the IPO stage. As of June 11, South Koreans owned $190.2 billion in U.S. equities, of which Tesla shares make up $24.1 billion worth. Mirae Asset has refunded subscription deposits in full, but investors may still have suffered losses from currency conversion, overseas remittance and refund procedures. Some deposits were converted into dollars when the won-dollar rate was around 1,530, while refunds were returned when the rate had moved closer to 1,510, raising the possibility of foreign-exchange losses. The FSS is also examining whether Mirae Asset sufficiently disclosed allocation risks, whether there was exaggerated marketing, and whether the brokerage had understood in advance that it might fail to receive any shares. A key issue is regulatory approval. Industry officials said Mirae Asset's failure to obtain clearance from Korean financial authorities may have made global underwriters reluctant to allocate shares to the brokerage. Korea requires securities registration documents to be submitted at least 15 business days before a public offering to general investors, but SpaceX followed U.S. IPO rules and filed roughly a week before listing. Mirae Asset later shifted the subscription from a public offering for general investors to a private placement for professional investors, but industry officials said the change may not have been fully coordinated with global advisers. In contrast, Mizuho Securities, which secured approval from Japanese regulators, reportedly received about $2.2 billion worth of SpaceX shares, or roughly 3 percent of the offering. The controversy has also spread to exchange-traded funds. Some asset managers had promoted plans to include SpaceX IPO shares secured through Mirae Asset in their ETFs. When the allocation failed, at least one fund reportedly bought SpaceX shares in the market on listing day, potentially at prices well above the $135 IPO price. Regulators are expected to examine whether ETF investors were disadvantaged as a result. The FSS is also expected to review possible conflict-of-interest issues after reports that Mirae Asset Group affiliates participated separately with proprietary capital and received SpaceX shares through a U.S.-based institutional channel. Those shares were separate from the failed client subscription, but the situation has raised questions over whether group interests and client interests were properly managed. Mirae Asset apologized to clients for failing to meet expectations. "We apologize for the inconvenience and for failing to meet the expectations of customers who waited a long time for the subscription results," the company said in a notice. The case is drawing heightened attention because it comes before a possible wave of U.S. mega-listings involving artificial intelligence companies such as Anthropic and OpenAI. Financial authorities see the SpaceX failure as a test case for how Korean brokerages should handle overseas IPO access for local investors. An FSS official said the regulator needs to thoroughly examine what happened because investor protection will become increasingly important as more Korean capital seeks access to global IPOs. 2026-06-15 14:49:58 -

NongHyup to Forgive 887.6 Billion Won in Delinquent Loans, Support 90,000 Vulnerable Individuals NongHyup will forgive 887.6 billion won in delinquent loans to support vulnerable populations. Additionally, the organization plans to provide over 15 trillion won in inclusive finance over the next five years to expand financial support for low-income individuals and farmers.On June 15, the NongHyup Central Association announced that it will forgive and write off a total of 887.6 billion won in long-term delinquent loans this year, aligning with the government's inclusive finance policy. This initiative aims to assist approximately 90,000 vulnerable individuals in their recovery.NongHyup plans to write off 687 billion won in long-term delinquent loans this year, relieving 64,000 individuals from collection burdens and supporting credit recovery. The breakdown by subsidiary includes 287 billion won from NongHyup Bank, 150 billion won from agricultural and livestock cooperatives, and 250 billion won from NongHyup Asset Management. As of last month, 178.5 billion won in long-term delinquent loans had already been written off, with an additional 508.5 billion won planned for the end of the year.Furthermore, NongHyup will reduce the principal and interest on loans that have been delinquent for over three years, targeting socially vulnerable groups such as the elderly and basic livelihood recipients, amounting to 200.6 billion won. The principal will be reduced by up to 90%, and all unpaid interest will be waived to encourage diligent repayment and improve credit ratings for delinquent borrowers.Currently, NongHyup has established a plan to provide 15.3 trillion won in inclusive finance over the next five years. This support will focus on loans for small businesses and self-employed individuals totaling 8.5 trillion won, as well as 6.8 trillion won for low-income and vulnerable groups.NongHyup Central Association Chairman Kang Ho-dong stated, "The write-off and forgiveness of long-term delinquent loans is part of our commitment to inclusive finance, bringing hope for recovery to those who have faced economic hardship for a long time. We will continue to expand inclusive finance across NongHyup to strengthen our public interest role and fulfill our social responsibilities."* This article has been translated by AI. 2026-06-15 14:48:00

NongHyup to Forgive 887.6 Billion Won in Delinquent Loans, Support 90,000 Vulnerable Individuals NongHyup will forgive 887.6 billion won in delinquent loans to support vulnerable populations. Additionally, the organization plans to provide over 15 trillion won in inclusive finance over the next five years to expand financial support for low-income individuals and farmers.On June 15, the NongHyup Central Association announced that it will forgive and write off a total of 887.6 billion won in long-term delinquent loans this year, aligning with the government's inclusive finance policy. This initiative aims to assist approximately 90,000 vulnerable individuals in their recovery.NongHyup plans to write off 687 billion won in long-term delinquent loans this year, relieving 64,000 individuals from collection burdens and supporting credit recovery. The breakdown by subsidiary includes 287 billion won from NongHyup Bank, 150 billion won from agricultural and livestock cooperatives, and 250 billion won from NongHyup Asset Management. As of last month, 178.5 billion won in long-term delinquent loans had already been written off, with an additional 508.5 billion won planned for the end of the year.Furthermore, NongHyup will reduce the principal and interest on loans that have been delinquent for over three years, targeting socially vulnerable groups such as the elderly and basic livelihood recipients, amounting to 200.6 billion won. The principal will be reduced by up to 90%, and all unpaid interest will be waived to encourage diligent repayment and improve credit ratings for delinquent borrowers.Currently, NongHyup has established a plan to provide 15.3 trillion won in inclusive finance over the next five years. This support will focus on loans for small businesses and self-employed individuals totaling 8.5 trillion won, as well as 6.8 trillion won for low-income and vulnerable groups.NongHyup Central Association Chairman Kang Ho-dong stated, "The write-off and forgiveness of long-term delinquent loans is part of our commitment to inclusive finance, bringing hope for recovery to those who have faced economic hardship for a long time. We will continue to expand inclusive finance across NongHyup to strengthen our public interest role and fulfill our social responsibilities."* This article has been translated by AI. 2026-06-15 14:48:00 -

Foreign Investors Increase Short Selling and Stock Borrowing in KOSPI Market Foreign investors have sold more than 22 trillion won in net terms in the KOSPI market this month, while the scale of short selling and stock borrowing has also rapidly increased. Analysts suggest that the simultaneous expansion of cash sales and short selling is amplifying the influence of foreign investors in the domestic stock market. According to the Korea Exchange on June 15, foreign investors net sold over 22 trillion won in the KOSPI market from the beginning of this month until June 12. Although they returned to net buying on June 12, they had previously engaged in net selling for 23 consecutive trading days, increasing the supply-demand burden on the domestic market. During this period, short selling transactions also surged significantly. The average daily short selling amount by foreign investors was approximately 2.6 trillion won, marking a 43% increase from last month's 1.8 trillion won. Compared to 1.1 trillion won two months ago in April, this represents an increase of over 130%. The proportion of foreign investors in total short selling transactions has also grown. This month, foreign investors accounted for 75.7% of short selling, up 7.5 percentage points from last month's 68.2%. Compared to 66.0% two months ago, the increase is even more pronounced. Given that foreign short selling transactions were around 8.6 trillion won at the beginning of the year, the recent upward trend is notable. In the stock borrowing market, the presence of foreign investors is also increasing. Stock borrowing involves transactions where investors borrow and lend shares, often serving as a precursor to short selling. The borrowing balance for foreign investors has risen from approximately 45.9 trillion won in January to about 76.5 trillion won this month, a 66% increase in just five months. While the increase in balance value is partly due to rising stock prices, the proportion of foreign investors in the total borrowing balance has also grown from 47.4% to 53.1% during the same period, indicating expanded participation in the stock borrowing market. Although it cannot be definitively concluded that the increase in borrowing balance directly leads to expanded short selling, there are observations that the surge in short selling transactions is linked to heightened demand for downward bets by foreign investors. Short selling has been particularly concentrated among large-cap stocks in sectors such as semiconductors, IT, and automobiles. The stock with the highest short selling this month was SK Hynix, exceeding 5 trillion won. Following that, Samsung Electronics saw about 3.5 trillion won in short selling, while Hyundai Motor, Samsung Electro-Mechanics, SK Square, and LG Electronics also experienced over 1 trillion won in short selling. 2026-06-15 14:48:00

Foreign Investors Increase Short Selling and Stock Borrowing in KOSPI Market Foreign investors have sold more than 22 trillion won in net terms in the KOSPI market this month, while the scale of short selling and stock borrowing has also rapidly increased. Analysts suggest that the simultaneous expansion of cash sales and short selling is amplifying the influence of foreign investors in the domestic stock market. According to the Korea Exchange on June 15, foreign investors net sold over 22 trillion won in the KOSPI market from the beginning of this month until June 12. Although they returned to net buying on June 12, they had previously engaged in net selling for 23 consecutive trading days, increasing the supply-demand burden on the domestic market. During this period, short selling transactions also surged significantly. The average daily short selling amount by foreign investors was approximately 2.6 trillion won, marking a 43% increase from last month's 1.8 trillion won. Compared to 1.1 trillion won two months ago in April, this represents an increase of over 130%. The proportion of foreign investors in total short selling transactions has also grown. This month, foreign investors accounted for 75.7% of short selling, up 7.5 percentage points from last month's 68.2%. Compared to 66.0% two months ago, the increase is even more pronounced. Given that foreign short selling transactions were around 8.6 trillion won at the beginning of the year, the recent upward trend is notable. In the stock borrowing market, the presence of foreign investors is also increasing. Stock borrowing involves transactions where investors borrow and lend shares, often serving as a precursor to short selling. The borrowing balance for foreign investors has risen from approximately 45.9 trillion won in January to about 76.5 trillion won this month, a 66% increase in just five months. While the increase in balance value is partly due to rising stock prices, the proportion of foreign investors in the total borrowing balance has also grown from 47.4% to 53.1% during the same period, indicating expanded participation in the stock borrowing market. Although it cannot be definitively concluded that the increase in borrowing balance directly leads to expanded short selling, there are observations that the surge in short selling transactions is linked to heightened demand for downward bets by foreign investors. Short selling has been particularly concentrated among large-cap stocks in sectors such as semiconductors, IT, and automobiles. The stock with the highest short selling this month was SK Hynix, exceeding 5 trillion won. Following that, Samsung Electronics saw about 3.5 trillion won in short selling, while Hyundai Motor, Samsung Electro-Mechanics, SK Square, and LG Electronics also experienced over 1 trillion won in short selling. 2026-06-15 14:48:00 -

Defense Ministry Calls Report on Teachers Visiting Chinese War Memorial a Serious Error The Defense Ministry stated it is investigating reports that the War Memorial Foundation considered including a visit to the Chinese "Anti-American Aid Memorial" in a training program for teachers. During a regular briefing on the 15th, Defense Ministry spokesperson Jeong Bit-na said that an audit is currently underway regarding the program and added, "Regardless of the reasons, the decision to review related schedules is considered a serious error by the Defense Ministry." She continued, "We will thoroughly clarify the facts through the audit and take strict action. There should be no actions that undermine the sacrifices and dedication of those who fought for the country." The War Memorial Foundation, which operates the Yongsan War Memorial under the Defense Ministry, reportedly included the Anti-American Aid Memorial in Dandong in its overseas training schedule for elementary, middle, and high school teachers this year but later removed it. Recently, the War Memorial Foundation faced criticism for promoting an educational program for the month of national defense and veterans, which presented the Korean War as the "Anti-American Aid War" alongside South Korea's perspective on the conflict. The term "Anti-American Aid" is a propaganda phrase used by China to justify its intervention in the Korean War, claiming to assist North Korea against American aggression. Spokesperson Jeong stated that an audit is currently underway regarding the promotional materials, as directed by the Defense Minister, and emphasized that if any violations are confirmed, strict actions will be taken in accordance with relevant regulations and procedures.* This article has been translated by AI. 2026-06-15 14:39:00

Defense Ministry Calls Report on Teachers Visiting Chinese War Memorial a Serious Error The Defense Ministry stated it is investigating reports that the War Memorial Foundation considered including a visit to the Chinese "Anti-American Aid Memorial" in a training program for teachers. During a regular briefing on the 15th, Defense Ministry spokesperson Jeong Bit-na said that an audit is currently underway regarding the program and added, "Regardless of the reasons, the decision to review related schedules is considered a serious error by the Defense Ministry." She continued, "We will thoroughly clarify the facts through the audit and take strict action. There should be no actions that undermine the sacrifices and dedication of those who fought for the country." The War Memorial Foundation, which operates the Yongsan War Memorial under the Defense Ministry, reportedly included the Anti-American Aid Memorial in Dandong in its overseas training schedule for elementary, middle, and high school teachers this year but later removed it. Recently, the War Memorial Foundation faced criticism for promoting an educational program for the month of national defense and veterans, which presented the Korean War as the "Anti-American Aid War" alongside South Korea's perspective on the conflict. The term "Anti-American Aid" is a propaganda phrase used by China to justify its intervention in the Korean War, claiming to assist North Korea against American aggression. Spokesperson Jeong stated that an audit is currently underway regarding the promotional materials, as directed by the Defense Minister, and emphasized that if any violations are confirmed, strict actions will be taken in accordance with relevant regulations and procedures.* This article has been translated by AI. 2026-06-15 14:39:00 -

Sweden Dominates Tunisia 5-1 to Lead Group F at 2026 FIFA World Cup Sweden displayed an impressive offensive performance, defeating Tunisia 5-1 in their opening match of Group E at the 2026 FIFA World Cup on June 15 at the Estadio Monterrey in Mexico. Returning to the World Cup stage for the first time since 2018, Sweden increased its chances of advancing from the group stage. They currently lead Group F, surpassing Japan and the Netherlands, who played to a 2-2 draw in their earlier match. Group F has been labeled the 'Group of Death' due to its competitive nature. This year's tournament features an expanded format with 48 teams, allowing the top two teams from each group, along with the eight best third-placed teams, to advance to the knockout stage. Sweden struck first, scoring in the 7th minute when Yasin Ayari capitalized on a cleared ball and unleashed a powerful right-footed shot from distance. Ayari, who has a Tunisian father and a Moroccan mother, scored his debut World Cup goal against his father's nation and showed restraint during his celebration. In the 30th minute, Sweden added a second goal when Alexander Isak received a pass from Viktor Jörgensen, broke through the defense, and found the net with a right-footed shot. After conceding a goal to Hannibal Mejbri in the 43rd minute, Sweden intensified its attack in the second half. Jörgensen took advantage of a critical mistake by the Tunisian defense, scoring again in the 59th minute to extend the lead to 3-1. Matthias Svanberg, who came on as a substitute in the 39th minute, sealed the victory with a goal, followed by Ayari completing his brace in the 51st minute, finalizing the score at 5-1.* This article has been translated by AI. 2026-06-15 14:36:00

Sweden Dominates Tunisia 5-1 to Lead Group F at 2026 FIFA World Cup Sweden displayed an impressive offensive performance, defeating Tunisia 5-1 in their opening match of Group E at the 2026 FIFA World Cup on June 15 at the Estadio Monterrey in Mexico. Returning to the World Cup stage for the first time since 2018, Sweden increased its chances of advancing from the group stage. They currently lead Group F, surpassing Japan and the Netherlands, who played to a 2-2 draw in their earlier match. Group F has been labeled the 'Group of Death' due to its competitive nature. This year's tournament features an expanded format with 48 teams, allowing the top two teams from each group, along with the eight best third-placed teams, to advance to the knockout stage. Sweden struck first, scoring in the 7th minute when Yasin Ayari capitalized on a cleared ball and unleashed a powerful right-footed shot from distance. Ayari, who has a Tunisian father and a Moroccan mother, scored his debut World Cup goal against his father's nation and showed restraint during his celebration. In the 30th minute, Sweden added a second goal when Alexander Isak received a pass from Viktor Jörgensen, broke through the defense, and found the net with a right-footed shot. After conceding a goal to Hannibal Mejbri in the 43rd minute, Sweden intensified its attack in the second half. Jörgensen took advantage of a critical mistake by the Tunisian defense, scoring again in the 59th minute to extend the lead to 3-1. Matthias Svanberg, who came on as a substitute in the 39th minute, sealed the victory with a goal, followed by Ayari completing his brace in the 51st minute, finalizing the score at 5-1.* This article has been translated by AI. 2026-06-15 14:36:00 -

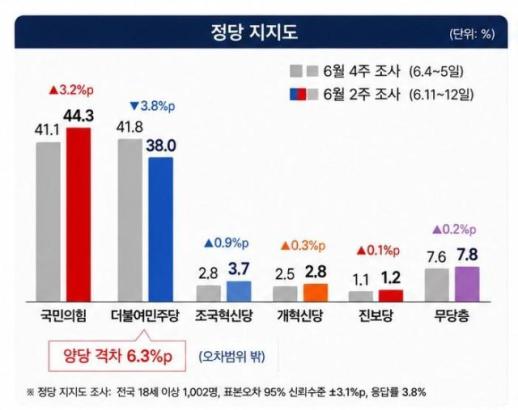

Public Discontent Reflected in Recent Polls: A Call for Political Responsibility Recent public opinion survey results have sent shockwaves through the political landscape. The ruling People Power Party (PPP) recorded a support rate of 44.3%, while the Democratic Party (DP) stood at 38.0%. This marks the first time since the inauguration of President Lee Jae-myung that the PPP has surpassed the DP by a margin outside the margin of error. President Lee's approval rating has also dropped to 51.5%, marking a decline for four consecutive weeks and nearly a 9 percentage point drop over the past month. The significance of these numbers lies not just in the figures themselves but in their implications. This shift in public sentiment reflects widespread disappointment and dissatisfaction with the political arena rather than a mere increase in support for a specific party. The controversy surrounding the Election Commission's handling of the June 3 local elections has left a profound impact on the public. Issues such as a shortage of ballots and vote counting errors are unacceptable in a democratic society. Elections are the cornerstone of democracy, and any erosion of trust in the electoral process inevitably undermines confidence in politics as a whole. Compounding these issues are the burdens of high inflation, soaring exchange rates, and an economic slowdown. The economic situation felt by the public is far from favorable. Small business owners are reaching their limits, and young people are struggling with employment and housing challenges. Citizens expect political leaders to address these pressing issues, yet the reality is filled with blame-shifting and political strife. Following the local elections, the DP has been engulfed in internal accountability discussions. Even within the party, calls for leadership accountability have surfaced. The controversies surrounding Representative Jeong Cheong-rae and factional conflicts reflect the instability of the ruling party. The focus on internal power struggles rather than a sober evaluation of the election results and necessary reforms is concerning. The PPP must also avoid misreading the situation. Following the rise in support, the party has quickly escalated its confrontational stance against the opposition, forming a special committee to prevent trial cancellations and discussing the possibility of impeachment. While opposition oversight is necessary, much of the support sent to the PPP by the public is a reflection of dissatisfaction with the DP's governance and the Election Commission's issues. Interpreting this as a comprehensive victory for the ruling party would be a misreading of public sentiment. One crucial aspect that the political sphere is overlooking is that this public opinion survey serves as a warning to the ruling party while also expressing expectations for the opposition. The public is not seeking a victory for one side but rather a return to normalcy in politics. Accountability for electoral failures is essential, as is the recovery of livelihoods. However, the focus of all discussions must center on the citizens. President Lee Jae-myung recently stated, "We must speak the language of responsibility rather than the language of conviction, and our focus should be on the entire nation, not just our factions." This is a message that the entire political landscape must heed. When politics becomes trapped in factional logic, the public disappears, leaving only the support base. The ruling party must remember its responsibility for governance, while the opposition must not forget its duty to propose alternatives. The reversal in support ratings just one year into the administration serves as a warning from the public to the political sphere. If both parties consume this as merely fuel for further political strife, the alienation of the public will only accelerate. The public desires a politics that works rather than one that fights. They seek accountable governance rather than a politics of blame. What is needed now is neither the cheers of the victors nor the excuses of the defeated, but an acknowledgment of what has gone wrong and a demonstration of what will be changed. That is the foundation, the principle, and the common sense. 2026-06-15 14:30:00

Public Discontent Reflected in Recent Polls: A Call for Political Responsibility Recent public opinion survey results have sent shockwaves through the political landscape. The ruling People Power Party (PPP) recorded a support rate of 44.3%, while the Democratic Party (DP) stood at 38.0%. This marks the first time since the inauguration of President Lee Jae-myung that the PPP has surpassed the DP by a margin outside the margin of error. President Lee's approval rating has also dropped to 51.5%, marking a decline for four consecutive weeks and nearly a 9 percentage point drop over the past month. The significance of these numbers lies not just in the figures themselves but in their implications. This shift in public sentiment reflects widespread disappointment and dissatisfaction with the political arena rather than a mere increase in support for a specific party. The controversy surrounding the Election Commission's handling of the June 3 local elections has left a profound impact on the public. Issues such as a shortage of ballots and vote counting errors are unacceptable in a democratic society. Elections are the cornerstone of democracy, and any erosion of trust in the electoral process inevitably undermines confidence in politics as a whole. Compounding these issues are the burdens of high inflation, soaring exchange rates, and an economic slowdown. The economic situation felt by the public is far from favorable. Small business owners are reaching their limits, and young people are struggling with employment and housing challenges. Citizens expect political leaders to address these pressing issues, yet the reality is filled with blame-shifting and political strife. Following the local elections, the DP has been engulfed in internal accountability discussions. Even within the party, calls for leadership accountability have surfaced. The controversies surrounding Representative Jeong Cheong-rae and factional conflicts reflect the instability of the ruling party. The focus on internal power struggles rather than a sober evaluation of the election results and necessary reforms is concerning. The PPP must also avoid misreading the situation. Following the rise in support, the party has quickly escalated its confrontational stance against the opposition, forming a special committee to prevent trial cancellations and discussing the possibility of impeachment. While opposition oversight is necessary, much of the support sent to the PPP by the public is a reflection of dissatisfaction with the DP's governance and the Election Commission's issues. Interpreting this as a comprehensive victory for the ruling party would be a misreading of public sentiment. One crucial aspect that the political sphere is overlooking is that this public opinion survey serves as a warning to the ruling party while also expressing expectations for the opposition. The public is not seeking a victory for one side but rather a return to normalcy in politics. Accountability for electoral failures is essential, as is the recovery of livelihoods. However, the focus of all discussions must center on the citizens. President Lee Jae-myung recently stated, "We must speak the language of responsibility rather than the language of conviction, and our focus should be on the entire nation, not just our factions." This is a message that the entire political landscape must heed. When politics becomes trapped in factional logic, the public disappears, leaving only the support base. The ruling party must remember its responsibility for governance, while the opposition must not forget its duty to propose alternatives. The reversal in support ratings just one year into the administration serves as a warning from the public to the political sphere. If both parties consume this as merely fuel for further political strife, the alienation of the public will only accelerate. The public desires a politics that works rather than one that fights. They seek accountable governance rather than a politics of blame. What is needed now is neither the cheers of the victors nor the excuses of the defeated, but an acknowledgment of what has gone wrong and a demonstration of what will be changed. That is the foundation, the principle, and the common sense. 2026-06-15 14:30:00 -

South Korea, Cambodia seek to expand cooperation through FTA SEOUL, June 15 (AJP) - South Korea discussed ways to broaden economic and trade cooperation with Cambodia, the Ministry of Trade, Industry and Resources said on Monday. Trade Minister Yeo Han-koo met with Cambodian Deputy Prime Minister Sun Chanthol in Seoul and held talks on expanding bilateral economic cooperation and strengthening collaboration in future industries. The meeting was requested by Chanthol, who is in South Korea to attend an investment blitz slated to be held in Incheon on Tuesday, which is expected to draw more than 200 business leaders from both countries to explore investment opportunities, share success stories, and build networks. During their talks, Yeo and Chanthol discussed a range of issues including ways to deepen cooperation through a future free trade agreement, as well as official development assistance (ODA) programs and international projects to reduce greenhouse gas emissions. According to the ministry, South Korea's trade with the Southeast Asian country, which has emerged as a new production base for ASEAN countries, has risen from US$966 million in 2021 to $1.16 billion last year and has continued to grow this year. Chanthol thanked Yeo for South Korea's ODA projects in Cambodia, saying they provide practical support for the country's industrial development and workforce training, and expressed hope for expanded cooperation. The ministry said it will continue to expand cooperation with Phnom Penh to help South Korean companies make inroads into the Cambodian market. 2026-06-15 14:25:43

South Korea, Cambodia seek to expand cooperation through FTA SEOUL, June 15 (AJP) - South Korea discussed ways to broaden economic and trade cooperation with Cambodia, the Ministry of Trade, Industry and Resources said on Monday. Trade Minister Yeo Han-koo met with Cambodian Deputy Prime Minister Sun Chanthol in Seoul and held talks on expanding bilateral economic cooperation and strengthening collaboration in future industries. The meeting was requested by Chanthol, who is in South Korea to attend an investment blitz slated to be held in Incheon on Tuesday, which is expected to draw more than 200 business leaders from both countries to explore investment opportunities, share success stories, and build networks. During their talks, Yeo and Chanthol discussed a range of issues including ways to deepen cooperation through a future free trade agreement, as well as official development assistance (ODA) programs and international projects to reduce greenhouse gas emissions. According to the ministry, South Korea's trade with the Southeast Asian country, which has emerged as a new production base for ASEAN countries, has risen from US$966 million in 2021 to $1.16 billion last year and has continued to grow this year. Chanthol thanked Yeo for South Korea's ODA projects in Cambodia, saying they provide practical support for the country's industrial development and workforce training, and expressed hope for expanded cooperation. The ministry said it will continue to expand cooperation with Phnom Penh to help South Korean companies make inroads into the Cambodian market. 2026-06-15 14:25:43 -

Samik Pharmaceutical Shares Rise on Expectations of Hair Loss Treatment Insurance Coverage Samik Pharmaceutical is experiencing a surge in stock prices following news that the government is considering health insurance coverage for hair loss treatments. The company’s long-acting hair loss treatment platform technology has attracted investor interest. As of 2:16 PM on June 15, Samik Pharmaceutical shares were trading at 7,700 won, up 29.85% from the previous trading day, according to the Korea Exchange. The rise in stock prices appears to be influenced by reports that the government is exploring health insurance options for hair loss treatments aimed at young people. The Ministry of Health and Welfare plans to gather public opinions in the second half of this year to assess the potential expansion of health insurance coverage for hair loss treatments. Health and Welfare Minister Jeong Eun-kyeong stated during a recent policy meeting that various opinions on the necessity of health insurance coverage for hair loss treatments would be collected before making a decision. The ministry is particularly focusing on options for individuals aged 20 to 34. Market expectations are growing that the hair loss treatment market could expand if health insurance coverage is realized. Consequently, there is heightened interest in pharmaceutical companies that possess relevant technologies and pipelines. Recently, Samik Pharmaceutical registered a patent for a technology that manufactures polymer microparticles using cyclodextrin complex compounds, securing its long-acting injectable platform technology. This technology serves as a foundational method for developing the JAK inhibitor baricitinib, used for treating alopecia, into a long-acting injectable administered once a month, as opposed to the current oral formulation.* This article has been translated by AI. 2026-06-15 14:24:00

Samik Pharmaceutical Shares Rise on Expectations of Hair Loss Treatment Insurance Coverage Samik Pharmaceutical is experiencing a surge in stock prices following news that the government is considering health insurance coverage for hair loss treatments. The company’s long-acting hair loss treatment platform technology has attracted investor interest. As of 2:16 PM on June 15, Samik Pharmaceutical shares were trading at 7,700 won, up 29.85% from the previous trading day, according to the Korea Exchange. The rise in stock prices appears to be influenced by reports that the government is exploring health insurance options for hair loss treatments aimed at young people. The Ministry of Health and Welfare plans to gather public opinions in the second half of this year to assess the potential expansion of health insurance coverage for hair loss treatments. Health and Welfare Minister Jeong Eun-kyeong stated during a recent policy meeting that various opinions on the necessity of health insurance coverage for hair loss treatments would be collected before making a decision. The ministry is particularly focusing on options for individuals aged 20 to 34. Market expectations are growing that the hair loss treatment market could expand if health insurance coverage is realized. Consequently, there is heightened interest in pharmaceutical companies that possess relevant technologies and pipelines. Recently, Samik Pharmaceutical registered a patent for a technology that manufactures polymer microparticles using cyclodextrin complex compounds, securing its long-acting injectable platform technology. This technology serves as a foundational method for developing the JAK inhibitor baricitinib, used for treating alopecia, into a long-acting injectable administered once a month, as opposed to the current oral formulation.* This article has been translated by AI. 2026-06-15 14:24:00