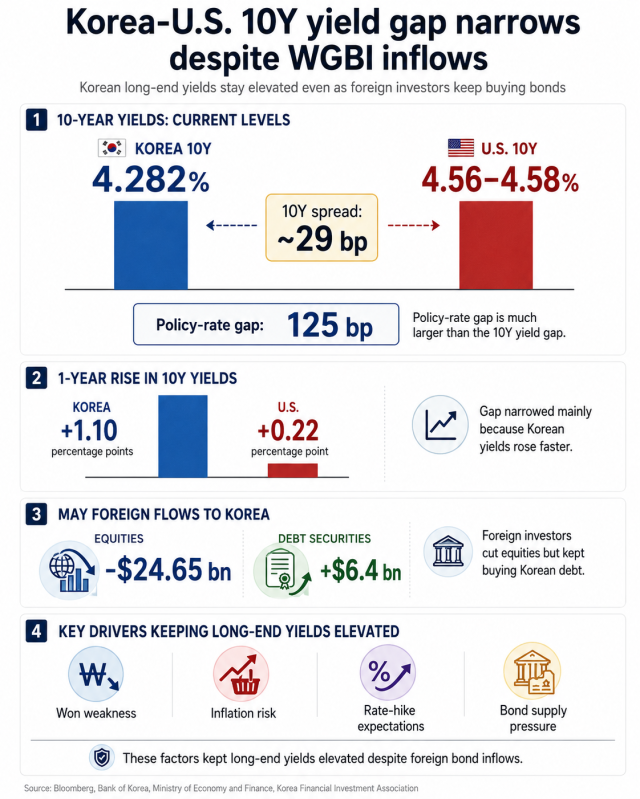

The spread between Korean and U.S. 10-year government debt has narrowed to less than 30 basis points, even though the policy-rate gap between the Bank of Korea and the Federal Reserve remains wider than 100 basis points.

As of midday Thursday, Korea’s 10-year government bond yielded 4.282 percent, while the corresponding U.S. Treasury yield was quoted around 4.56 to 4.58 percent in Asian trading.

Such a narrow gap between Korean debt and bonds issued by the world’s largest economy and reserve-currency issuer is rare.

On a monthly-average basis, the spread was last this narrow in July 2023, near the final phase of the postpandemic tightening cycle, when U.S. rates were still rising while Korean markets were already pricing in the end of BOK rate increases.

The BOK’s base rate stands at 2.50 percent, while the Federal Reserve’s target range for the federal funds rate is 3.50 percent to 3.75 percent. If long-term yields simply tracked current policy rates, U.S. 10-year yields would be much further above Korean yields.

The compressed spread shows that long-term yields are pricing far more than current central bank settings. They also reflect expectations for future rate paths, inflation, currency risk, bond supply and the term premium investors demand to hold longer-dated debt.

In Korea, those risk factors have pushed the 10-year yield higher even as weak domestic demand limits expectations for how far the BOK can raise rates.

The narrowing gap therefore does not simply mean Korean bonds have become more attractive against U.S. Treasuries. It suggests investors are demanding greater compensation to hold Korean long-term debt.

The latest rise shows that the recent sideways movement in Korean yields did not mean pressure had faded. The 10-year yield has struggled to move below 4.2 percent and is now approaching the 4.3 percent threshold.

Trading Economics data showed Korea’s 10-year yield was 1.10 percentage points higher than a year earlier, while the U.S. 10-year yield was up 0.22 percentage point over the same period.

That suggests the narrowing Korea-U.S. 10-year yield gap has been driven mainly by Korean bond weakness, not by any meaningful decline in U.S. Treasury yields.

Some analysts say Korean government bonds are already pricing in multiple rate increases, while geopolitical risks from the Middle East have revived inflation concerns through oil prices.

The won is another source of pressure.

For foreign investors, Korean bonds are not just a yield trade. They also carry exchange-rate risk. When the won stays near 1,500 per dollar, interest income from Korean bonds can be offset by currency losses.

That risk has persisted even after Korea posted a record current account surplus of $38.61 billion in May, led by a record goods surplus of $37.86 billion.

For long-term investors, the issue is not only whether Korea generates dollars through trade, but whether portfolio flows and currency expectations can stabilize enough to reduce the risk premium on won-denominated debt.

Inflation is another reason investors are demanding more compensation, especially as price growth remains above the BOK’s 2 percent target and renewed oil-price pressure revives global inflation concerns.

Still, the rise in Korea’s 10-year yield is not simply a bet on aggressive BOK tightening.

Strong semiconductor exports have supported growth, but weak consumption and pressure on small businesses are expected to limit how far the BOK can push rates above 3 percent.

Even planned issuance can weigh on the long end when global bond yields are elevated and domestic inflation risks remain priced in.

That has left the Korean bond market in an unusual position: foreign investors continue to absorb Korean debt, but the inflows have not been strong enough to pull long-term yields lower.

The main source of foreign demand is Korea’s inclusion in the World Government Bond Index this year, creating benchmark-driven buying from global passive funds and index-tracking investors.

Analysts say the WGBI effect has so far been uneven, with inflows concentrated more in short- and medium-term maturities than in longer-dated bonds.

May balance-of-payments data also pointed to the split in foreign flows. Foreign portfolio investment in Korean securities fell by $24.65 billion, while foreign investment in Korean debt securities increased by $6.4 billion on WGBI-related inflows.

Foreign investors, in other words, are cutting Korean equity exposure but remaining committed to Korean debt.

Korea’s yield shortfall against U.S. Treasuries has shrunk, but Korean bonds are also trading at higher yields as investors price in currency, inflation and supply risks.

For markets, the key question is no longer simply whether the Korea-U.S. yield gap narrows further. It is whether Korea’s 10-year yield breaks above 4.3 percent — and whether WGBI-driven demand can absorb the pressure from government bond supply.

Copyright ⓒ Aju Press All rights reserved.